The next correction is less about cash flows to corporates and more about relative risk asset valuations as currencies settle down to a new trading regime, says Sonali Ranade

Currencies have been driving markets as central banks wield the monetary policy to stimulate their economies. Much of the focus has been on Japan, but the Japanese Central Bank was late to the party.

The United States started the cycle of currency debasement taking the $ from 92 in 2007 to 73 in 2011. The ECB was next, tanking the euro from $1.58 in 2007 to $1.20 in 2011. In contrast, the yen actually appreciated against the $ from 2007 to 2011, with the $ moving down from 125 yen in 2007 to 76 yen in 2011.

So the Japanese depreciation of the yen that is touted as the latest round in the currency war hasn’t made up even 50 per cent of the debasement that was imposed on the $. But then when did the financial press ever reflect reality? If it did, we traders would be out of business!

The debasement of the $ is over in my view. Both the euro and the yen need to correct but their direction over the long term is also up. In the case of the euro and yen, corrections in currencies may also test equity and bond valuations. And that is basically what the ensuing correction in world markets is all about -- a reality check on all asset prices as the world settle down to a new regime of currency valuations.

India always seeks the muddle path. In the period 2007 to 2011, when the world was debasing currencies, the RBI had little clue on what its response should be. Absent a cogent policy, the INR traced a muddled path. Believe it or not, while others were actively debasing currencies, the RBI allowed the $ to first appreciate from INR 40 in 2007 to INR 51 in 2009 [the correct response] and the reverse, letting the $ depreciate from INR 51 to INR 44 in 2011 -- tanking both the economy and our exports.

Waking up suddenly to the looming balance of payment crisis in 2011, it allowed the $ to go from INR 44 to INR 57. Net net, from 2007 to 2012, we have debased the rupee from 1$=40 to 1$=57. Currently we are at 1$=54 INR. And export growth is 0, while CAD is 4 pc of GDP, prolly higher!

So the next correction is less about cash flows to corporates and more about relative risk asset valuations as currencies settle down to a new trading regime. Read the technical in that light.

|

Gold: Gold closed the week at $1609.50, decisively violating the support at $1620. Gold could return to test 1620 as an overhead resistance before proceeding lower towards the $1525 region. Gold’s 50 DMA is poised to pierce the 200 DMA from the top, which would signal a death cross. Barring reactive pullbacks, I see nothing bullish about the metal until it signals a bottom has been formed. |

|

Silver: Silver closed the week at $29.84, well below both its 50 and 200 DMAs. Gold has a floor at $28.50 which is the metal’s next logical target followed by $26. Silver could collapse much like gold as it nears $28. |

|

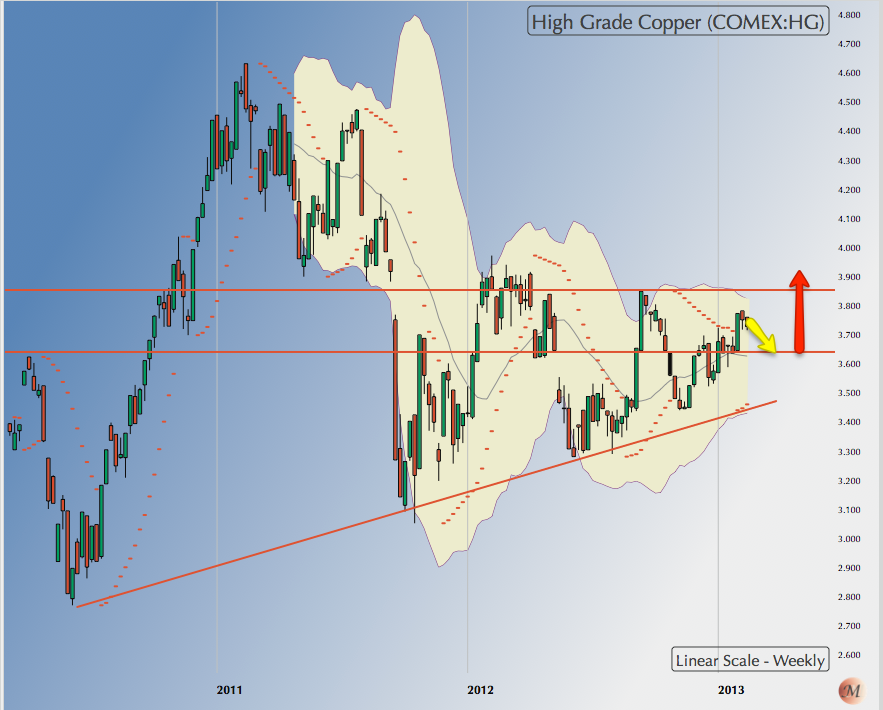

HG Copper: Copper closed the week at $3.734, well above its 50 and 200 DMAs. The metal appears to be testing the 3.70 as a support before moving higher. Its next logical target remains 3.85. Following any collapse in metal prices copper may not go below the 3.70 area. |

