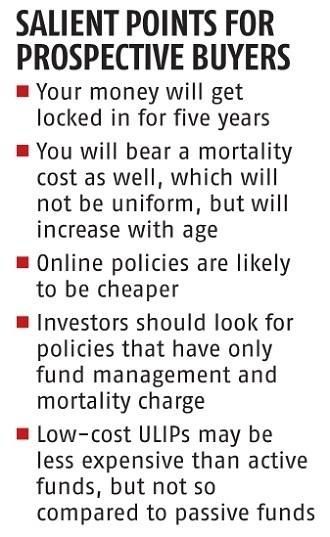

Stick to low-cost ULIPs launched in the past few years.

Go with an insurer with a good investment team and solid track record of long-term returns, suggests Sanjay Kumar Singh.

In Union Budget 2021-2022, the finance minister took away Section 10(10D) tax exemption from unit-linked insurance plans (ULIPs) whose annual premium exceeds Rs 2.5 lakh.

Such policies will now be taxed at 10 per cent at maturity.

The purpose behind providing this benefit is to encourage smaller customers buy insurance.

But many of these high-premium ULIPs are primarily investment products with only a thin wrapping of insurance.

Now, the tax treatment of high-value ULIPs will be on a par with that of other investment products, like equity mutual funds (MFs).

"Investment-oriented products should be treated on a par. If one enjoys tax exemption for maturity proceeds, that puts other products, whose proceeds get taxed, at a disadvantage," says Jimmy Patel, managing director and chief executive officer, Quantum Asset Management Company.

The impact

Existing investors in high-premium ULIPs (annual premium above Rs 2.5 lakh) will not be affected.

These changes apply only to policies purchased on or after February 1, 2021.

"Whoever has purchased a policy in the past can continue to enjoy exemption," says Ashok Shah, partner, N.A. Shah Associates.

In the future, the aggregate of policy premiums in ULIPs will be taken into account to calculate whether you are eligible for Section 10(10D) tax exemption.

So, splitting your ULIP premiums among companies to avail of tax exemption will not work.

One feature that made ULIPs attractive was that investors could switch between funds without attracting any cost.

In MFs, the investor gets saddled with capital gains tax and sometimes even an exit load on switching.

Experts are not sure if such tax-free rebalancing will continue in high-value ULIPs.

"Now they will be treated as capital assets. Such rebalancing could attract tax. But one should wait for the Central Board of Direct Taxes guidelines for clarity on this," says Deepesh Raghaw, founder, PersonalFinancePlan, a Securities and Exchange Board of India-registered investment advisor.

The attractiveness of high-premium policies has reduced.

"Policies where the premium is up to Rs 2.5 lakh will continue to enjoy tax exemption. Customers should confine themselves to such policies," says Rajesh Cheruvu, chief investment officer, Validus Wealth.

What you should do

Most investors, especially younger ones, should keep their investments and insurance apart.

"On the insurance side, they will have the flexibility to increase or decrease their term cover, depending on their liabilities and life stage. On the investment side, they will be able to choose the best fund managers across asset and sub-asset classes, instead of having their funds managed only by fund managers from one company, as is the case in a ULIP," says Vishal Dhawan, chief financial planner, PlanAhead Wealth Advisors.

Investing in MFs also allows the freedom to make thematic investments.

Well-informed high networth individuals may make tactical investments in ULIPs.

"They should keep 80-90 per cent of their corpus in equity funds. They should also have term insurance. About 10-20 per cent of their corpus may be tactically allocated to ULIPs," says Cheruvu.

According to Dhawan, investors unable to bear market volatility could benefit from the long lock-in in ULIPs.

These policies could also impose the required discipline on irregular savers.

Stick to low-cost ULIPs launched in the past few years.

Go with an insurer with a good investment team and solid track record of long-term returns.

Feature Presentation: Aslam Hunani/Rediff.com