The question on who should borrow from the market and whether the borrowing will be under two buckets should be decided by the GST Council, and not by the Centre.

If there is no consensus, there has to be a vote says A K Bhattacharya.

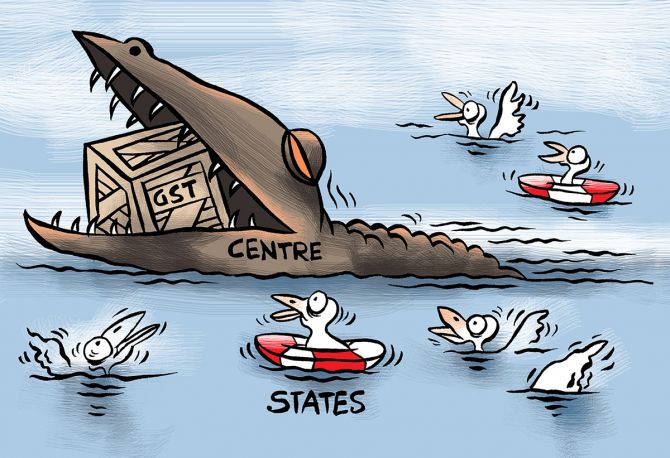

Some states are unhappy over the manner in which the Centre has tried to meet their demand for compensation for the loss of revenues from the goods and services tax in 2020-2021. This has already become a major dispute between the Centre and some states.

How this is resolved will determine not only the future of the country's biggest indirect taxes reform, but also the character of Centre-state fiscal relations and indeed the shape of federalism in India.

The broad nature of the dispute is as follows. The Centre has calculated that the revenue loss for the states, based on the assumption of an annual nominal revenue growth rate of 14 per cent, will be around Rs 3 trillion during 2020-2021.

But the revenue from the GST compensation cess levied for this purpose would not be more than Rs 65,000 crore.

The gap, therefore, is huge.

The Union government has proposed two options.

The first one envisages that the Reserve Bank of India would create a special window of borrowing for the states to help them meet their revenue loss of about Rs 97,000 crore, arising out of the GST implementation problems.

Those choosing this option will also enjoy an additional relaxation in their fiscal deficit target of 0.5 percentage point of their gross state domestic product (GSDP).

The second option envisages that the Centre would help the states access borrowing of Rs 2.35 trillion from the market, but there would be no relaxation in their overall borrowing limit.

In both the options, the levy of GST compensation cess would be extended beyond the transition period of five years, which originally was to end in June 2022.

The additional revenue, as a result, would be used by the states to repay the loans they would have taken.

However, those who opt for the first scheme can use the cess proceeds to repay their interest and principal, but those under the second scheme can use the cess proceeds for repaying the principal amount only.

Why should there be two schemes? The Centre seems to believe that the GST Compensation Act of 2017 was framed to 'provide for compensation to the States for the loss of revenue arising on account of implementation of the goods and services tax'.

The revenue loss on account of GST implementation is estimated at Rs 97,000 crore. Hence, states that opt for the first scheme to borrow this total amount under a special RBI borrowing window will get preferential treatment.

In other words, the Centre seems to be arguing that states opting for an additional borrowing of Rs 1.38 trillion, over and above Rs 97,000 crore, will have to do so at a slightly higher cost to compensate themselves for a loss in revenue on account of an economic slowdown in the wake of the pandemic.

Thus, such states should be treated differently, made to pay the interest cost and should be denied the extra borrowing flexibility.

This is like the Centre attaching conditionality to the two options -- if you stay within the lower borrowing limit, necessitated only by GST implementation problems, you get certain concessions, but if you want to borrow more to compensate yourself for the general revenue shortfall due to the pandemic, you need to pay a price.

It is this differential treatment that is the first reason for the states being upset with the Centre.

This has clearly arisen from a flawed understanding of the GST Compensation Act. The relevant provisions of the law make no distinction between a revenue loss arising out of GST implementation and a revenue loss for any other reason.

Indeed, Sections 3, 6 and 7 of the Act say clearly that the projected revenue for the states will be based on a nominal growth rate of 14 per cent, which is assumed to be the revenue that would have accrued to a state in the absence of the GST.

Treating the states's revenue loss under two different buckets, therefore, can prove to be legally unsustainable.

The second reason for the states's unhappiness is the Centre's argument that it cannot use the Consolidated Fund of India to compensate the states for their revenue loss.

This argument has merit in principle, but has become a little weak after an amendment to the GST Compensation Act carried out in August 2018.

The original law had mandated that the compensation cess would be credited to a non-lapsable fund known as the GST Compensation Fund, which shall form part of the public account of India.

It was also stipulated that half of the amount remaining unused in the Fund at the end of the transition period (June 2022) shall be transferred to the Consolidated Fund of India and the balance shall be distributed among the states in the ratio of their total revenue from their taxes in the last year of the transition period.

But in August 2018, about a year after the GST rollout, the Centre got the GST Compensation Act amended to make a crucial change. It allowed the Centre to transfer from the GST Compensation Fund half of the unused cess collections to the Consolidated Fund of India at any point of time in any financial year, while the remaining half could be distributed among the states.

In effect, the amendment allowed the fungibility of the unused cess collections even before the end of the five-year transition period.

If the unused portion of the cess collections, kept in the public account (GST Compensation Fund) could be transferred to the Consolidated Fund of India at any time of the financial year, surely a reverse flow in times of such a crisis induced by the pandemic should not be frowned upon.

The third and the most important cause of the states's disillusionment with the Centre's approach to the GST compensation issue is the manner in which the spirit of the discussion held at the time of finalising the GST Compensation Act is not being honoured now.

At the seventh meeting of the GST Council, held in December 2016, Arun Jaitley, the finance minister and the chairman of the Council at that time, had made it unambiguous that the compensation for the states should be funded from the cess and if there was any shortfall, it could be 'supplemented by some mechanism that the Council might decide'.

The eighth meeting of the Council, therefore, decided in January 2017 that 'in case the amount in the GST Compensation Fund is likely to fall short or fell short of the compensation payable in any bimonthly period, the GST Council shall decide the mode of raising additional resources including borrowing from the market which could be repaid by collection of cess in the sixth year or further subsequent year.'

So, why is there a dispute?

Earlier GST Council meetings had already decided that market borrowings would be a solution to meet the shortfall in compensation.

The question on who should borrow from the market and whether the borrowing will be under two buckets should be decided by the GST Council, and not by the Centre.

If there is no consensus, there has to be a voting.

In the current situation and the voting methodology (75 per cent approval for a proposal with the Centre having a one-third share of votes and the states having a two-thirds share), the Centre will have to get at least 19 states to come on its side to have its way. This may require some political management by the Centre.

But recent developments and the Centre's approach have made the situation fraught with more difficult problems.

Even if the states unhappy with the Centre's current proposal lose the vote, they would press for the creation of a dispute settlement mechanism within or outside the GST Council.

That would open up a new chapter in India's GST saga.