|

WTI Crude: WTI crude closed the week at $95.86, well above both the 50 and 200 DMAs. Crude appears to be testing the validity of its break atop $93 and the test may be nearing completion. Provided $93 holds true as the new support, expect crude to head the $100 level. Note, crude may retest $93 several times as other risk assets prices test supports over the next few weeks. |

|

US Dollar [DXY]: DXY closed the week at 80.576, above its 50 DMA but below its 200 DMA, which currently stands at 81. DXY appears to have completed its correction from the top of 84.25 at point C shown on the charts and put up bullish flag topping at 80.71. It could move higher from here to nick the 200 DMA at 81 before correcting. A move beyond 81.50 will signal the resumption of a bull run in DXY. |

|

EURUSD: EURUSD closed the week at 1.3362, just above its 50 DMA, which currently stands at 1.3290. The euro has completed the first leg of its bull run from 1.20 to 1.37. It is now into a Wave 2 correction the downside target of which could be 1.300 followed by 1.265. It will take a while to get there with many pullbacks in between. The next logical target is 1.31. |

|

USDJPY: The $ closed at Yen 93.48. By my reckoning of the wave counts, the rally in the $ vs Yen is over for now, having topped out 94.42. Expect the $ to correct in a normal bullish correction to the run-up from 75 to 94. The eventual target of the correction could be in the region of 84 Yen. |

|

USDINR: $ closed the week at INR 54.31 just below its 50 DMA. The 200 DMA is currently placed at 54.70 and the $ could well test that level before turning down towards its logical target of 51.50. Hard to read if anybody in RBI is really in charge of the desk that monitors this pair. India has been losing exports and yet the INR appreciates against the $. Strange RBI policies! |

|

Yield on 10-Year USTs: Yields on all US Treasuries have been creeping up. The rate on 10-year notes closed the week at 2.01 pc after having made a high of 2.05 pc during the week. As the weekly chart of yields shows, the rates have now decisively moved into a new trading range that spans from 2.0 pc to 2.30 pc. That may not seems much but could cause huge changes in incremental fund flows among asset classes. |

|

German DAX: DAX closed the week at 7593.51, some 240 points or 3 pc below its recent top. Has the DAX topped out? There is a small chance that DAX could reach for the all time high of 8095. However, a countdown from DAX’s top of July 2007 shows it has run out of time. [DAX topped earlier than SPX in 2007.] DAX prolly has made its top already and is now headed for a correction that may be rather shallow. First stop from here is 7450. |

