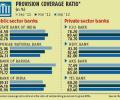

PCR is the ratio of provisioning to gross non-performing assets and indicates the extent of funds a bank has kept aside to cover loan losses. In December 2009, RBI had told all banks to maintain a PCR of at least 70 per cent by September 2010, to enhance their soundness.

Axis Bank reported a sharp drop in net profit in the second quarter of financial year 2026 (Q2FY26) on higher provisions and weak operating profit growth while revenue growth was moderate. But loan growth and deposit growth improved to double-digits year-on-year (Y-o-Y) and asset quality also improved with the gross non-performing loan or NPL ratio moving down.

Public-sector banks (PSBs) are attracting the attention of investors and the PSU Bank Index has gained nearly 10 per cent in the past month. PSBs have seen return on assets (RoA) climbing to 1 per cent in 2024-2025 (FY25) and margins are believed to have moved up further in the first half of this financial year (H1FY26) with asset quality remaining stable.

The banking sector could see better loan growth in the third quarter of financial year 2026 (Q3FY26) with improved net interest margins (NIMs), though the full impact of latest rate cuts will be largely felt in the fourth quarter. There may be lower slippage in unsecured loans and microfinance institutions (MFIs) along with steady recovery trends, which should lower credit cost.

Sanjay Malhotra has made structural changes to banking regulation to bring down costs and increase efficiency. Plus, he kicked off a benign interest regime. But there are challenges ahead.

Private sector lender Yes Bank on Saturday reported a 46.7 per cent growth in net profit to Rs 502 crore for the June 2024 quarter, helped by a reduction in provisions. The city-headquartered bank's core net interest income rose 12.2 per cent to Rs 2,000 crore. Its net interest margin stayed flat at 2.4 per cent.

Non-banking financial company (NBFC) Tata Capital is set to launch its much-anticipated $2 billion (Rs 17,200 crore) initial public offering (IPO) in the week beginning September 22, market sources familiar with the matter said on Sunday. The issue is expected to value the company around $11 billion, they added. Tata Capital is likely to make its stock market debut by September 30.

'As the team builds, each of them will bring in a different perspective, new thinking.'

Amid a rise in non-performing assets, most public sector banks have seen a substantial drop in their provision coverage ratio in the year since the reserve Bank of India (RBI) withdrew the 70 per cent provision coverage ratio norm.

India's largest PSU bank, State Bank of India, delivered excellent results, once the impact of a big jump in employee expenses was adjusted for. The net interest income (NII) beat the Street due to a better net interest margin (NIM) and good loan growth. The credit growth at 5.2 per cent quarter-on-quarter (Q-o-Q) (15 per cent year on year) was excellent for a large bank.

'Sebi's move to cap brokerage charges will help investors by lowering the overall cost of investments.'

A bill to repeal the MGNREGA and introduce a new rural employment law, the Viksit Bharat Guarantee for Rozgar and Ajeevika Mission (Gramin), has been circulated among Lok Sabha members.

We'll need to wait a couple of years to see how many restructured loans turn bad and whether some banks fall victim to their obsession for growth, explains Tamal Bandyopadhyay.

Bank of Baroda (BoB) has made prudential provision of Rs 500 crore for exposure to Go First, which has sought bankruptcy protection after the National Company Law Tribunal (NCLT) admitted its plea for voluntary insolvency. Sanjiv Chadha, managing director and chief executive officer of BoB, said the bank identifies issues in advance and makes provisions if required. The Mumbai-based public sector lender has an exposure of Rs 1,300 crore to the troubled airline.

'Bank has enabling provision to raise capital up to Rs 7,500 crore over a longer period of time.'

The bad assets or gross NPAs of commercial banks fell to a 12-year low of 2.8 per cent in March 2024 and may go down further to 2.5 per cent by the end of the current fiscal, said the RBI's Financial Stability Report (FSR) released on Thursday. Scheduled Commercial Banks' (SCBs) gross non-performing assets (GNPA) ratio fell to 2.8 per cent, and the net non-performing assets (NNPA) ratio to 0.6 per cent at the end of March 2024. "The asset quality of SCBs recorded sustained improvement, and their GNPA ratio moderated to a 12-year low in March 2024. Their NNPA ratio too improved to a record low," said the June FSR.

Shriram Finance's (SHFL's) profit after tax (PAT) rose 10 per cent year-on-year (Y-o-Y) to Rs 2,140 crore in the fourth quarter of the financial year 2024-25 (Q4FY25).

The bank's overall exposure to the 40 select accounts referred by the Reserve Bank to be resolved under bankruptcy laws is Rs 15,229 crore

The Reserve Bank of India on Monday said that RBL Bank is well capitalised and its financial position remains "satisfactory", amid speculations relating to the private sector lender in certain quarters in wake of recent events surrounding the bank. In a statement, the Reserve Bank of India (RBI) also said there is no need for depositors and other stakeholders to react to speculative reports. The bank's financial health remains stable, it said.

'Now we have one of the best asset qualities in the industry.'

Union Finance Minister Nirmala Sitharaman will review the performance of regional rural banks (RRBs) after the Budget session of Parliament, according to two people familiar with the matter. The finance minister will review the performance of RRBs after August 13. The review will include discussions on enhancing the digital capabilities of RRBs, said a senior government official.

The report said resilience of the banks has increased with a sharp improvement in the provision coverage ratio to 60.6 per cent in March 2019 from 52.4 per cent in September 2018 and 48.3 per cent in March 2018.

