A lot will depend on how the equity markets in the US play out in April-May this year. A correction there, long overdue, could change all the variables in the current equations, says Sonali Ranade.

The story of currency markets since July 2012 to December 2013 can be explained by the depreciation of the yen. In the 17-month period from July-end 2012 to December-end 2013, the yen depreciated by roughly 55 per cent against the euro and 35 pc against the US dollar. In the same period, the euro appreciated by about 16 pc against the US dollar. Yen’s weakness rather than anything else has been driving currency markets. This may continue for a while longer as Abenomics plays out fully in Japan and China.

The second thing to note is that 10-year yields on US treasury notes are about to break above 300 bps and head towards 380 bps over the next six months. Some of this may already be priced into the equity markets but we can be sure not all of it is in the price. On the other hand, equity markets may actually view an increase in long-term interest rates as confirmation of growth at least to begin with. The impact of rising interest rates on the US dollar may also be muted to begin with since other rates too are likely to rise with the exception of Japan.

Back in India, the attention will remain focused on the US dollar which is likely to weaken modestly against the euro but strengthen against the yen over the next few months, ie, till mid-April 2014. However, the USD-INR charts show that the first leg of the correction to the run up to 69 may be over, and the dollar could move in the next few weeks to test the overhead resistance at 64 albeit gradually. A vault over 64 may take a while though as the second leg of the correction kicks in.

A lot will depend on how the equity markets in the US play out in April-May this year. A correction there, long overdue, could change all the variables in the current equations. I shall have more on that in the second half of the week.

Happy New Year to all.

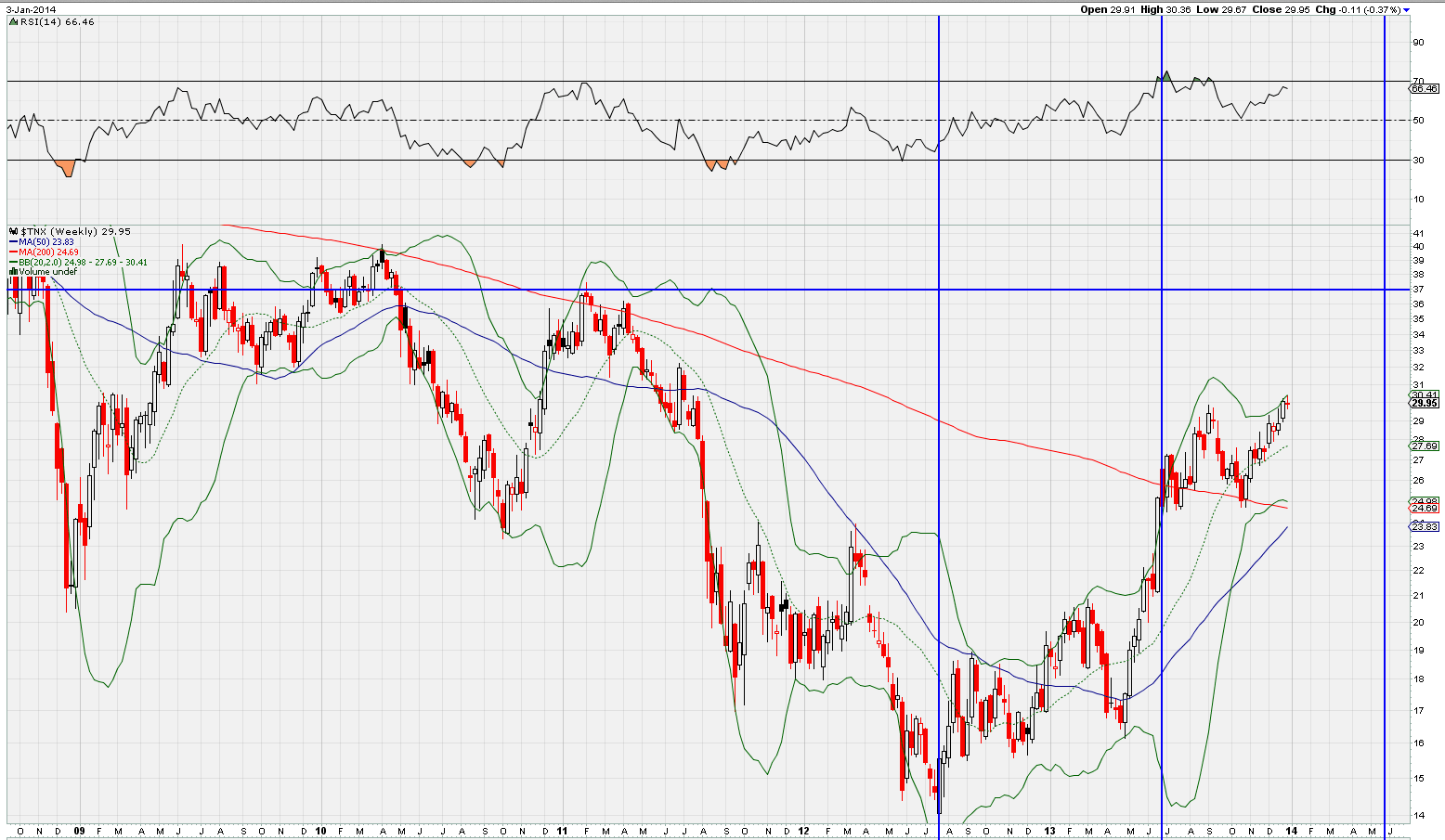

YIELD ON 10-YEAR TREASURY NOTES

YIELD ON 10-YEAR TREASURY NOTES

I have put up the long-term weekly chart of yields on 10-year Treasury Notes [$TNX] in order to show where we are headed in terms of interest rates on US treasuries. Note the current yield on 10 year Treasuries is exactly 300 bps.

