It is necessary and worthwhile to restore credibility to India's national income and growth estimates, rues Shankar Acharya

How fast is the Indian economy growing?

What is the sectoral composition or structure of the economy? How fast are major sectors expanding?

Until two months ago, we thought we had a pretty good idea.

Not so after January 30, 2015, when the Central Statistical Office released its newly based estimates of national income and growth.

Changes in base year are normal and happen every seven or eight years to accommodate fresh data sources, changes in economic structure and methodological improvements.

But this time (unlike ever before) the results of the base change, from 2004-05 to 2011-12, have led to substantial bemusement, bordering on incredulity, among many economists and analysts, including many in the government and the Reserve Bank of India.

What are some of the key issues and questions?

Before we get into these, it is important to emphasise one point: there is no evidence of any of political agenda behind this puzzling exercise.

Government and central bank officials seem as surprised and perplexed as those outside. It's a strictly ‘made-in-CSO’ conundrum.

Economic growth

The growth story of the past dozen years, according to the old (2004-05) base, is well-known: the unprecedented nine-per-cent-a-year boom of 2003-04 to 2007-08; a dip below seven per cent in 2008-09 following the global financial crisis and associated global recession; a smart recovery in 2009-10 and 2010-11, followed by a steep slowdown from 2011-12 onwards, yielding two successive years of below-five-per-cent growth in 2012-13 and 2013-14, for the first time in 25 years.

As the table shows, the new data tell a very different story for the three most recent years, the only three for which the CSO has given estimates according to the new 2011-12 base. Yes, 2012-13 growth is still below five per cent, but then there is a surprising rebound to 6.6 per cent in 2013-14 (6.9 per cent as measured by gross domestic product, or GDP, in market prices) and a further acceleration to 7.5 per cent in 2014-15 according to the ‘advance estimates’.

It is these last two years, 2013-14 and 2014-15, (averaging seven per cent growth according to the new base) that do not square with all the other available indicators: almost no industrial expansion according to the Index of Industrial Production, or IIP (also produced by the CSO!); sluggish growth in tax revenues; lacklustre corporate earnings; slowing bank credit expansion (down to its lowest level in 21 years in 2014-15); slowing investment and exports; a weak employment market; . . . and so on.

A growth rebound in 2013-14 is particularly puzzling, since that was the year when India experienced a mini balance-of-payments crisis (with significant outflows of capital) and a 300-basis-point policy interest rate hike during the second quarter.

To my knowledge, nowhere else have such unpleasant events spurred significant economic recovery!

Sectoral composition and growth

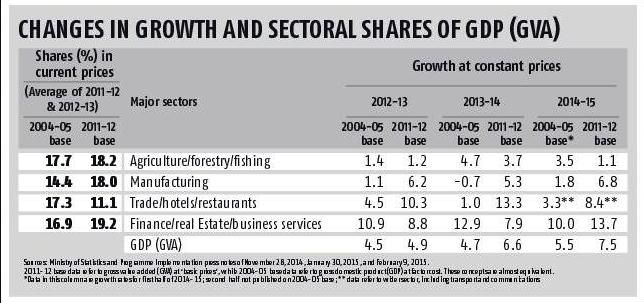

The first two columns of the table compare the shares of some major sectors in GDP according to the two bases. Here are some noteworthy points:

- For years, policymakers and analysts have bemoaned the low share of manufacturing in India's GDP, below 15 per cent according to the familiar 2004-05 base.

The new base tells us that the problem is perhaps not quite that bad, since it gives a share of 18 per cent.

Apparently, this change is mainly due to sourcing industrial data from the ministry of corporate affairs database on some 500,000 company accounts (the MCA-21 data) for the first time.

This may well be an improvement on past practice.

The problem is that a non-official member of the relevant CSO sub-committee, Professor R Nagaraj, has just published an article in the latest (March 28, 2015) issue of the respected Economic and Political Weekly, raising serious issues with the manner in which the CSO has used this data - Thanks mainly to the availability of new sample data for 2010-2011, collected by the National Sample Survey, the estimated share of wholesale and retail trade (and hotels and restaurants) has declined sharply from over 17 per cent of GDP according to the old base to 11 per cent in the new base

- On the other hand, the share of "finance, real estate and business services" in GDP has risen in the new base by a couple of percentage points to 19 per cent.

The new data also show remarkably higher growth rates for two key sectors, manufacturing and trade/hotels/restaurants, in recent years, as compared with the estimates according to the 2004-05 base.

The new data also show remarkably higher growth rates for two key sectors, manufacturing and trade/hotels/restaurants, in recent years, as compared with the estimates according to the 2004-05 base.

Thus, manufacturing is shown to be growing at five to seven per cent in 2012-2015, a good four to six per cent higher than estimated previously.

As in the case of overall GDP, such robust rates of growth sit awkwardly with trends in all other known indicators, such as tax receipts, bank credit, the IIP, corporate earnings and employment.

Is this because of infirmities in the use of MCA-21 data?

The same uncomfortable disparities arise with the trade/hotels/restaurants sector. According to the old base, this sector barely managed one per cent growth in 2013-14.

In contrast, the new base has it growing at above 13 per cent in the same year!

One could go on with raising more issues and puzzles.

The real issue is, what is to be done?

The way forward

It is clear that the new estimates of national income and growth do not readily pass the ‘smell test’.

Before they become the foundation of analytical descriptions and projections of the current, the past and the future trends in the Indian economy, a few things have to be done (most of which should have been done before publication of the new data series). Most importantly, the new methodology and the numbers it has yielded need to be subject to serious, independent, professional scrutiny.

It is understood that the National Statistical Commission has been entrusted with such a review.

That is certainly an important start.

Second, before the commission delivers its report (assuming it has been tasked to prepare one), it should organise one or more conferences of independent professional statisticians and economists on the matter.

Third, before any further publication of any revisions to the latest data, it might be wise to compile the ‘back series’ (for at least 10-15 years) according to the new methodology. All this will entail hard work and discomfort for all concerned.

But surely, it is necessary and worthwhile to restore credibility to India's national income and growth estimates.

Till such review and revision are complete, we really can't be too sure about India's current, past and prospective growth rates.

My own circumspect answer to the question in the title is that if India's gross domestic product grew at around 5.5 per cent in 2014-15 according to the old base, it will probably register six per cent plus growth in 2015-16 according to the same yardstick.

Not stellar, but better than nearly all other large economies in today's world.

Image: The bronze statue of Bull at the Bombay Stock Exchange. Photograph: Reuters

Shankar Acharya is honorary professor at Icrier and former chief economic advisor. These views are his own