10 stocks which are most popular with brokerages right now and are expected to deliver maximum upside over the next 12 months.

The Indian equity market has been weak since it touched an all-time high in October last year.

The market since has been making low highs and lower lows, indicating lack of conviction among investors.

The benchmark S&P BSE Sensex is down 6.3 per cent, from its all-time high in October last year, but many stocks are down 30-40 per cent during this period on growth concerns.

Most brokerages, however, remain optimistic and expect another year of double-digit returns from the broader market.

The Sensex was up 18 per cent in 2021-2022 (FY22) -- its second consecutive year of double-digit returns.

Brokerages expect 13.6 per cent upside on average from BSE 200 stocks over the next 12 months, with the top performing stocks expected to rise 25-30 per cent by the end of 2022-2023 (FY23).

The confidence clearly reflects in their stock recommendations.

For example, there are 5,127 analyst recommendations for stocks that are part of the BSE 200 index.

Of which, 4,449 recommendations, or 87 per cent of total, are either 'buy' or 'hold' recommendations.

There are only 678 'sell' recommendations, which gives a ratio of more than five 'buy' calls for every 'sell' rating.

Analysts see strong double-digit growth in corporate earnings in FY23 to trigger a fresh round of rally in the markets.

Banks and information technology companies like ICICI Bank, State Bank of India, Infosys, HCL Technologies, and Tech Mahindra are expected to top the growth charts, with higher-than-average increase in revenue and profits.

Many brokerages also expect a positive surprise from top companies in consumer durables, automotive (auto), capital goods, and insurance sectors.

Here are 10 stocks which are most popular with brokerages right now and are expected to deliver maximum upside over the next 12 months.

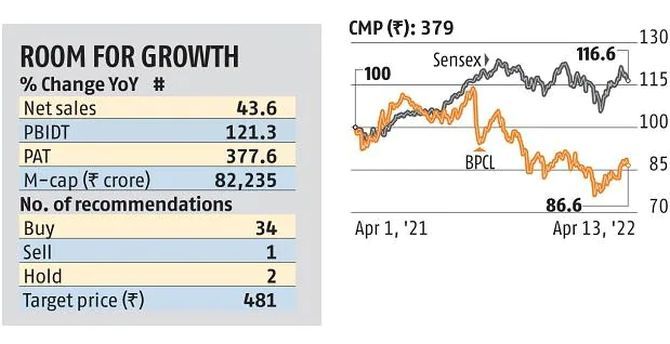

Bharat Petroleum Corporation

The public sector crude oil refiner and marketer is among the top picks of analysts, with 34 'buy' recommendations and just one 'sell' call.

Analysts expect the stock to gain 24 per cent from the current levels, even though it is down 5 per cent in the last 12 months.

Bharat Petroleum Corporation's (BPCL's) net profit was down 6.2 per cent year-on-year (YoY) in the first nine months of FY23 due to factors like inventory loss and lower marketing margins.

Analysts expect a turnaround in its earnings in FY23, driven by higher refining margins and improvement in marketing margins due to fuel price hikes.

The stock also gets support from an incredibly low valuation with trailing price-to-earnings (P/E) of 6.4x and price-to-book (P/B) value of 1.5x

The government's sale of BPCL should also lead to better price discovery for the stock.