On a weekly basis, the yield has breached the previous top at 295 bps and has fallen back a bit to test it as support. The yield has more robust support at 285 bps. My sense is that after a few days of consolidation, we are likely to see yields move up 320 bps or higher. On the price charts the price of treasuries could fall 118 from the current level of 123.50.

Though significant by itself, as it confirms a long-term upward shift in interest rates, the move may not impact equity and currency markets all that much since it is widely expected. Nevertheless, the market’s reaction to a move above 300 bps in yields would be fraught with interest.

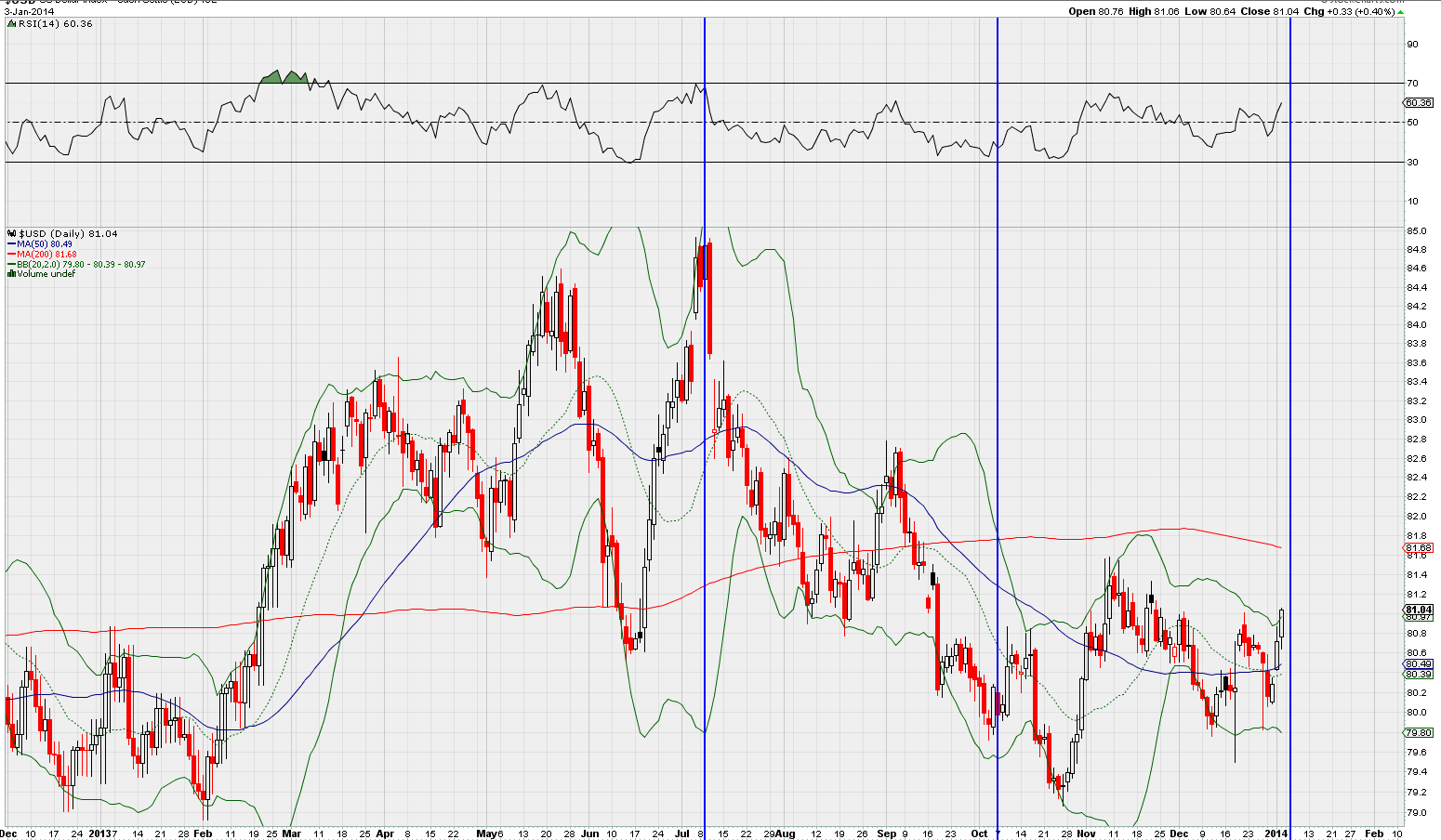

DXY

DXY

The US Dollar is placed in a zone from where it can shoot for $DXY 90 or dive for $DXY 70 with equal range and more or less equal probability. The Index closed at 80.9550 on January 3, 2014, and is one of the most difficult currencies to call at this point.

