Expect a more modest out-turn of around 5 per cent (if not less) because of the longer-term scarring effects of the Covid shock, the sharply slowing growth in the pre-Covid years and some scepticism about the growth-efficacy of some of recent official policy initiatives, explains Shankar Acharya, former chief economic advisor to the government.

Ever since the National Statistical Office estimates of 2021-2022 Q1 came out at end August, there has been a lively debate on whether it reflects a V-shaped recovery or not.

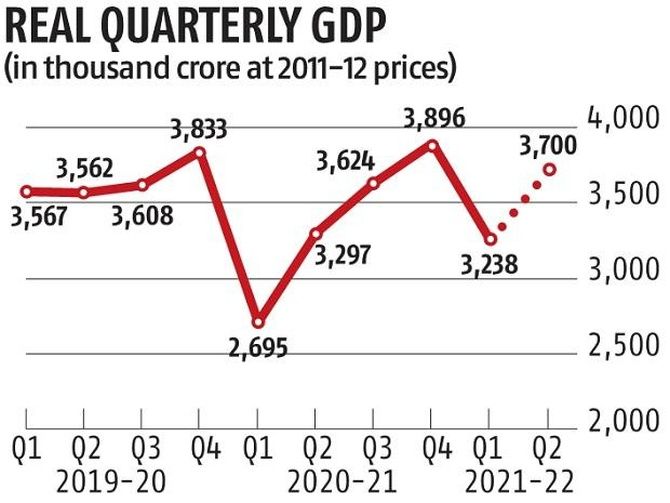

Well, a glance at the figure should answer the question.

It plots the level of real (inflation-adjusted) quarterly GDP as per the NSO since the first quarter of 2019-2020 and includes my guestimate for 2021-2022 Q2.

It clearly supports three statements.

First, the recovery from the deep plunge of April-June 2020 (the brutal downswing of the 'V') was followed by a smart recovery in the next three quarters to restore quarterly GDP to its prior levels.

This does merit the sobriquet of a 'V', even if the upswing was somewhat more leisurely.

Second, with the deadly second wave of the pandemic in March-June 2021, there was another plunge in GDP, which, though not as deep as in the previous year, negated much of the recovery.

Third, based on high frequency data, there is likely to be another robust recovery from Q2 of 2021-2022 (depicted by the dotted line).

Now the picture resembles a somewhat straggly 'W' more than a 'V'. And that may be the final profile unless a strong third Covid wave leads to another drop in GDP.

Based on what we know, there is a widespread consensus that full-year GDP growth in 2021-2022 will likely be in the range of 8-10 per cent, bringing the level of annual GDP back to its 2019-2020 level or marginally higher.

That means the economy will have lost a massive 10-12 per cent of potential growth to Covid and lockdowns.

But the even more important issue is what will happen to economic growth in the medium term, say, the five years, 2022-2023 to 2026-2027? This is where the debate gets sharper.

The optimists (including government analysts) expect a swift reversal to an average of about 7 per cent-plus annual growth and cite the slew of recent policy initiatives undertaken in support.

More bearish independent analysts (like me) expect a more modest out-turn of around 5 per cent (if not less) because of the longer-term scarring effects of the Covid shock, the sharply slowing growth in the pre-Covid years and some scepticism about the growth-efficacy of some of the recent official policy initiatives.

The Covid/lockdown shock has bequeathed at least four lasting scars, which may take long to heal.

First, the informal, non-agricultural segment of the economy, amounting to around a quarter of GDP and around 40 per cent of total employment and populated by many thousands of small, medium and micro producers of goods and services, has been hammered by the Covid/lockdown catastrophe.

For most of them, recovery has been very weak in both output and employment terms (this is the lower arm of the so-called K-shaped recovery); and many have ceased to function, swelling the ranks of the under-employed in agriculture and low-end services.

Getting back to their earlier output/income levels may be a bridge too far.

Second, the macroeconomic effect of their reduced incomes may well be to keep aggregate consumption on a lower path for several years, which, in turn, would have discouraging consequences for aggregate investment.

Third, the two years of deep Covid impact on public finances have led to record fiscal deficits and sharply higher government debt-to-GDP ratios, near 90 per cent.

Global experience suggests such fiscal weakness is rarely conducive to sustained, strong economic growth.

Fourth, Covid consequences have further weakened an already stressed financial system.

The optimists point to the remarkable array of growth-promoting policy initiatives undertaken by the government in the last two years.

I list the prominent ones together with a brief comment in brackets next to each:

- The major restructuring/reform of corporate taxation done in September 2019 (thanks, perhaps to the Covid shock, this has helped swell company profits without spurring much fresh investment).

- The major reforms of agricultural marketing and distribution (these are in abeyance due to political opposition).

- The restructuring of about 30 labour laws into four codes which passed Parliament last year (their implementation awaits the promulgation of the rules, which have to be agreed by central and state governments. Also, some key elements like the level of the national minimum wage remain to be specified; an unduly high rate could stifle employment growth in the poorer regions).

- The recent Budget commitment to privatise non-strategic public sector enterprises (despite a buoyant capital market, progress remains slow).

- The establishment of a 'bad bank', the National Asset Reconstruction Company Limited, to solve, or greatly reduce, the pervasive legacy problem of bad loans in the banking system (this may be a promising initiative, but it has just started).

- The launch, in April 2020, of the government-financed Production-Linked-Incentives (PLI) scheme to accelerate the growth of key manufacturing sectors and their exports (such selective support could turn into a double-edged sword).

- The recently announced Rs 6 trillion National Monetisation Pipeline for public sector assets (the success of this programme depends critically on effective and extended commercial partnerships between the public and private sectors, an arena which has not seen great success in the past decade).

On the negative side, in the important area of trade policy, after a quarter century of phased reductions in India's record high customs duties, government policy has, unfortunately, reversed course in recent years.

Furthermore, in 2019, after seven years of negotiations with 15 other countries in Asia, the government suddenly drew back from becoming a founding member of the mega regional trade pact RCEP (Regional Comprehensive Economic Partnership), thus weakening our potential for stronger trade links and value chains with the proximate and most dynamic regional trading hub in the world.

Hence, the prospects for sustained rapid increases in our exports and imports have been significantly diminished.

Taking all this into account, I see little reason to alter the view I expressed in March this year: 'We shall find it difficult to exceed an average of 5 per cent growth in the medium term'.

Shankar Acharya is Honorary Professor at ICRIER and former chief economic adviser to the Government of India. Views are personal.

Feature Presentation: Rajesh Alva/Rediff.com