Instead of only focusing on the tenure for which the best interest rate is available, investors should also focus on their own investment horizon.

After six consecutive repo rate hikes, the Reserve Bank of India's Monetary Policy Committee opted for a strategic pause last month, holding the benchmark lending rate firm at 6.5 per cent.

Fixed deposit investors are trying to assess whether interest rates have peaked and if this is a good time to lock into FDs for the long term.

Experts caution that the RBI has only indicated a pause on interest rates, and not a pivot.

Vishal Dhawan, board member of the Association of Registered Investment Advisors , says, "Depending on incoming data, both domestic and international, this may change."

While some experts believe there is still scope for rates to inch upwards, others are of the view they will begin to trend downwards in six to eight months.

Multiple tenures

Should you be governed purely by the interest rates when selecting the tenure of FDs, or should there be other considerations as well?

Even though interest rates across multiple tenures may not be drastically different from one another (due to a flat yield curve), experts suggest locking into FDs of differing tenures at this juncture.

Dhawan says, "You should do so to get the benefit of laddering and thereby mitigate reinvestment risk on maturity."

Instead of only focusing on the tenure for which the best interest rate is available, investors should also focus on their own investment horizon.

If you park your money in a longer-tenure FD but have to break it midway, the purpose will be defeated.

Adhil Shetty, CEO, Bankbazaar, says, "Most FDs carry a penal interest of 1 per cent if you break them prematurely."

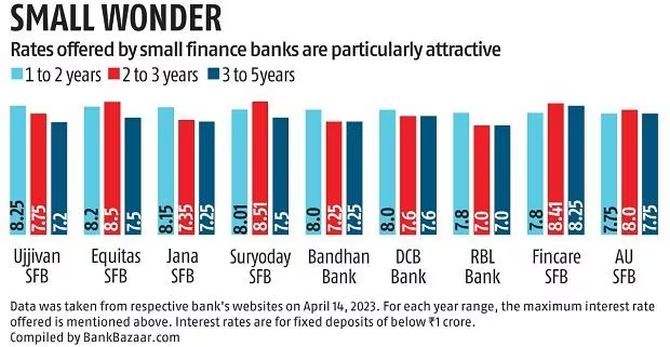

Large banks or SFBs?

Small finance banks (SFBs) are currently offering mouth-watering returns on their FDs.

Deepali Sen, founder and partner, Srujan Financial Advisers, says, "Risk-averse investors may avoid them. Only those prepared to take some risk should go for their FDs."

Investors who opt for FDs of SFBs should limit their total deposit in each SFB to Rs 5 lakh, the limit for deposit insurance.

Exposure to SFBs' FDs should also not exceed about 20-25 per cent of an investor's total FD holdings.

Diversify across fixed-income options

Instead of confining themselves only to FDs, investors should consider other fixed-income options as well.

According to Pankaj Shrestha, head of investment services, Prabhudas Liladhar, "Debt mutual funds, tax-free bonds, RBI floating-rate bonds (taxable), and G-Secs are good alternatives to FDs currently."

Although debt mutual funds are no longer eligible for indexation benefit on long-term capital gains, investors should still consider them.

If interest rates decline, these funds could see mark-to-market gains.

Shrestha says, "Tax is not deducted at source in debt MFs, which is an advantage for buy-and-hold investors."

He also suggests investing in target maturity funds, which invest in safe debt securities.

Investors can also know the indicative yield of these funds at the time of investment.

Investors in the higher tax brackets may consider tax-free bonds.

Sen suggests opting for AAA-rated corporate FDs of top-notch companies. Bear in mind, however, that these FDs offer lower liquidity than bank FDs.

RBI floating rate saving bonds offer 35 basis points more than National Savings Certificates.

Now that rates of NSC have been hiked to 7.7 per cent for the April-June quarter, these bonds are expected to start offering 8.05 per cent.

"Invest in them if you have a horizon of seven years," says Shrestha.

What should a senior citizen do?

Senior citizens tend to depend heavily on FDs for their regular cash flows. Experts suggest they should lock in money for a longer tenure.

Colonel Sanjeev Govila (retd), a Securities and Exchange Board of India-registered investment advisor and CEO of Hum Fauji Initiatives, a financial planning firm, says, "If you don't need the liquidity, then lock in money for a longer tenure."

"Interest rates are expected to trend downwards in six to eight months," explains Colonel Govila. "If you enter shorter-duration FDs now, you will have to reinvest at a lower rate of interest when they mature."

Those who may have liquidity requirements should, however, ladder their investments.

Disclaimer: This article is meant for information purposes only. This article and information do not constitute a distribution, an endorsement, an investment advice, an offer to buy or sell or the solicitation of an offer to buy or sell any securities/schemes or any other financial products/investment products mentioned in this article to influence the opinion or behaviour of the investors/recipients.

Any use of the information/any investment and investment related decisions of the investors/recipients are at their sole discretion and risk. Any advice herein is made on a general basis and does not take into account the specific investment objectives of the specific person or group of persons. Opinions expressed herein are subject to change without notice.