If you do decide to invest in the under-construction project of a mid-level player, check his financials. Avoid heavily-leveraged ones, advises Sanjay Kumar Singh.

Patna-based businessman Rohit Karna, 50, and his school teacher wife Garima, 46, have been scouting for an apartment in the National Capital Region (NCR) for the past six months.

The news of the crisis in non-banking financial companies (NBFCs) and the consequent fund crunch real estate developers are facing has got the couple worried.

"When you go house hunting, you see so many projects where construction been at a standstill for some time. If fund supply to the sector grows tighter, more projects could meet the same fate," says Rohit.

The Karnas have decided to proceed only after weighing all their options.

Liquidity crisis stifles recovery

Experts say the liquidity crisis, which began from around September 2018, has put an end to the nascent recovery in sales.

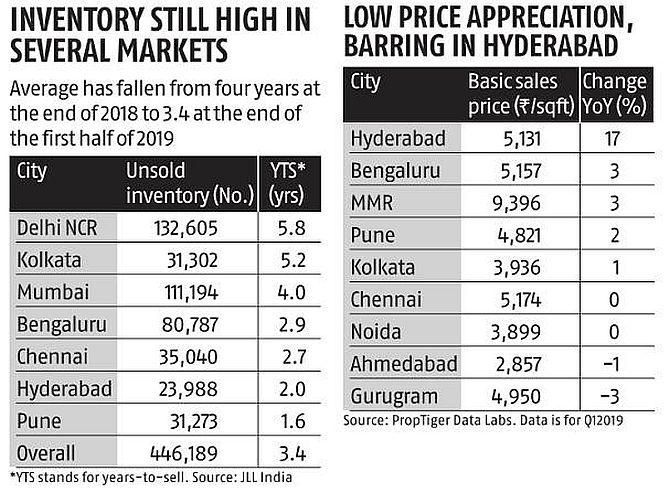

The market is saddled with a large number of heavily delayed or terminally stuck projects.

"Currently, 1.74 lakh homes in 220 projects are stalled across the top seven cities. There are more in the smaller cities. Their collective value is a staggering Rs 1,774 billion. Of the stalled units, 66 per cent or over 1.15 lakh units have already been sold," says Anuj Puri, chairman, ANAROCK Property Consultants.

He adds that the predominant reason is the lack of liquidity with developers.

With banks saddled with non-performing assets (NPAs), NBFCs had stepped into the breach.

From Rs 64,000 crore in 2011-12, credit by NBFCs/HFCs (housing finance companies) to developers increased by more than 3.5 times to about Rs 233,000 crore in 2017-18.

Lending by NBFCs/HFCs slowed down considerably in October-March 2018-19.

"Net disbursals by NBFCs/HFCs to developers declined by almost half from Rs 52,000 crore in 2017-18 to an estimated Rs 27,000 crore in 2018-19," says Samantak Das, chief economist and head of research & REIS, JLL India.

NBFCs/HFCs have put in more stringent guidelines for lending.

"Interest cost charged from developers is also moving up," says Gagan Randev, national director, capital markets and investment services, Colliers International India.

The silver lining is that funding has not stopped entirely.

"At a recent event, big institutional investors said they are still willing to lend to developers who have managed their balance sheets well," says E. Jayashree Kurup, head-content and advisory, Magicbricks.

Das adds that small and medium NBFCs/HFCs continue to lend, but the ticket size of their loans is smaller.

NHB ban on subvention schemes

The National Housing Bank (NHB) recently directed HFCs to avoid extending housing loans where developers service the loans on borrowers' behalf.

According to Mani Rangarajan, group chief operating officer, Elara Technologies (which owns Housing.com), "About 30-35 per cent of sales in new launches were through subvention schemes."

A low-cost source of financing has closed down for developers.

"Developers were able to get financing at 9-10 per cent via this route, compared to the 13-20 per cent they have to pay if they borrow from the debt market," adds Rangarajan.

Private equity funding for real estate developers had already dried up in the wake of the NBFC crisis, according to Puri, and now one more funding avenue has been shut down.

Randev adds that second-tier developers, who relied more on subvention schemes, will find the going difficult.

Buyers benefited from these schemes by just making the down payment after which they did not have to worry about making further payments till possession.

Many buyers who may not be able to bear the burden of both rent and pre-EMI could postpone their purchases.

Rangarajan says developers have gone back to the drawing board and may come up with alternative offers over the next 15-30 days.

Ready-to-move-in is risk-free

In the current environment, inexperienced and risk-averse investors should opt for ready-to-move-in properties.

"You are able to circumvent development risk and you also don't have to pay goods and services tax on a ready house," says Randev.

Such properties are costlier than under-construction ones, but not too much more.

"The difference is not more than 5-8 per cent in today's market," says Kurup.

She says you can offset this difference by negotiating for discounts and freebies.

Das says that the premium paid for ready properties will partly be offset by the fact that you stop paying rent right away.

Under-construction projects require due diligence

The current issues of the sector have not affected all developers equally.

"Strong, financially sound players will not only complete their projects but also launch new ones. They will even get private equity backing for them. Under-construction projects by them can be considered," says Puri.

He suggests avoiding under-construction projects by smaller developers with no visible construction progress.

If you decide to invest in the under-construction project of a mid-level player, check his financials (easily available for listed players).

Avoid heavily-leveraged ones.

In case of unlisted players, go to the web site of the state Real Estate Regulatory Authority (RERA).

It will have information on the developer's project portfolio.

"Any developer who has three or more projects scheduled for completion in the next year is going to need a lot of working capital. Going with such a player would be a risk," says Kurup.

Also check the developer's track record of completed projects.

Ask him whether he has got project funding.

The web site of the Registrar of Companies also has information on loans given by various entities to developers, informs Randev.

Finally, visit the project site to check the pace of construction.