It's not e-retailers alone. Bankers are also celebrating initiatives like 'Big Billion Day Sale' this festive season.

It's not e-retailers alone. Bankers are also celebrating initiatives like 'Big Billion Day Sale' this festive season.

For, online shopping of physical goods in India is estimated to reach $4 billion in 2014, and multiply by over 11 times to $45 billion by 2020 - reflecting a compound annual growth rate (CAGR) of 50 per cent.

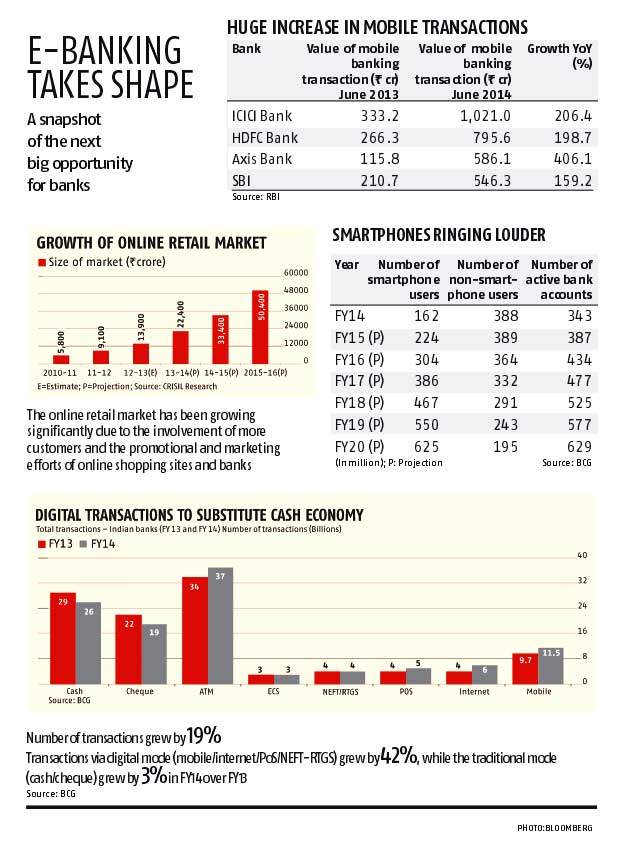

The country's internet population, 213 million as on 2013, is seeing an addition of five million every month, driven by the rapid growth in smartphones. Most banks are cashing in on this opportunity, as it helps them earn revenues and in lowering costs.

Bankers explain every time a card is used online, the issuing bank earns, on an average, 1-1.5 per cent of the amount spent.

The earnings can be higher, depending on the amount spent and type of card used. Online transactions also result in cost savings for lenders.

For instance, instead of using the ATM, if a customer performs an online transaction through his mobile phone or computer, the transaction cost for the bank is nearly halved.

The same transaction would cost the bank 10 times more if the customer visits the branch to withdraw cash.

Lenders are increasingly partnering online retailers - a move e-retailers believe is mutually beneficial. While retailers are able to offer a payment gateway provider for purchase of goods, banks gain from increasing use of plastic money.

"Banks gain if they form a tie-up with us as in our marketing exercises, we would also advertise about the cash-backs and rewards available on banks' cards. Also, it is not possible for a bank to reach so many offline retailers," said Vijayendra Singh, managing director at Foodpanda, an online food ordering platform.

Foreign and new-age private sector banks have taken the lead in facilitating e-tailing, the process of selling retail goods on the internet.

Citibank India, for instance, hosts a cyber-sale - OMG! Wednesdays - every fortnight, allowing its debit and credit card customers to avail of deep discounts across six to 10 leading e-commerce merchants across categories.

The OMG! Sale was launched on December 5, 2012 and again in the same month next year. "The OMG! Sale 2013 saw over 800 per cent increase in our cards daily spends, with a 71 per cent jump over the OMG! Sale 2012 spends. Transactions grew four times and web visits increased 44 per cent," Kartik Kaushik, country business manager at Citibank India, said.

Currently, close to 85 per cent of all Citibank customers' financial transactions take place through digital channels.

The bank has a 10 per cent share of payment through IMPS with less than 0.5 per cent share of the total banking accounts. Also, 30 per cent of Citibank customers who log in to its website do so via mobile devices.

Private lenders like HDFC Bank and IndusInd Bank have launched e-commerce sites exclusively for customers.

"We have allowed our bank customers to not only shop online but redeem their points online," said Anil Ramachandran, head of retail unsecured assets, credit cards and personal loan, at IndusInd Bank.

While online travel still has the largest share of the e-commerce market in India, experts believe e-tailing will be the biggest growth driver in coming years.

"Going forward, e-tailing will have an expected CAGR of over 60 per cent... Within e-tailing, fashion is likely to be the driving segment," Motilal Oswal Securities said.

E-commerce also appears to help plastic money gain acceptance. The number of debit card transactions at point-of-sale (PoS) terminals - a majority of which was done online - has more than doubled in four years.

According to the Reserve Bank of India's (RBI) data, the number of debit card PoS transactions was 59.6 million in June 2014. It was 47.6 million a year earlier, and 23.9 million in June, 2011. The volume of credit card PoS transactions also increased twofold to 48.3 million.

Rajiv Anand, president for retail banking at Axis Bank, says: People are shopping online and as a result, debit and credit card usage has gone up significantly. More, e-retailers are providing a swipe machine to customers at the point of delivery.

Experts say technology has played a key role in helping banks exploit the e-commerce boom. ICICI Bank, for instance, has launched as many as six next generation mobile apps in July-September.

Bankers claim digital banking has evolved from basic online banking to a broad set of services and helps lenders strengthen their relationship with customers. Hence, it is no longer a matter of choice for lenders.

"It is not only about making money. The question is whether you should be present in areas where your customers are. If the answer is yes, as a bank you have to offer these services," Prashant Joshi, head of retail banking at Deutsche Bank in India, said.

Sanjay Sethi, founder and chief executive officer of ShopClues, says the growth of e-commerce is dependent on the popularity of online banking. "People who are comfortable doing online banking are the ones who also shop online and vice versa. And, therefore, one is an enabler for the other."

The Regulator’s Do’s And Don’ts

The Regulator’s Do’s And Don’ts

- Firms that route online billing internationally will need to include second factor authentication and will have to route the transactions through a bank in India

- All new debit and credit cards to be issued only for domestic usage unless international use is specifically sought by the customer

- Cards for international usage will have to be EMV chip and PIN-enabled

- More secure infrastructure suggested for online transactions

- A system of alert may be introduced when a beneficiary to an account is added

- Banks may put in place a mechanism for velocity check on the number of transactions effected per day/per beneficiary

- Banks may consider implementation of digital signature for large-value payments

- More secure infrastructure suggested for online transactions

- Banks may explore the feasibility of implementing new technologies like adaptive authentication, etc for fraud detection