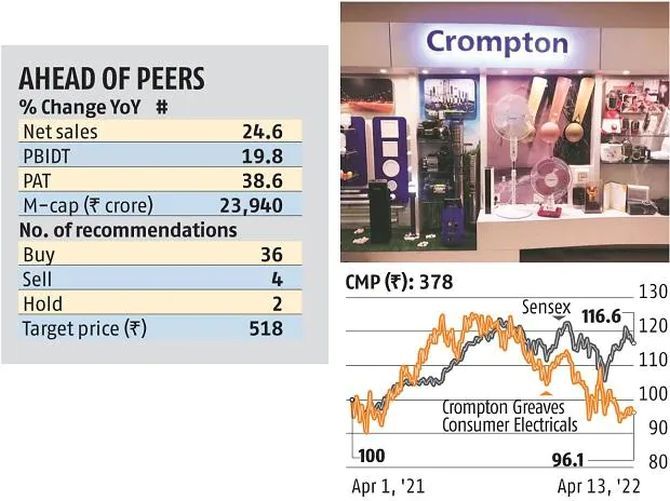

Crompton Greaves Consumer Electricals

After the recent acquisition of Butterfly Gandhimathi Appliances, the company is looking at gaining 15-20 per cent share of the small kitchen market by unlocking synergies from sourcing, manufacturing, and innovation.

While inflationary headwinds could impact near-term margins, IIFL Research says the company has been ahead of peers in relation to managing costs and restoring gross margins in the second half of calendar year 2021.

Strong brand recall, product innovation pipeline, industry-leading operating profit margin, and go-to market strategy may prop 2020-21 through to 2023-24 (FY24) annual net profit growth to 11 per cent, says Elara Capital.

The company has a strong balance sheet, with net cash of over Rs 1,000 crore, which should help drive future acquisitions and growth plans.

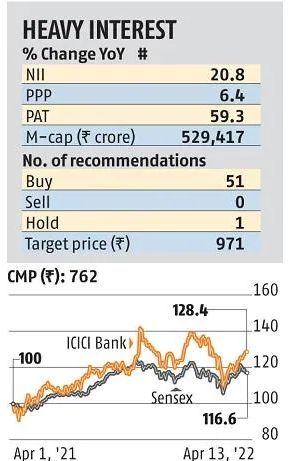

ICICI Bank

ICICI Bank is one of the top recommended stocks on Dalal Street (D-Street) right now.

It has 51 'buy' recommendations, one 'hold', and zero 'sell' rating, indicating analysts' strong conviction in the lender's long-term growth potential.

Its net profit was up 59.3 per cent YoY -- among the fastest in the banking industry -- in the trailing 12-months (TTM) ended December 2021.

Analysts expect the bank's earnings momentum to continue, driven by higher credit growth, margin improvement, and lower provisioning for bad loans.

The bank also scores on higher retail and digital orientation, and strong capital and provision buffers.

The risk to the stock comes from a steady rise in bond yields and potential rate hike by the Reserve bank of India that could result in lower margins in the first half of FY23.

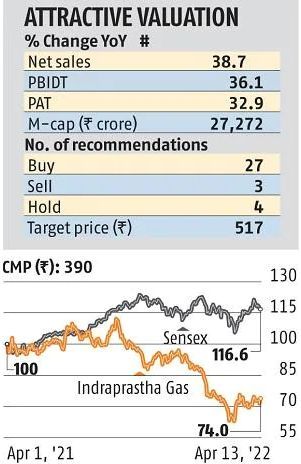

Indraprastha Gas

A consistent performer in the city gas distribution space, the company has posted an annual volume growth of 11 per cent and an earnings growth of 30 per cent over 2017-18 through to 2019-20.

The gains have come on the back of regulatory support and favourable economics.

There are near-term headwinds, given the rising cost of liquefied natural gas and high spot price of non-administered pricing mechanism gas, but gas is still cheaper than other fuels.

ICICI Securities believes that the economics of usage, environmental compulsions, and growing addressable market will continue to support stellar volume growth during FY22-FY24.

A long-term trigger could be the company's plan to set up battery charging stations on the battery swapping model.

Valuations are attractive, given the 30 per cent decline in the stock price in the past six months.

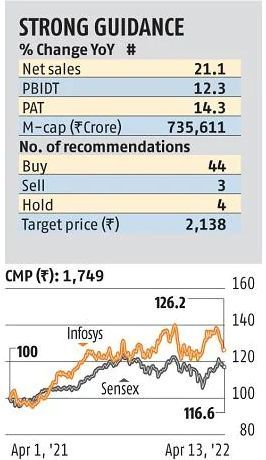

Infosys

Deal intake of $2.3 billion in the March quarter (fourth quarter, or Q4) and $9.5 billion in FY22 give good growth visibility in FY23, with large deals at their highest ever.

