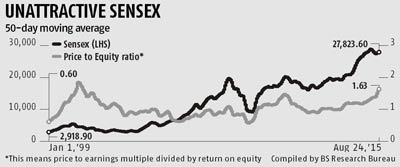

At 1.6, the price-to-equity multiple is at a 15-year high; the index’s return on equity is down to a record low of 13.5%; catching the bottom fish best avoided

Though there is a temptation to bottom-fish after a major market crash, retail investors would do well to steer clear of choppy waters. When adjusted for underlying earnings and return on equity, Dalal Street remains expensive.

The benchmark Sensex’s price-to-equity ratio (price-to-earnings multiple divided by the underlying return on equity) is at a 15-year high and just shy of its peak during the 2000 dot-com bubble. The ratio is now 1.6, higher than during previous market highs.

During the dot-com bubble, it had touched a high of 1.9. This is due to a combination of the Sensex’ higher valuation and a fall in return on equity.

This is due to a combination of the Sensex’ higher valuation and a fall in return on equity.

The index companies’ return on equity is now down to 13.5 per cent, the lowest in about 20 years.

By comparison, the index is trading at 20.5 times its trailing 12-months earnings, similar to valuations during previous highs.

Historically, the index tends to correct whenever the price-to-equity ratio remains above one for a sustained period; the market rises if the ratio falls below one. For instance, the ratio had reached a high of 1.5 on the eve of the 2010 market correction, while it was 1.2 on the eve of the January 2008 correction.

By comparison, it was less than one for around a year in the run-up to the 2003-2008 bull-run; it fell to an all-time low of 0.6 after the Lehman Brothers-triggered market crash, fuelling a recovery.

“Valuations haven’t become mouth-watering, despite the recent correction.

"The market could fall if the global economic environment turns choppy,” says Anoop Bhaskar, fund manager and head (equity), UTI Mutual Funds.

He doesn’t expect a strong recovery either, given the subdued earnings growth.

“Stock prices are not expected to recover in a hurry, with the likelihood of a poor earnings growth in the second quarter,” he says.

Others point to the severity of the current business cycle.

“The current business cycle is similar to that in the early 2000s, but the stock valuation is closer to 2007 highs, when corporate earnings were growing at 30-35 per cent.

"Now, earnings growth is down to single digits,” says Dhananjay Sinha, head (institutional equity), Emkay Global Financial Services.

According to a study by Emkay Global, the return on assets for Sensex and Nifty companies has been about three per cent since 2008-09, down from about seven per cent in FY07 and FY08. Given this, the odds favour further correction in the benchmark indices and richly-valued stocks, unless corporate earnings deliver in the next couple of quarters.

Given this, the odds favour further correction in the benchmark indices and richly-valued stocks, unless corporate earnings deliver in the next couple of quarters.

“We expect a recovery in corporate earnings in the latter half of this financial year.

"If it comes through, there will be strong support for the market,” says Bhaskar.

Investors should keep in mind that foreign institutional investors are sitting on large profits, as they have been accumulating Indian equity since the March 2015 quarter.

Their first sell-off was during the June 2015 quarter, when they cut their BSE-500 holdings by about 40 basis points to 20.4 per cent.

In March 2009, FIIs owned only 12.6 per cent of BSE 500 companies, on an average.

This raises the possibility of an FII-led market correction in case the global economic environment worsens.

Be the prepared for the buying opportunity that will create.