The Indian stock market is scaling new highs every week on expectation of faster economic growth but across the border, in China, faster growth has not translated to a stock market boom.

In the past five years, the Shanghai SSE 180 index is up only 25 per cent against a cumulative 175 per cent rise in the BSE Sensex during the period. In the past 12 months, the Sensex has rallied by 35 per cent against flat movement in the SSE 180.

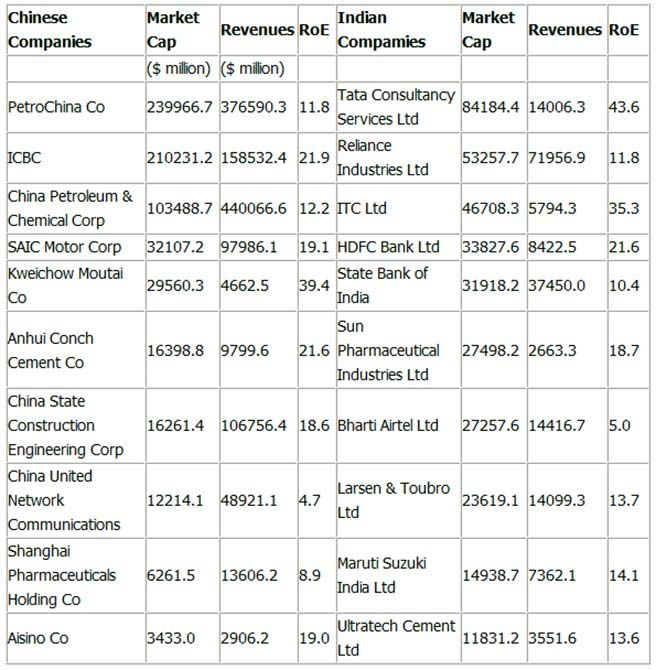

This has resulted in a huge gap in the valuation of top Indian and Chinese companies, across sectors. On average, SSE 180 companies are half as valued as their Indian peers. The Shanghai stock exchange benchmark index is valued at only 7.7 times the trailing 12-month earnings.

The corresponding ratio for the Nifty 50, benchmark of the National Stock Exchange here, is 18.6 times the combined trailing earnings for its constituent companies.

Part of the explanation is the higher return on equity (RoE) for Indian companies. The weighted average RoE for Nifty 50 companies was around 15 per cent higher than the 10 per cent for SSE 180 companies last year.

The analysis is based on the current market capitalisation and past 12-month earnings of the companies that are part of the Nifty 50 index and Shangahi SSE 180 index. It excludes eight Chinese companies whose latest 12-month finances were not available.

Most of the top Chinese companies are now trading at a fraction of the valuation enjoyed by their Indian counterparts. China’s largest automobile maker, SAIC Motor Corp, is trading at 7.3x its trailing 12-month net profit.  In contrast Maruti Suzuki, this country's top car maker, is trading at 31.6x; Tata Motors is trading at 13x its trailing 12-month earnings. SAIC is currently valued at a little over $32 billion, less than a third of its past 12-month revenues of $98 billion. Maruti Suzuki is valued nearly twice its revenues, despite SAIC's higher RoE (19.1 per cent versus Maruti's 14.1 per cent).

In contrast Maruti Suzuki, this country's top car maker, is trading at 31.6x; Tata Motors is trading at 13x its trailing 12-month earnings. SAIC is currently valued at a little over $32 billion, less than a third of its past 12-month revenues of $98 billion. Maruti Suzuki is valued nearly twice its revenues, despite SAIC's higher RoE (19.1 per cent versus Maruti's 14.1 per cent).

China’s largest lender, Industrial and Commercial Bank of China (ICBC), is trading at 5.7x its trailing earnings.

In comparison, State Bank of India is valued at 13.6x its trailing earnings. HDFC Bank, this country’s most highly valued one, is trading at 23.4x its trailing 12-month earnings. Chinese banks are, however, more profitable than Indian counterparts, with average RoE of 20 per cent against 15 per cent here.

China’s top fast moving consumer goods company, Kweichow Moutai Co, is valued at only 12 times its trailing earning, a fraction of the 30x price to earnings (PE) multiple enjoyed by India’s top consumer goods companies such as ITC, Hindustan Unilever and Asian Paints.

Similarly in cement, India’s top manufacturers are now the most expensive in the world, trading at nearly 25-30x their trailing earnings. In contrast, the PE multiple of China’s top cement makers is in single digits.

Analysts attribute the valuation gap to the difference in the investors’ growth perception about the two markets. “GDP growth in China has dropped from 10 per cent per annum to seven per cent now and is expected to fall further. In India, growth bottomed out at 4.7 per cent in FY14 and is now expected to rise. This translates into faster earnings growth for Indian companies compared to Chinese ones,” says Motilal Oswal, chairman of Motilal Oswal Financial Services.

Valuation in China is also depressed due to the dominance of government-owned companies.

In a recent study by CLSA, there were only three government-owned companies among the top 10 most valued ones in India. The corresponding Chinese list has seven government enterprises.

State-owned enterprises continue to dominate the Chinese economy, unlike in India, where public sector undertakings are declining in importance and are largely absent from high growth and high value sectors such as information technology, pharmaceuticals and comsumer goods,” says Vishesh Chandiok, national managing partner, Grant Thornton India LLP. Government-owned enterprises command lower valuations worldwide.

Beside, the SSE 180 has a higher weightage of state-owned banks, commodity companies and real estate ones.

Typically, these sectors command lower valuations. “Investors fear a big NPA (bad loans) problem for Chinese banks and its contagion impact on the economy and the corporate sector if the economy slows further. This has also contributed to lower valuations,” says G Chokkalingam, head of Equinomics Research & Advisory.

The Chinese stock market also faces heat from currency appreciation. “The yuan is appreciating against the dollar, eroding Chinese competitiveness in many sectors like textiles. This is working in India’s favour, where the currency has depreciated significantly vis-a-vis the dollar in the past five years,” says Oswal.

The Chinese stock market also faces heat from currency appreciation. “The yuan is appreciating against the dollar, eroding Chinese competitiveness in many sectors like textiles. This is working in India’s favour, where the currency has depreciated significantly vis-a-vis the dollar in the past five years,” says Oswal.

Note: Revenues during 12 trailing months ending June 2014

Price to earning multiple latest, Return on equity for latest financial year

.jpg)