Infosys has guided for a 13-15 per cent YoY revenue growth on broad-based demand, strong deal pipeline, and client mining efforts.

Brokerages say there could be upward revision to it, given past trends.

Wage inflation, investments, and rise in travel and other costs have led to a moderation in the FY23 margin guidance to 21-23 per cent.

High attrition of nearly 28 per cent in Q4 is also a concern -- a trend also seen with peers.

However, Motilal Oswal Research believes Infosys could deliver margins on the higher side of its guidance band, with strong growth and reduced dependence on sub-contractors as attrition falls.

Brokerages expect Infosys to outpace Tata Consultancy Services on FY23 revenue growth and remain a beneficiary of accelerated global IT spends.

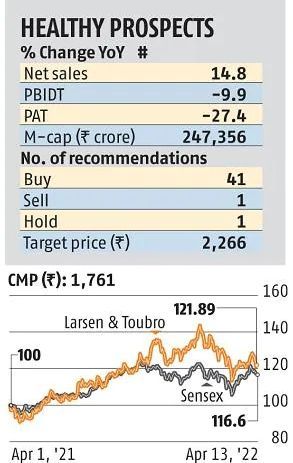

Larsen & Toubro

Larsen & Toubro (L&T) is another Street favourite in the large-cap space, with 41 'buy' recommendations and just one 'sell' rating.

The stock is up around 25 per cent in one year and brokerages expect further gains of 27 per cent in the next 12 months.

A good showing by L&T in FY22 was driven by a strong rebound in its core earnings (excluding other income) and a better-than-expected performance by its three IT subsidiaries.

Its core earnings before interest, tax, depreciation, and amortisation was up nearly 121 per cent on a consolidated basis during the TTM ended December 2021.

Analysts expect L&T to report high double-digit growth in earnings in FY23, driven by faster growth in its core engineering, procurement and construction business and continued good performance by its IT subsidiaries.

L&T's earnings, however, face risk from low government expenditure in FY23 and margin pressure in its IT business.

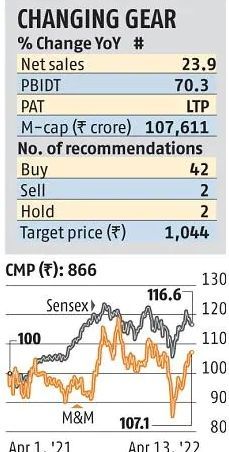

Mahindra & Mahindra

The auto segment is expected to get back on the growth trajectory in FY23, with the global semiconductor shortage showing signs of easing and production ramping up.

With utility vehicles accounting for 48 per cent of passenger vehicle sales, Mahindra & Mahindra (M&M) will stand to benefit, given its vast portfolio in the segment.

The company's focus on creating a diverse electric vehicle (EV) portfolio comprising 17 new products (FY24 onwards), including light commercial vehicles and three-wheelers, is another positive.

M&M is also looking at value unlocking by getting a strategic partner to fund growth and expansion in the EV business.

Strong agriculture exports, record kharif crop acreage, and normal monsoon rainfall should support tractor demand in FY23, according to Nomura, although current trends indicate sluggish performance.

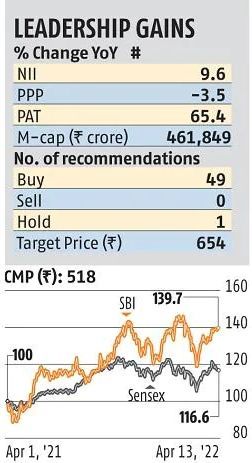

State Bank of India

State Bank of India (SBI) -- India's biggest bank by assets -- is also a favourite of D-Street right now.

