When looking for alternatives, consider several parameters -- your investment horizon and liquidity requirement, post-tax returns, and risk.

Sanjay Kumar Singh reports.

Conservative retail investors and senior citizens find themselves in a predicament in today's low interest-rate environment.

For instance, at 6.25 per cent, the interest rate on HDFC's 66-month fixed deposit is at a 43-year low, according to media reports.

"The Reserve Bank of India's (RBI) benchmark repo rate is at 4 per cent.

This has pulled lending, and, hence, deposit rates down," says Adhil Shetty, chief executive officer, BankBazaar.

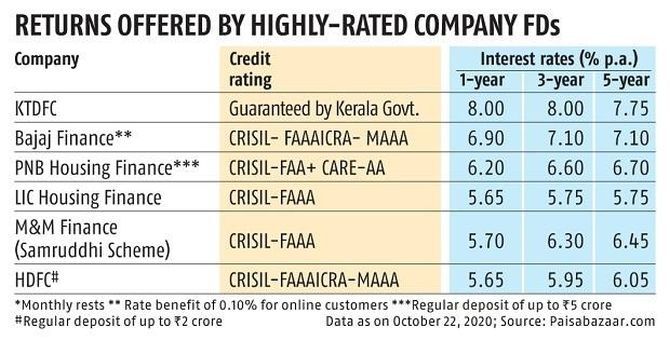

By moving from a bank FD to an AAA-rated corporate FD, you may be able to boost returns by about 100-150 basis points (bps).

But be choosy. "Stick to FDs from corporates that have a strong parentage or the support of a government entity," says Shravan Kumar Sreenivasula, director, investment advisory and products, Avendus Wealth Management.

The credit rating should be high.

"Go with FDs that have AAA or at best AA+ rating," says Raghvendra Nath, managing director, Ladderup Wealth.

He also suggests sticking to known names and market leaders.

Do not go down the credit curve.

"Many NBFCs are facing trouble in refinancing themselves. The risk of investing in them for an extra 100-200 basis points is not worth it," says Deepesh Raghaw, founder, PersonalFinancePlan, a Securities and Exchange Board of India-registered investment advisor.

Before investing in a corporate FD, look up that company's bond yield.

"If it is very high, or trading volume is thin, you should reconsider," says Raghaw.

Avoid locking yourself in instruments of above 12-24-month tenure.

"If economic growth returns, the rate cycle could reverse and you could move to instruments offering better yields," says Sreenivasula.

When looking for alternatives, consider several parameters -- your investment horizon and liquidity requirement, post-tax returns, and risk.

Among alternatives, the five-year Post Office Time Deposit Account, offering 6.7 per cent, may be considered as it offers Section 80C benefit.

But Post Office products are not easy to operate.

The RBI Floating Rate Bond (taxable), which offers 35 bps higher returns than the National Savings Certificate (7.15 per cent currently), is another option.

As in corporate FDs, interest income from these products is taxed at the slab rate.

Among long-term savings products, Public Provident Fund (7.1 per cent) and Sukanya Samriddhi Account (7.6 per cent) remain attractive.

Senior citizens looking to generate income may consider Senior Citizen Savings Scheme (7.4 per cent) and Prime Minister Vaya Vandana Yojana (8-8.3 per cent).

"Seniors may also consider the Life Insurance Corporation's annuity product (without return of purchase price option) Jeevan Akshay VII, which is giving 8.1 per cent to 60 year olds and 10.5 per cent to 70 year olds," says Raghaw.

Investors in higher tax brackets should consider debt mutual funds with a horizon of above three years (for favourable tax treatment).

Sreenivasula suggests investing in floating rate and short-duration funds.

Bharat Bond Exchange-Traded Fund, with a portfolio yield of 6.59-6.64 per cent over a 10-11-year horizon, may be used to lock in rates.

Nath suggests corporate bond funds and banking and PSU funds that invest mostly in AAA papers.

Feature Presentation: Aslam Hunani/Rediff.com