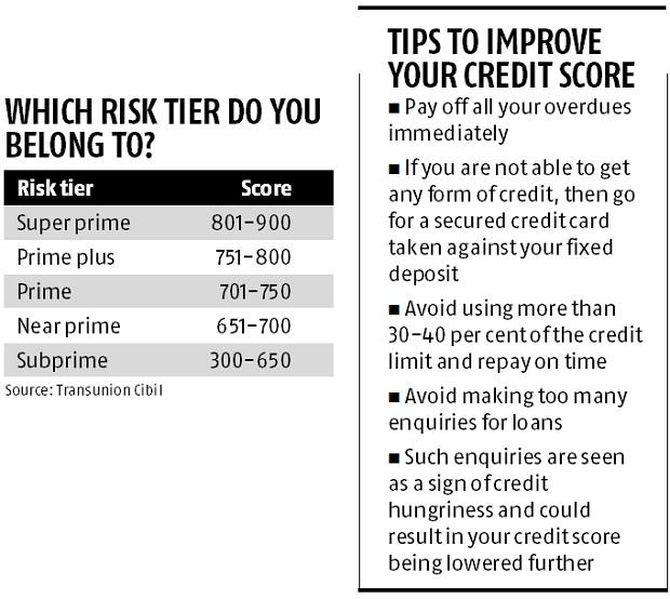

'A score of 750 and above is considered to be good, though these cut-offs can vary depending on the type of loan being sanctioned,' points out Arun Ramamurthy.

The credit score ranges from 300 to 900 and measures the probability that a customer will default.

It is designed to decide whether you will get a loan and at what interest rate.

Everything like a credit card or a home loan is dependent on your credit score and, hence, it is imperative that the scores are calculated and reported correctly.

The credit score is calculated based on the credit history of an individual over past 24 months.

The score is dependent on a combination of factors like credit utilisation; type, amount and duration of credit facilities availed; month-on-month credit payment behaviour; delinquencies and defaults; written-off or settlements on credit facilities and also the credit history on loans by the consumer.

The score is dynamic and will change based on the individual's month-on-month credit activity and payment behaviour.

However, it's also becoming increasingly apparent that the credit score (the three-digit number) works in patchy way when it comes to discriminating on risk.

In fact, most lenders look at the content in the report and then take a decision (even ignoring the credit score).

In theory, it should be simple enough, given accurate data, to make a statistical model that ranks people on credit scores.

The problem is, however, the data itself.

If the data is faulty, the resultant scores may not be accurate.

Also, a lot of lending institutions report the data with a lag, which also accentuates the problem.

The risk models used to generate a credit score are mostly imported from developed economies where the lending ecosystem is robust.

These models, while tweaked for India, may not capture the essence of India's diversity leading to score mismatches.

Pros of credit score

Measures risk of default

Mathematically, the credit score measures the probability that a person will default in the next 24 months.

It's a great measure of individual risk.

Determines whether you get a loan

Lenders typically apply a score cut off while deciding on a loan or card application.

A score of 750 and above is considered to be good, though these cut-offs can vary depending on the type of loan being sanctioned.

Enables risk-based pricing:

A person with a high credit score is associated with lower credit risk and could be priced lower and vice-versa.

Utility extends beyond lending:

The credit score has gained a wide range of applications -- in jobs, telecom, insurance, property rental, etc.

Nowadays, companies have started to check a person's credit score before making job offers.

This helps to exclude candidates with poor risk (integrity) profiles.

Cons of credit score

There are quite a few problems with the credit score.

Different bureaus come up with different scores, and there is lack of standardisation.

The credit scores seldom rank, which makes risk differentiation difficult, especially at lower score bands.

The issue is that at scores below 600, one can't really say that a person with 550 score has a better credit profile compared to someone with a 450 score.

As not much lending happens in these segments, not enough data is available for giving a score.

Lenders often use only the data in a credit report and not the credit score.

And rather inexplicably, scores often remain static for months together.

How to improve credit score

Notwithstanding the controversies surrounding the credit score, its conceptual utility as a measure of individual risk cannot be underestimated.

Generally speaking, a score of 750 and above is considered to be good from a lending point of view.

One can take several steps to improve one's score.

The time it will take for your score to improve is the amount of time required by you to accomplish the following steps:

Check if you have overdue payments:

If yes, repay these immediately.

A person's payment history has a major weightage in credit scoring.

A missed payment can lower your score.

Do not close old credit cards:

The older your credit card relationship, the higher your credit score is likely to be.

Often, people close old credit cards because they feel they have too many of them.

An old card is valuable from a credit scoring perspective and should not be closed.

Have a mix of loan types:

You should have a mix of secured and unsecured loans -- credit cards, personal loans, home loans, etc.

Having different types of credit gives the bureau data about how a person is performing on different types of credit lines.

This diversity helps improve your score.

Keep card utilisation ratio low:

Try and keep your card utilisation to below 30 per cent of your credit limit.

This is an important point.

Using your card at high levels of credit limit indicates credit hunger, which can impact your credit score negatively.

Take some form of credit:

If you have a low credit score, chances are that you do not have any active card or loan.

Try and take a secured credit card from a bank.

These cards are easily available from major banks and help in two ways.

You get a lower rate of interest on your fixed deposit while leveraging this deposit to take a card.

If you back your loan regularly on time, it will reflect on your bureau report and improve your score.

Do not utilise this card for more than 30 per cent of the credit limit.

Once you do get a new credit card, use it wisely.

Do not over-use it and do not miss any payments on it.

Do not apply for new loans or credit cards for the next six months.

Any application for a loan gets flagged off as an inquiry on your credit report.

More the inquiries, more the perceived credit hunger, which affects your credit score adversely.

A good credit score is not about having no credit, nor is it about having too much credit.

This is what makes having a good credit score so challenging.

Maintaining and improving your credit score is like walking the middle path.

Too much of credit and your credit score can reduce.

Too little credit and the bureau won't have any data to score you.

Arun Ramamurthy is an industry expert and the author of Unlock The Power Of Your Credit Score