The stock is up 50 per cent in the last 12 months, driven by strong earnings growth.

SBI's net profit was up 65.4 per cent YoY in the TTM ended December 2021, largely driven by 32.6 per cent YoY decline in provisions for bad loans and decline in interest expenses.

SBI's gross interest income was up by a modest 2.7 per cent on a TTM basis.

Analysts expect SBI's earnings to be driven by 9-10 per cent growth in its loan book and improvement in margins in a rising rate cycle.

The banks' earnings, however, face potential downside from a faster rise in cost of funds and a moderation in gross domestic product growth in FY23.

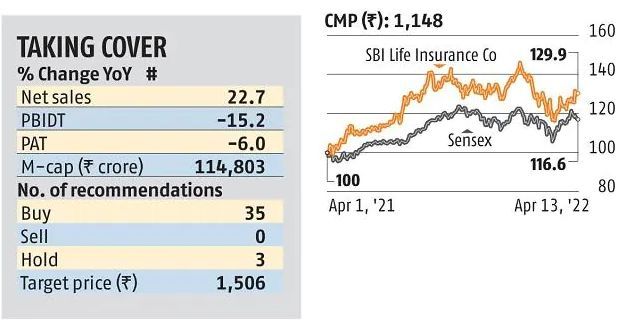

SBI Life Insurance

Brokerages expect SBI Life Insurance (SBI Life) to do well, given that target prices indicate an over 31 per cent upside over the next 12 months.

The stock has 35 'buy' ratings, zero 'sell' recommendations, and three 'hold' calls.

The life insurer's net profit was up 56.3 per cent YoY in the third quarter of FY22 after two quarters of earnings contraction.

Analysts now expect it to maintain the earnings momentum in FY23 as well, driven by faster growth in premium income, new product offerings, and margin improvement.

The life insurance industry, however, faces challenges from rising inflation and cost of living that could adversely affect premium growth/new business in FY23.

The SBI Life stock also faces downside risk from its rich valuation, with trailing P/E of 84x and P/B value of 10x.

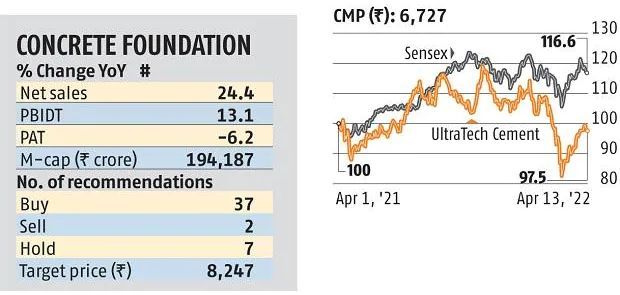

UltraTech Cement

Most brokerages are structurally positive on cement demand, considering the upcycle in the housing sector and the government's thrust on infrastructure.

Brokerages prefer UltraTech due to its leadership position, capacity growth, and efficient operations.

Sales volume for the sector will remain marginally lower in Q4, according to B&K Securities.

UltraTech's India volumes are seen falling 1 per cent YoY.

Credit Suisse has an 'outperform' rating on the stock, given the strong long-term demand outlook and pricing discipline, with commodities' pull-back driving profitability.

Valuations are at attractive levels, as the sector trades below its historical average valuation.

UltraTech is trading at 13x its enterprise value-to-operating profit, compared to the historical average of 15x.

Upside over target price; as on April 13, 2022; Buy, Sell, & Hold denote number of analyst recommendations; # trailing 12 months ended Dec 2021 (March 22 for Infosys); NII: Net interest income; PPP: Pre-provisioning profit; PAT: Profit after tax; M-cap: Market capitalisation; YTD: Year-to-date; LTP: Loss-to-profit; PBIDT: Profit before interest, depreciation and tax; upside is for one year, based on target and current prices (both rounded off); compiled by BS Research BureauSources: Bloomberg, Capitaline

Feature Presentation: Aslam Hunani/Rediff.com