Analysts remain selective on cement stocks amid the likely government's capex push ahead of the scheduled general elections in May 2024.

While UBS has initiated coverage on the Indian cement sector with an anti-consensus negative view and suggests investors sell select cement stocks on a rally, those at Nomura remain selectively bullish on the sector and prefer companies with large brownfield optionality and multi-region presence.

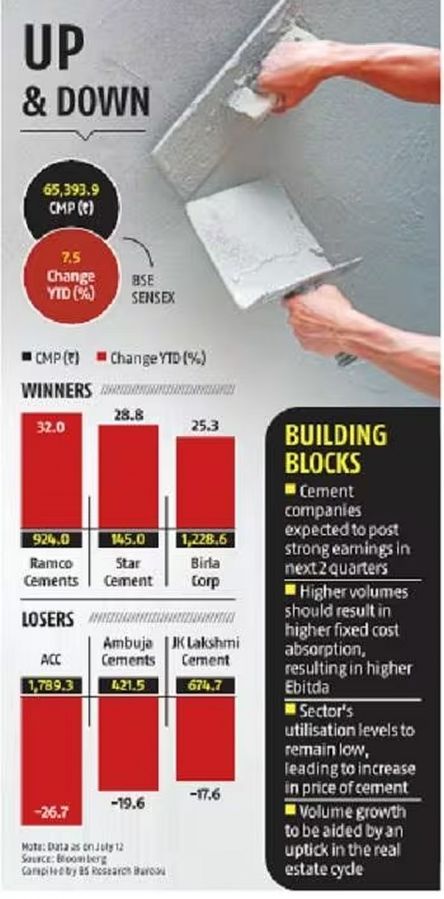

In the near-term, UBS expects strong earnings of cement companies in the next two quarters to be driven by robust demand and margin tailwinds, but suggests any sharp uptick in stock prices could offer a good opportunity for booking profits in the related counters.

“With valuations of 15x one-year forward EV/EBITDA and 30x FY25E PE for a sector tracking close to gross domestic product (GDP) growth rate, rising competition, low entry barriers and return profile of low double digits, we see little room for potential upside. Structurally, we would sell any rally, not buy the dip,” wrote Nikunj Mandowara and Pramod Kumar of UBS in a recent note.

Among the lot, UBS has a 'Buy' rating on ACC, has downgraded Ultratech to 'Neutral' and Dalmia and Ambuja to Sell.

Nomura, on the other hand, has maintained a neutral rating on Ultratech Cement and Ambuja Cements, while maintaining a 'reduce' rating on ACC, Ramco Cement and Shree Cement.

It has initiated coverage on Dalmia Bharat and Nuvoco Vistas with a buy rating.

That said, both UBS (at 10 per cent) and Nomura (8 per cent) have similar forecasts for volume growth in FY24 in the pre-election year, which they feel will also be aided by an uptick in the real estate cycle (housing accounts for 60-65 per cent of cement demand in India).

Higher volumes, Nomura believes, should result in higher fixed cost absorption, resulting in higher EBITDA/tonne, partially offset by weaker realisation given market share tussle amid unbridled capacity expansion by the industry.

“We do not see the industry attaining pricing power in the near-term, as we expect utilisation levels to remain low.

"As a result, we expect prices to increase in line with the wholesale price index (WPI), similar to costs, barring a few episodes of supplier discipline / indiscipline.

"This will keep the ROCE depressed amidst rising capital employed," wrote Jashandeep Singh Chadha of Nomura in a recent report.

Meanwhile, at the bourses, cement stocks have had a mixed run. While Ramco Cements, Prism Johnson, Ultratech Cement JK Cement, Orient Cement and Dalmia Bharat gained between 11 per cent and 41 per cent in the first half of calendar year 2023 (H1-CY23) and outperformed the S&P BSE Sensex that moved up nearly 7.85 per cent during this period, Bheema Cements, ACC, Ambuja Cements, Jaiprakash Associates, JK Lakshmi Cement and India Cements lost up to 75 per cent, ACE Equity data shows.

Consolidation

The chances of consolidation / merger & acquisition (M&A) across the top five cement companies in the near-to-medium term, too, according to UBS, appear slim.

Valuation-wise, the most expensive cement company, Ambuja Cement (standalone), UBS said, is trading at roughly $260 million per tonne of capacity (versus replacement costs of roughly $100 million), while the most inexpensive mid-cap cement stock with sound operational performance and balance sheet is trading at $40-50 per tonne.

“There is limited incentive to sell for the top 6-28 companies and balance sheet strengths provide a buffer to absorb margin hits from weak pricing.

"We, therefore, believe notable market share gains from the top 6-28 companies remain difficult for the top-five firms – organically or inorganically.

"This raises the threat of overcapacity or expansion lagging guidance.

"Both are de-rating risks for an expensive sector in the 90th percentile of its five-year valuation range,” the UBS note said.