The Index’s 200 DMA lies above at 81.65 while the 50 DMA lies below at 80.52. I would be reluctant to call the currency either way until it decisively breaks below 79 or above 82. That said my sense of the long-term trend in the Dollar is that [a] it bottomed out at 71.88 on April 21, 2008, and [b] that it is correcting down in an orderly impulse wave starting from the top of 88.46 made on June 7, 2010.

With that larger picture in mind, a correction is under way from the top of 84.78 made on July 9, 2013 mid-April 2014. For the near term, $DXY can shoot for 81.68, its 200 DMA but is unlikely to sustain above it. My sense is the Index will nick the average and head down again for a retest of 79 before it makes up its mind on the direction in which to head. I am bearish on $DXY till Mid-April.

A word of caution is in order. The $DXY can compress going forward or show extreme volatility. Compression would be a bullish indicator, while extreme volatility with a mean of 80 would be bearish. That is best that I can do at this point.

EURUSD

EURUSD

The EURUSD is an uptrend from a low of 1.20 made in August 2012. The uptrend has a target of 1.4250 ending mid-April 2014. The pair’s 200 DMA lies well below the current level of 1.35870 at 1.33. The 50 DMA is currently placed at 1.36, just a bit above Friday’s close. The current correction from the top of 1.3892 made on December 17, 2013, in no way threatens the long-term uptrend.

That said, the EURUSD is likely to find support at 1.3550 and that support is followed by more robust support at 1.3450, which is unlikely to be breached. I expect EURUSD to turn up again from 1.3450 or above and head right back up to challenge 1.40 again. 1.40 is an important overhead resistance that may take more than three or four attempts to take out. But that’s the direction in which EURUSD is headed as soon as the current short correction ends.

USDJPY

USDJPY

The Dollar has been in a major uptrend against the Yen from a low of 75.6 made on October 28, 2011, and that uptrend has a target of 110 Yen and is intact. The 200 DMA of USDJPY is placed at 99.45 Yen while the 50 DMA is currently at 101.7. Both the averages are well below Friday’s close of the Dollar at 104.82.

USDJPY took out the previous top of 103.70 made on May 22, 2013, in the current rally making a top of 105.440 on January 2, 2014. The current correction is little more than one intended to test the last top as the new support.

With that in view, first support from the current level lies at 103.50 followed by a more robust support at 101.50. My sense is the Dollar might take a breather around 103 for two to three weeks before heading right back to 105 and above. ‘Abenomics’ is determined to run the full course and it’s probably the right thing to do for Japan at this point.

EURJPY

EURJPY

As the euro is strengthening against the US dollar, and the Yen is weakening against the US Dollar, we take a look at the EURJPY, the price of Euro in Yen, to check if the trends in place bear out the prognosis for the US Dollar.

The Euro has been on uptrend against the Yen since the last week of July 2012 from a level of 94 Yen. It topped out recently at Yen 145.67 in last week of December 2013, showing an appreciation of 55 pc over 17 months.

During the same period, the US Dollar appreciated against the Yen going from 78 Yen in End July 2012 to 105.25 in December 2013 showing an appreciation of 34.94 pc.

Meanwhile, the Euro appreciated against the US Dollar during the same 17-month period going from 1.20 to 1.390, showing an appreciation of 15.83 pc.

Putting it another way, it would appear that it is the deliberate weakening of the Yen that is driving the markets over the last 17 months and not Fed actions such as they are. Policy action in Yen explains most of the moves in both Euro and the US Dollar.

A word of caution is due, though. The 110 Yen to the US Dollar is a formidable overhead resistance and the wave counts favor a consolidation over the weeks ahead. But such consolidation is likely to be well above 100 Yen to the US Dollar.

USDINR

USDINR

After topping at INR 68.80 on 8/28/2013, the Dollar has been correcting and has twice successfully bounced off the bottom at INR 61. I think the correction was completed at a low of INR 60.83 on December 9, 2013, and since then the Dollar is an uptrend with a target of INR 64.

Within the uptrend to INR 64, my sense is that Dollar completed wave [a] at INR 62.48 and wave [b] at INR 61.71 and on topping 62.50 over the next few days, will head for 64 or slightly higher.

Over a longer-term horizon, I think the long-term uptrend in the USDINR remains firmly in place. The pair’s 200 DMA lies well below at INR 60 while, the 50 DMA is at 62.12 and the Dollar closed Friday at INR 62.18, just a touch above the 50 DMA.

The Dollar may well turn down in world currency markets, especially against currencies such as the Euro and Yuan. But as far as the USDINR market is concerned, it is decidedly in a long-term uptrend. Don’t shade the Dollar using INR.

NB: These notes are just personal musings on the world market trends as a sort of reminder to me on what I thought of them at a particular point in time. They are not predictions and no one should rely on them for any investment decisions.

Sonali Ranade is a trader in the international markets.

.jpg)