'Maintain a balanced approach with a preference for short-to medium-duration funds.'

'A dynamic bond fund acts like a gilt fund in a rate cut scenario and like a conservative short-term bond fund when rates rise.'

Alternative investment funds (AIFs) have crossed Rs 5 trillion in terms of funds raised, while the investment commitments have surpassed Rs 12 trillion for the first time as of September, according to data released by the Securities and Exchange Board of India (Sebi).

'Investors can consider staying invested in long duration products as there is a possibility of rate cuts in the near term.' Positive macros - lower inflation, high forex reserves and favourable demand-supply dynamics for government bonds - make a strong case for rate cuts from December, says Devang Shah, head of fixed income, Axis Mutual Fund. In an interview with Abhishek Kumar in Mumbai, Shah says this view may not hold true if commodity prices go up sharply.

'When interest rates rise, the NAVs of these funds will fall.' However, they won't fall as much as longer-duration funds.

The introduction of tax deducted at source (TDS) on income from central government securities and state bonds may not lead to a significant effect on retail participation, according to market participants. The Union Budget proposed that starting October 1, 2024, investors may face a 10 per cent TDS on investments in central government securities and state development loans (SDLs). "Last Budget, TDS on interest on securities was reintroduced.

Overseas fundraising by Indian firms is experiencing a robust revival in 2024, following a lacklustre 2023. This resurgence is primarily driven by strong demand for high-yield bonds from international investors amid improving liquidity conditions and reduced hedging costs. Indian companies raised ~32,619 crore through overseas bonds in the first half of 2024, surpassing the total amount raised via such instruments in the entire 2023, which stood at ~31,218 crore, according to PRIME Database. In comparison, ~45,237 crore was raised in 2022 and ~1.05 trillion was secured in 2021.

Bond markets, global as well as domestic, are likely headed towards hard times over the next three to six months, as higher vegetable prices, rising fuel costs, and improved wages may keep inflation hot, believe analysts, who expect the yields to hit 7.5 per cent in the near-term from the current 7.234 per cent. In this backdrop, they suggest investors can put in money in funds/instruments with residual maturity of 4 to 6 years, while longer-term investors can allocate cautiously to the longer end in the range beyond 7 years.

Tactical investors should have an investment horizon of around six months to one year, long-term investors should stick around for 10 years or more.

Actively managed debt funds with the flexibility to go long on duration made a strong comeback on the returns chart in 2023, thanks to softening bond yields. The average one-year returns of floater, long-duration, gilt, and dynamic bond funds, which ranged between 2.3 per cent and 4.5 per cent at the end of 2022, now stand at over 7.2 per cent, with some schemes delivering over 8.5 per cent, according to data from Value Research. Debt fund returns are inversely related to yields of underlying investments, meaning a decline in yields is positive for funds.

'Your decisions should not be driven by your view on the market, but by your objectives, risk appetite, and time horizon.'

Debt fund managers are reassessing their strategies after the setback delivered by the Reserve Bank of India recently. While most are refraining from any knee-jerk reaction to the central bank's surprise open market operation (OMO) announcements, they are taking a re-look at the duration of their schemes. Sandeep Yadav, head of fixed income at DSP Mutual Fund, said it has trimmed the duration of some schemes, considering the hawkish stance by the RBI.

Opinions vary, but fund managers remain bullish.

'If rate cuts happen, bond yields will come down and investors will make mark-to-market capital gains on them.'

Highly-rated finance firms and housing finance companies are expected to benefit from the absence of Housing Development Finance Corp (HDFC) from the bond market once it merges with the HDFC Bank in early FY24. Post merger, the bond market is expected to become less crowded, which will ease fund raising conditions for other players in the field. It may perhaps also compress the spread for debt instruments floated by housing finance companies (HFCs) over 10-year government bonds, subject to demand and supply conditions.

'Banks will continue to increase FD rates to attract more deposits and meet the increasing demand for credit.'

Besides high portfolio yield, investors may enjoy capital gains in debt funds in 2023 as bonds rally in anticipation of rate cuts.

Covid-19, US yields, dollar to weigh on equity flows in the near term.

The Securities and Exchange Board of India (Sebi) on Monday relaxed the norms for valuing perpetual bonds. The norms, which had sought to value banks' deemed residual maturity of Basel III additional tier 1 (AT1) bonds as 100-year debt from April 1, were strongly opposed by the finance ministry. In a statement released on Monday, the regulator said the maturity would be 10 years until March 31, 2022, and would be increased to 20 and 30 years over the subsequent six-month period.

'It is going to be a tough balance for the RBI to manage economic stability and ensure smooth government borrowing.'

Issuers are currently not comfortable with the bids they have been getting for their bond offerings.

In 2021, there is the risk of interest rates spiking. Investors should tackle duration risk with a longer investment horizon, suggests Sanjay Kumar Singh.

Take a call to stay put or opt our based on whether you think the company will be able to find a strategic investor, suggests Sanjay Kumar Singh.

The RBI on Friday said it will give banks Rs 1 trillion through targeted long-term repo operations (TLTROs), of up to three-year maturity, to deploy in "investment-grade corporate bonds, commercial paper, and non-convertible debentures over and above the outstanding level of their investments in these bonds as of March 27, 2020."

.jpg)

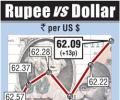

The Reserve Bank of India sold dollars via state-owned banks around 62.3575 per dollar to contain the rupee's fall, traders said.

.jpg)

In New York market, the dollar lost ground against most major rivals on last Friday amid mixed US data on industrial production and consumer sentiment.

.jpg)

Most Asian currencies weakened versus the dollar with the Thai baht and Philipine peso sliding on disappointing economic data.

Domestic shares and other global markets rose on upbeat trade data from China earlier in the day and after a US House deal extending the federal borrowing authority.

Mutual fund houses hold Rs 3,400 crore of Yes Bank's 'riskier' bonds. Reliance MF, Franklin Templeton MF and UTI MF account for bulk of these exposures.

In May 2014, FIIs were net buyers by Rs 20,225 crore (Rs 202.25 billion).

The rupee had gained five paise to close at 63.25 against the dollar in on Monday's trade on fresh selling of the US currency by exporters amid bullish stocks.

Forex dealers said besides the dollar's gains against other currencies overseas, increased demand from importers for the American unit put pressure on the rupee but a higher opening in the domestic equity market capped losses.

'Both IIP and CPI inflation numbers are showing a huge disconnect from the leading indicators.'

Go for high quality and low-to-medium-duration funds in your debt portfolio

RBI's foreign exchange reserves fell $237.5 million.

Debt fund managers think the Reserve Bank governor might at best go for one rate cut in April.

.jpg)

The RBI has bought Rs 124.62 billion worth of bonds since its announcement on Aug. 20 that it would occasionally buy bonds to relieve some of the cash tightness in the banking system.

The Reserve Bank of India cut its repo rate by 25 basis points to 6.50 per cent.