With high credit growth and healthy asset quality, listed commercial banks are expected to report steady growth in earnings during the fourth quarter ended March 2024 (Q4 FY24). Profits are expected to grow at 9.6 per cent year-on-year (Y-o-Y) and net interest income (NII) by 8.7 per cent in Q4 FY24, according to Bloomberg analysts' estimates. According to Motilal Oswal Securities, while bank credit growth has been robust, deposit growth has also gathered pace.

'Challenge is basically near-term growth as the outlook has turned a bit adverse.'

Axis Bank and ICICI Bank consumed 37-59 per cent of their operating profit for COVID-19 provisioning, while the figure is 24 per cent in case of Kotak Mahindra Bank and 10-12 per cent for IndusInd Bank and HDFC Bank.

Axis Bank's loan portfolio quality deteriorated, with gross NPAs rising to 5.22% of gross advances.

Yes Bank on Saturday reported over two-fold jump in standalone net profit at Rs 452 crore for March quarter 2023-24, primarily due to benefits on the provision front. In the year-ago quarter, the bank logged a profit of Rs 202.43 crore. The private sector lender benefitted from write-back on income tax and interest on income tax returns, but the profits were limited by its inability to comply with the mandatory priority sector lending (PSL) requirements, its management said.

In 2025 banks are in for challenges such as pressure on margins and slowing credit growth. With the likelihood of a repo rate cut in February or April, external benchmark-linked loans of banks will be repriced immediately. However, deposit rates are expected to adjust more gradually, which could impact the net interest margin (NIM) - a key measure of profitability for banks.

Since Sanjay Malhotra took office as governor in December, the Reserve Bank of India (RBI) has adopted a more accommodative stance, which bodes well for banking and the economy as they navigate a growth slowdown, according to analysts.

Global rating agency Fitch said on Monday that bank credit growth in excess of 13 per cent year on year in FY23 could put pressure on core equity tier ratios (CET1) of banks, especially public sector lenders. It may limit the buffers of Indian banks to absorb potential future losses. Bank credit expanded by 11.5 per cent in FY22. Full-year loan growth for FY23 will represent a modest slowdown from the 17 per cent YoY pace in H1FY23.

ICICI Bank reported good results for the October-December 2023 quarter (Q3), with 24 per cent year-on-year (Y-o-Y) growth in profit after tax (PAT). Net interest margin (NIM) dropped 10 bps quarter-on-quarter (Q-o-Q) to 4.43 per cent. Credit growth was at 19 per cent Y-o-Y (4 per cent Q-o-Q), while deposit growth was at 19 per cent Y-o-Y (3 per cent Q-o-Q).

LIC Housing Finance (LICHF) delivered a healthy FY24 with improvements in net interest margin (NIM) and credit costs and an improved return on assets of 1.7 per cent compared to an average of 1.3 per cent between FY14-FY23. Loan growth was low due to technology upgrades to the platform in H1FY24, though momentum improved in H2FY24. In Q4FY24, the net interest income (NII) came in at Rs 2,250 crore.

Axis Bank's results for the fourth quarter of the 2022-23 financial year (Q4FY23) were skewed due to large one-off charges related to its acquisition of Citi's retail business. Axis reported a loss of Rs 5,730 crore on account of exceptional items of Rs 12,350 crore (net of tax) towards Citi's acquisition, policy harmonisation etc. Excluding this one-off, the adjusted net profit or profit after tax (PAT) would be Rs 6,630 crore, up 61 per cent year-on-year (YoY).

Rising bad loans continued to haunt public sector banks (PSBs) in the March 2016 quarter.

SBI Cards & Payment Services reported mixed results for the January-March quarter (Q4) of FY24. While it managed to deliver strong earnings growth, it saw a perceptible decline in net interest margin (NIM) and suffered deteriorating asset quality. Taken together, the market was disappointed with the share dropping 3.5 per cent.

Banks enjoyed an expansion in Net Interest Margins (or NIMs) as well as in credit demand through the 2022-23 financial year (FY23). The credit expansion was because economic growth continued to recover from the Covid-19 years, and indeed, second half GDP growth surprised on the upside. The NIM expansion was because banks raised lending rates immediately (in many cases automatically due to floaters) as the Reserve Bank of India (RBI) hiked policy rates, and only started raising deposit rates late into the fiscal.

Treasury gains helped ICICI Bank post a nearly 10 per cent increase in the consolidated net profit for the April-June quarter at Rs 11,696 crore on Saturday. Growth in the core income slowed for the country's second largest private sector lender, but the treasury operations helped it report a 14.62 per cent rise in its post-tax profit at Rs 11,059 crore on a standalone basis. The core net interest income (NII) growth came at a multi quarter low of 7.3 per cent to Rs 19,553 crore for the reporting quarter.

'It is nice that the banking system is in good shape.' 'It is a little early to call it too good because I think it was too bad in the past.'

SBI Cards and Payment Services reported numbers that met Street expectations in the first quarter of the 2023-24 financial year (Q1FY24). The net profit came in at Rs 590 crore, while pre-provision operating profit grew 17 per cent year-on-year (YoY) (a little better than expectations). But provisions were hiked due to surprise stress from pre-Covid-19 period of 2018-19, and that dragged earnings.

If the earnings in the first quarter of the current financial year are an indication, most banks, particularly those majority-owned by the government, have fared well, reveals Tamal Bandyopadhyay.