In the past 10 years, the Street punished companies that joined the capex bandwagon and rewarded those that chose to stay asset-light.

Early last week, Prime Minister Narendra Modi asked India Inc to take risks and invest more, the idea being that it would boost growth and turn corporate sector's fortunes.

Dalal Street, however, appears to be thinking otherwise.

In the past 10 years, the Street punished companies that joined the capex bandwagon and rewarded those that chose to stay asset-light.

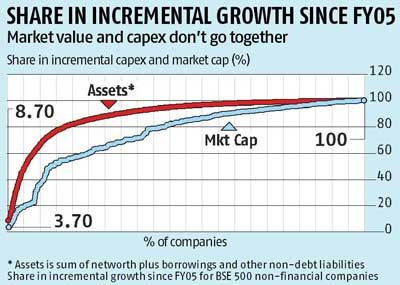

Between FY05 and FY15, only 14 companies accounted for half of the incremental growth in India Inc's capital expenditure (or assets) during the period.

These companies, however, accounted for only a fifth (20 per cent) of the incremental rise in the BSE 500 companies’ (ex-financials) market cap during the period.

The corresponding ratio for India Inc's top 20 investors was 59 per cent and 22 per cent, respectively (see charts).

The list includes big names such as Reliance Industries, Oil and Natural Gas Corporation, NTPC Limited, Tata Motors, Tata Steel, Bharti Airtel, Adani Enterprises, Hindalco, Vedanta and Indian Oil, among others.

The analysis is based on the consolidated financials and financial year-end market capitalisation for BSE 500 companies beginning FY05.

The sample is restricted to 299 non-financial firms whose finances are available for the past 11 years.

For example, RIL, the biggest investor during the period, accounted for 8.7 per cent of the incremental capex in the last decade.

But, it contributed only 3.7 per cent to the sample's incremental market cap.

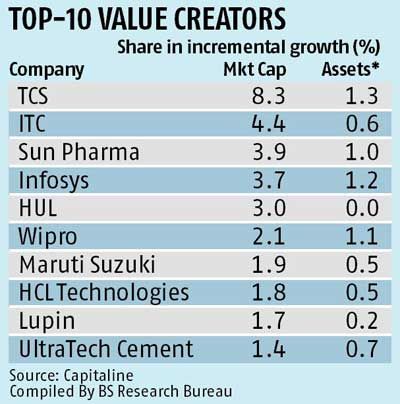

In contrast, Tata Consultancy Services accounted for 8.3 per cent of the incremental growth in the combined market cap, many times larger than its 1.3 per cent share in the incremental capex during the period.

Most of the rise in India Inc's market value was led by asset-light firms such as TCS, ITC, Hindustan Unilever, Infosys, Wipro, Sun Pharmaceutical Industries, Maruti Suzuki, Lupin and HCL Technologies, among others.

In all, only 36 companies (12 per cent of the sample) accounted for two-thirds of the incremental rise in the combined market cap by sharing 54.7 per cent of the incremental capex during the period.

In all, only 36 companies (12 per cent of the sample) accounted for two-thirds of the incremental rise in the combined market cap by sharing 54.7 per cent of the incremental capex during the period.

As on market close on September 4, two-thirds of the market cap was accounted for by companies that control only 40 per cent of India Inc assets.

Interestingly, the past year's stock market rally was accompanied by a relative cut-back in capex by India Inc.

In FY15, India Inc's capex growth was the slowest in a decade -- up by only 5.5 per cent against the 10-year compounded annual growth rate of 20.8 per cent.

The companies' combined market was, however, up 33.5 per in FY15, growing at nearly double the average growth of 17.9 per cent during the period.

Disapproval from the Street aside, there is little economic incentive for India Inc to scale-up investments at the moment.

Return on assets hit a new low of 5.5 per cent in FY15, a third of what it was in FY05 (14.3 per cent) and even lower than that in FY09 -- the year demand was hit by Lehman crisis.

There has been a steady decline in India Inc's asset utilisation as demand failed to match the rising supply. Last financial year, India Inc earned Rs 106 for every Rs 100 invested in their operations -- the lowest in the last decade.

The mismatch has turned many companies into value destroyers for their shareholders -- incremental expense on capex was greater than the addition to their market value.

For example, NTPC added $20 billion (Rs 1.32 lakh crore) to its asset pile last decade.

But, its market cap was up less than half the amount (Rs 50,833 crore or Rs 508.33 billion).

But, its market cap was up less than half the amount (Rs 50,833 crore or Rs 508.33 billion).

The gap was even bigger for Tata Steel at Rs 1.15 lakh crore or Rs 1.15 trillion (rise in capex) and Rs 8,584 crore or Rs 85.84 bllion (rise in market value).

In all, the companies in the sample added Rs 38.2 lakh crore ($600 billion) to their balance sheet, while their combined market value was up by Rs 51.9 lakh crore or Rs 51.9 trillion during the period.

Analysts blame it on the cost associated with capex.

"Capex also means debt and debt servicing eats into the profitability besides raising companies' future cost of capital.

If a company is unable to generate adequate incremental revenues and profits from initial capex, it starts a vicious cycle of lower profitability, rising debt and falling market value," says Dhananjay Sinha, head institutional Equity Enkay Global Financial Services.

Others blame it on the cyclical factors.

"Bulk of the capex is accounted for by commodity producers which have been hit by the global commodity downturn.

"But most of these companies are done with their capex and as soon as the commodity cycle picks up, gains will flow directly into to their bottomline and the mismatch between their balance sheet size and valuations will vanish," says Revati Kasture, head research CARE Ratings.

Image: Stock traders at work. Photograph: Reuters

The image is used for representational purpose only