Even if you get a bit late in buying things you need, it is always better to avoid debt traps, advises Vishwajeet Parashar

Illustration: Dominic Xavier/Rediff.com

Today's young generation is completely hypnotised by latest gadgets, new clothes and accessories to maintain their fancy lifestyle among their group. Thanks to the improving Indian economy which is helping youth to fetch decent salaries which they usually spend for their status war with peers.

Well, this could be the reason why many people today pay more EMIs compared to their monthly savings.

In addition, personal loans, home loans, car loan and consumer durable loans are adding burdens on their pockets.

When you take any loan, you sign documents of paying equated monthly installments on the long-term or short-term basis at a certain interest rate which lender/bank charges to you. With this, you make certain psychological adjustments to your finances.

1. You may compromise any other expenses, but you will be bound to pay monthly EMIs

2. Every new spending will make you do some mental calculation to check whether you can manage the burden with your existing EMI outgo

On the other hand, systematic investment plan (SIPs) in mutual fund schemes is quite popular investment options because of its consistent performance and ease of monthly contribution, which is as low as Rs 500.

One can fulfill her/his financial goals by linking her/his mutual fund SIPs and contributing the amount based on the calculation.

Which one is good?

In the case of EMI, if you are paying an EMI towards the creation of an asset then it is termed good as your asset will appreciate even if you pay interest on EMIs.

Therefore, any EMI paid for home loan repayment is good.

EMI paid to repay a car loan, credit card or personal loan is considered bad as you end paying huge interest on your principal amount and at the same time value of the goods which you have bought also gets depreciated.

When you invest in mutual funds through SIPs you gradually create an asset for yourself that will help you achieve your financial goals in life with the help of the power of compounding.

What to choose?

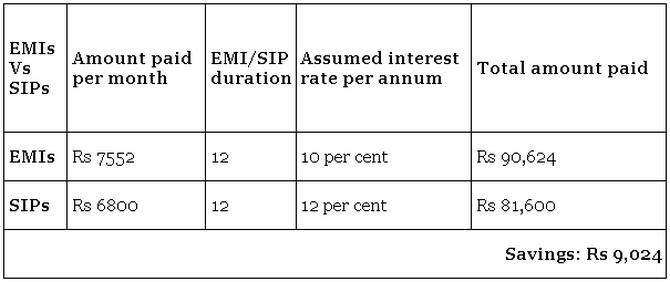

Let's suppose, next Diwali you plan to buy a new sofa set worth Rs 85,000.

One option is to plan it now and when Diwali comes you buy the same by swiping your credit card and convert the repayment into 12 monthly installments.

With this, you will end up paying almost Rs 90,626 approximately (Rs 7552 EMI per month for 12 months) at an assumed interest rate of 12 per cent, which could go up to 15 per cent depending upon the lender.

But if you plan it and start saving for it in advance, let's say an year before, you only need a SIP of approx Rs 6800 per month to save Rs 85000 till Diwali at an assumed and expected rate of return of 10 per cent.

The example above clearly explains the advantage of going for SIPs against buying any item on EMIs that include a substantial interest outgo. In fact, the SIP route also helps you save money that would otherwise end up in your lender’s account. At the same time it gives you and your family, a sense of security.

Conclusion:

Even if you get a bit late in buying things you need, it is always better to avoid debt traps which slowly pull you to the stage where you end up taking another loan to pay the previous loan. SIPs give you disciplined approach to investment at a very nominal amount to start with.

All you need to do is decide in advance how much money you will need to buy the goods that you want so that you can plan your SIPs amount accordingly.

Vishwajeet Parashar is Senior VP and Group Head -- Marketing, Bajaj Capital