'FDs should hold your emergency funds, equivalent to around 6-12 times your monthly expenses.'

The Reserve Bank of India began its battle against inflation with an off-cycle hike in key policy rates on May 4.

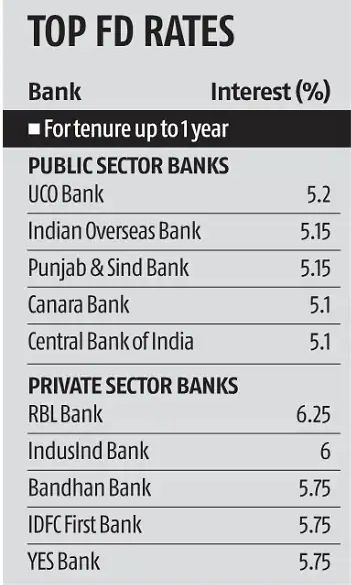

Taking a cue, banks such as Kotak Mahindra Bank, Axis Bank, Punjab National Bank, and non-banking financial companies (NBFCs) such as Bajaj Finance, and several others, have hiked interest rates on fixed deposits (FDs).

How much more can rates rise?

"The repo rate is expected to increase by another 75-100 basis points (bps) over the next 12 months. FD rates should also follow a similar trajectory and rise by 60-80 bps over this period," says Vibhor Mittal, chief business officer of fixed income, CredAvenue.

Credit offtake is a key factor that will determine how far FD rates climb.

"If credit demand continues to rise, banks will have to raise FD rates to attract more deposits and cater to increased credit demand," says Naveen Kukreja, CEO and co-founder, Paisabazaar.com.

Safe haven against volatility

Investors should use FDs as a safe haven against volatility.

"Suppose that you have invested in equity mutual funds for a long-term goal. As your goal approaches, you should move money from equity funds to FDs. This will ensure that market fluctuations don't deplete your corpus and jeopardise your goal," says Adhil Shetty, CEO, BankBazaar.

Yielding negative real returns

Consumer price index (CPI)-based inflation for April came in at 7.8 per cent.

"In such a scenario, FDs will continue to offer negative real returns," says Mittal.

While conservative investors would have welcomed the recent increase in FD rates, experts say overdependence on them should be avoided.

"Only the amount needed for routine expenses should be parked in FDs. The rest of the portfolio should be parked in better-yielding instruments," adds Mittal.

FDs work well for near-term financial goals, such as saving for children's school fees or a vacation. Emergency funds may also be parked in them.

According to Shetty, "FDs should hold your emergency funds, equivalent to around 6-12 times your monthly expenses. The rest of your portfolio should be spread across various asset classes to maximise returns."

Remain at the shorter end

Investors should currently avoid locking in their money in FDs for the long term.

"As FD rates are expected to increase continuously over the short term, depositors should select tenures of one-two years. This will allow them to renew their maturity proceeds at higher rates," says Kukreja.

Also avoid the auto-renewal facility while booking an FD.

"At the time of maturity, this will give you the opportunity to manually select the optimal tenure after factoring in your investment horizon and the highest rate slab available," adds Kukreja.

Another strategy investors can employ is to ladder their FD investments.

"Laddering will take care of liquidity issues," says Shetty.

Laddering can also help average out interest-rate fluctuations.

Alternative investments

Equity mutual funds are good instruments for achieving long-term goals.

Despite their volatility in the short term, they are likely to offer better returns than FDs over seven years or more.

On the fixed-income side, salaried employees should make full use of Employees Provident Fund (EPF), which is currently offering 8.1 per cent.

Public Provident Fund (PPF), which is currently offering 7.1 per cent, is open to both salaried and self-employed persons.

Senior Citizens Savings Scheme (7.4 per cent), Floating Rate Savings Bonds issued by the RBI (7.15 per cent), Sukanya Samriddhi Account (7.6 per cent) are other long-term products that may be used.

Be mindful of the lock-in periods in these instruments.

If you want liquidity, and the benefit of indexation, invest in shorter-duration debt mutual funds of up to one year.

While the returns from these instruments have averaged about 3-3.5 per cent over the past year, their returns will improve as interest rates rise and their portfolios get reinvested in higher-yielding bonds.

Feature Presentation: Aslam Hunani/Rediff.com