|

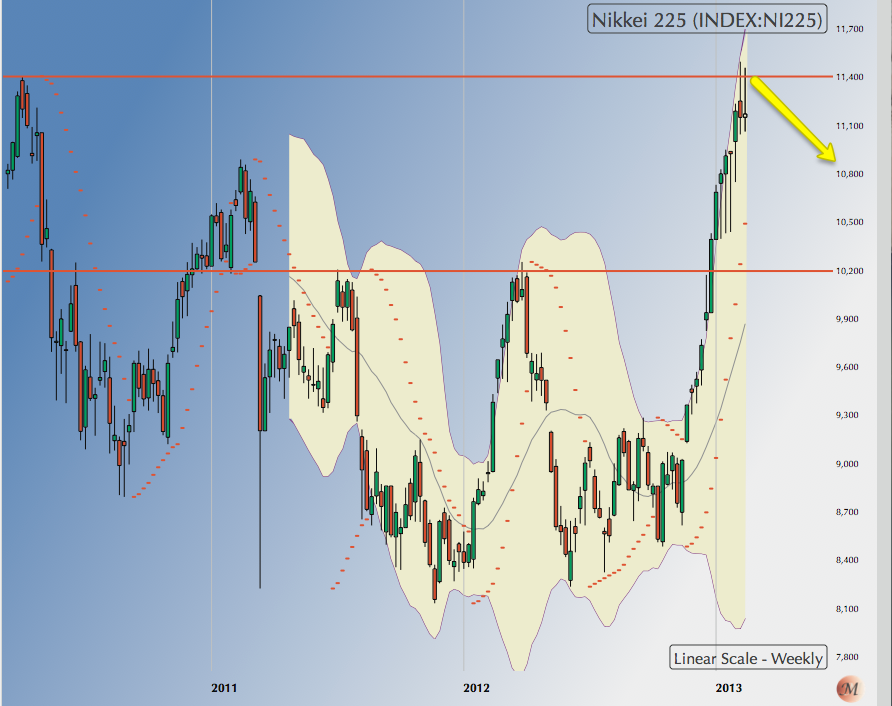

Nikkei 225: Nikkei 225 closed the week at 11,174 after having made a top of 11,506. By my wave counts, the current rally, more a bear rally really, is over and the index could correct down to 10.200. Note, the ensuing correction is more in the nature of a normal correction to run up from 6840 to 11,500 spanning a little over four years and the fall comes at the fag end of the correction. It is not a bear market. The correction may be both short and shallow. |

|

S&P 500 [SPX]: SPX closed the week at 1517.1. My D-day for the end of this rally is February 22, Friday. Not that it is possible to be that precise. Just that we are pretty much done in terms of the current rally though a higher high is not ruled out. My sense is that we will probably see a short, shallow correction before the rally resumes. I would be surprised if 1420 were taken out in the ensuing correction. But you never know. So treat 1420 as first stop. |

|

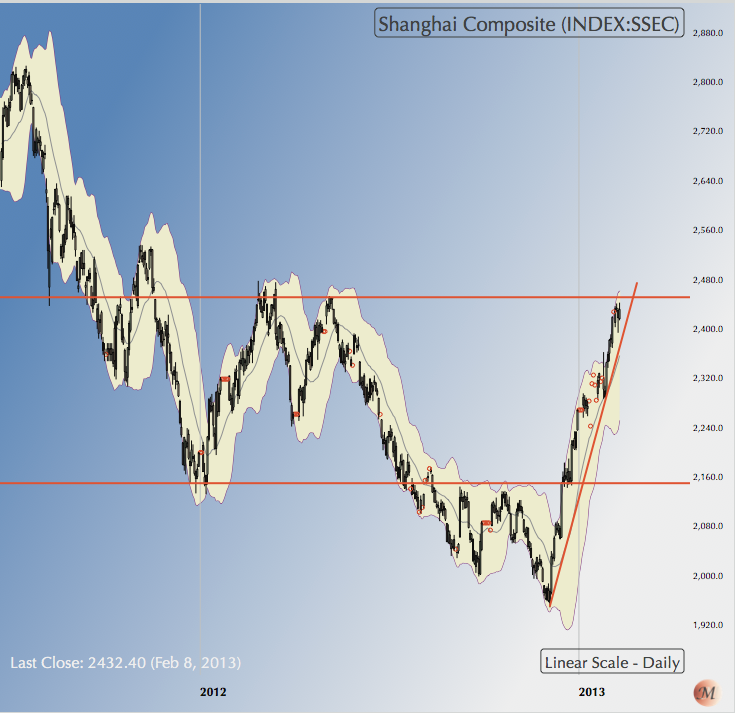

Shanghai Composite: Just to complete the picture on the corrections due in world markets, take a look at the Shanghai Composite. Big overhead resistance is looming at 2500. Such major overhead resistances are rarely taken out at first attempt. So a modest correction is due and it could well turn out to be 30 pc to 50 pc of the gain from 1950 to 2500. The correction times well with world markets. |

|

NSE NIFTY: NIFTY closed the week 5887.40. That was well below both its 50 and 200 DMAs. With the violation of 5950, the next logical target for NIFTY now becomes 5700. Note, the 200 DMA is now placed at 5500 and it is highly unlikely that NIFTY will breach that level in the current correction. |

To me the ongoing correction is a buying opportunity for long-term investors especially in cyclical blue chips. NIFTY’s correction too could be timed to end with world markets and could be short and shallow from here on.

NB: These notes are just personal musings on the world market trends as a sort of reminder to me on what I thought of them at a particular point in time. They are not predictions and none should rely on them for any investment decisions.

Sonali Ranade is a trader in the international markets