Tax planning should not be left for March.

If you do so, you could face a severe cash crunch in that month, warns Sanjay Kumar Singh.

The end of the financial year is three months away.

If you have not begun investing for tax-saving yet, you need to start the process right away.

If you leave this crucial task for March 2021, you will not have the leisure to decide which options are best suited for you.

If you invest in haste, you could even fall prey to the mis-selling that is rampant during the last quarter.

Choose the right tax regime:

Two tax regimes are now available to taxpayers.

Calculate your tax liability under both the new and the old regime and select the one that is more beneficial to you.

The new tax regime, wherein you pay a lower tax rate but don't get the benefit of most tax deductions, is better suited for taxpayers with lower incomes between Rs 5 and 8 lakh.

According to Deepesh Raghaw, founder, PersonalFinancePlan, a Securities and Exchange Board of India-registered investment advisor, "People who do tax saving to the extent of Rs 2 lakh -Ras 2.25 lakh or more will be better off in the old tax regime."

Adds Archit Gupta, founder and CEO, ClearTax, "Those who are diligent about tax saving, who ensure they get the maximum deduction under various sections like 80C and others, should continue with the old tax regime."

Those who opt for the new tax regime will, of course, not have to make any forced investments.

"They will enjoy greater freedom regarding where to invest. They must, on their own, ensure they create an emergency corpus, and invest towards key financial goals like retirement," says Gupta.

Account for taxation of dividend from equities:

In the Union Budget 2020-2021, dividend from stocks and equity mutual funds was made taxable in the hands of investors.

Earlier, many investors who did not have an active income (from a job or a business), but derived their income from large investment portfolios, structured them in such a manner that they received a large, tax-free dividend income each year.

Since their tax liability was low, they also invested less in tax-saving products.

"Now that dividend income from equity products has become taxable in the hands of investors, such investors will have to restructure their portfolios. It also means they may have to begin investing more in tax-saving products from this year," says Arvind Rao, chartered accountant and founder, Arvind Rao & Associates.

Locking in money is not advisable always:

Many people aged around 30 may be planning to buy a house within the next two-three years and need to save money for down payment.

If they invest in a tax-saving product, their money will get locked up for at least five years (barring in tax-saver mutual funds, where the lock-in is three years only).

"It may make more sense for such people to accumulate money for their goal rather than try to maximise their tax saving," says Rao.

Financial planning first:

Taxpayers need to invert the traditional order and think about their financial goals first, and about tax saving next.

Most investors have long-term goals such as saving for retirement, children's education and marriage, and so on.

Once they have identified their goals, they may choose products that will help them achieve them while also providing tax benefits.

Gupta says that the risk level of the products chosen must match the investor's risk appetite.

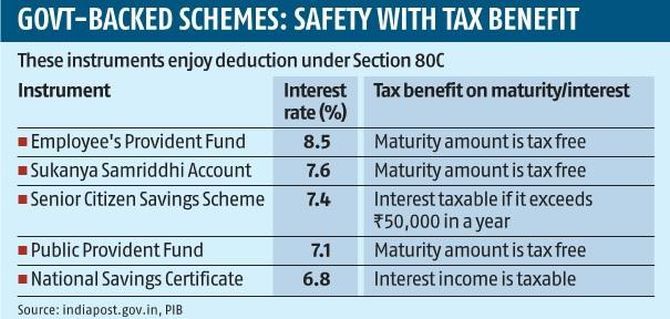

Adds Raghaw: "Products like equity-linked savings schemes (ELSS) and Public Provident Fund (PPF), which also offer Section 80C tax benefit, are a good fit in portfolios aimed at achieving long-term goals."

Most people need term and health insurance and should buy adequate amounts of them at the earliest.

The tax benefit on them should be treated as a bonus.

Avoid over-investing in tax-savers:

Many taxpayers tend to lock up a larger part of their corpus in tax-savers than is necessary.

To avoid this, calculate all the expenses, deductions and investments you already make that are eligible for tax benefit.

If you are a salaried employee, your employer would be deducting your contribution towards Employee's Provident Fund (EPF).

Those who have children tuition fee to pay are eligible for Section 80C deduction.

Most people also have insurance policies.

Only after you have added up all these elements should you think of making additional tax-saving investments.

Give yourself time:

Tax planning should not be left for March.

If you do so, you could face a severe cash crunch in that month.

Also, at that point of time, salespersons from the financial sector are out in full force.

They invariably pitch products where they earn the highest commission, not those that are best suited for your needs.

You need time to understand the pros and cons of various tax-saving options.

"It is for this reason that taxpayers should plan their taxes in advance and avoid the last-minute rush," says Gupta.

Traditional plans from insurers usually offer inadequate insurance cover and low investment returns.

As for unit linked insurance plans (ULIPs), the agent may tell you that the version he is selling is low-cost.

What goes unsaid is that the portion of the premium that goes towards paying for life cover increases with age (unlike a term plan where the premium remains constant).

So, while a low-cost ULIP may be suitable for someone who is 25 years old, it may not be as suitable for someone who is, say, 55 years old.

The higher cost the latter pays for life coverage will erode his returns.

Many people mistakenly buy an insurance product thinking it is a one-time commitment.

When they realise it is an annual commitment which they can't afford, they let the policy lapse and lose their money.

If you invest in ELSS in March, there is a possibility you could purchase units at a time when the markets are high.

Instead, if you begin a systematic investment plan at the start of the financial year, you would get the benefit of rupee-cost averaging.

It is difficult to get into such nuances if you make tax-saving investments a couple of days before the deadline.

Feature Presentation: Aslam Hunani/Rediff.com