Ensure that you get a high sum insured.

Also, make sure the policy covers the cost of implants (pacemaker, stent, etc), and pre and post-hospitalisation expenses, advises Bindisha Sarang.

One trend that has got experts worried is that younger people are increasingly falling prey to cardiac ailments.

According to the Indian Heart Association, nearly 50 per cent of all heart attacks in Indian men occur in those below 50 years, while 25 per cent occur in those below 40.

Indian women, too, have high mortality rates arising from cardiac diseases.

The high cost of treatment of cardiac ailments is another cause for worry. An angioplasty can easily cost Rs 5 lakh-Rs 6 lakh.

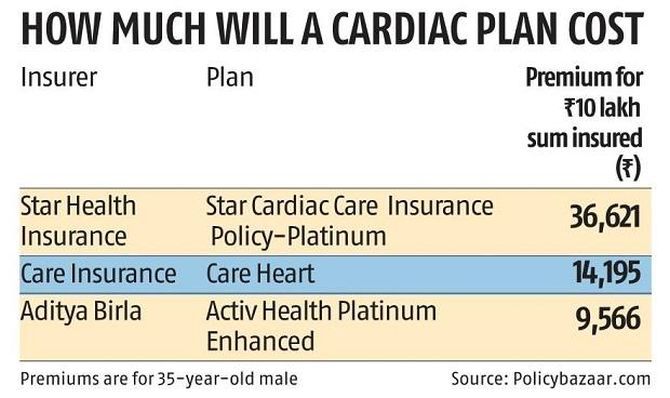

Cardiac-specific plans

A number of insurers offer cardiac-specific insurance policies.

These plans cover most heart-related treatments, like bypass, heart failure, cardiomyopathy, angiography, insertion of pacemaker, etc.

Some also cover outpatient expenses.

These cardiac-specific plans are useful, especially for people already suffering from a heart condition.

Says S Prakash, managing director, Star Health and Allied Insurance: "Our policy offers coverage even to people already suffering from a heart condition, or those who have undergone a heart-related procedure. We cover people from 7 to 70. Congenital heart diseases, installation of pacemaker, and transplants are all covered."

Some of these policies may not even require a medical screening.

Some cardiac plans cover heart-related conditions exhaustively and also cover hospitalisation costs for other diseases (just like a comprehensive health insurance plan).

Among cardiac-specific plans, both indemnity covers (which pay the actual cost of hospitalisation) and fixed-benefit covers are available.

Says Amit Chhabra, head-health insurance, PolicyBazaar: "Several insurers offer fixed-benefit health plans for heart-related conditions. These plans pay a lump sum if the insured is diagnosed with a cardiac condition."

Since a cardiac-specific plan covers only one disease, it is likely to be less expensive than a critical illness plan.

Check waiting period

Whether you are buying a comprehensive health insurance plan, a critical illness plan, or a cardiac-specific plan, check out the waiting period.

Says Naval Goel, founder and chief executive officer, PolicyX.com: "Some plans will not cover existing heart-related conditions at all. Some will cover them after a specified waiting period. Cardiac-specific plans offer coverage with the shortest waiting period."

In comprehensive health insurance policies, the coverage usually kicks in after 90 days.

In the case of a pre-existing heart condition, the coverage may be offered after three-four years.

If you have a heart ailment

People who already have a heart condition may not be able to purchase a comprehensive health insurance plan.

"As soon as a person is detected with a heart-related condition, he should buy a cardiac-specific plan," says Goel.

Ensure that you get a high sum insured. Also, make sure the policy covers the cost of implants (pacemaker, stent, etc), and pre and post-hospitalisation expenses.

But if you are healthy...

People not suffering from a heart condition should buy a comprehensive individual or family-floater plan.

Says Pankaaj Maalde, Mumbai-based certified financial planner: "If you have a comprehensive health insurance policy of Rs 10 lakh, you don't need either a critical illness policy or a disease-specific policy."

Adds Pankaj Mathpal, Mumbai-based certified financial planner: "A combination of comprehensive health insurance plan and super top-up is a good idea for augmenting the sum insured. If you are not suffering from a heart ailment, but have a family history of the disease, buy a critical illness plan."

Some experts are of the view that given the rising incidence of cardiac diseases, most people would be better off with a combination of comprehensive health insurance plan and critical illness cover.

"While the indemnity cover will take care of hospitalisation expenses, the fixed-benefit plan will compensate for the loss of income during the recovery period," says Mayank Bathwal, chief executive officer, Aditya Birla Health Insurance.

Feature Presentation: Aslam Hunani/Rediff.com