To attract capital into infrastructure projects, the ratings system needs a fresh look, says Vinayak Chatterjee.

It is with a certain clarity of purpose that Finance Minister Arun Jaitley raised this rather technical subject in his Budget Speech this year where he talked of, “a new credit rating system for infrastructure projects, which gives emphasis to various in-built credit enhancement structures, instead of relying upon a standard perception of risk which often results in mispriced loans”.

It is with a certain clarity of purpose that Finance Minister Arun Jaitley raised this rather technical subject in his Budget Speech this year where he talked of, “a new credit rating system for infrastructure projects, which gives emphasis to various in-built credit enhancement structures, instead of relying upon a standard perception of risk which often results in mispriced loans”.

This was followed up by another aspect of implementation detailing in the same Budget, which said: “LIC of India will set up a dedicated fund to provide credit enhancement to infrastructure projects. The fund will help in raising the credit rating of bonds floated by infrastructure companies and facilitate investment from long time investors.”

Why did the finance minister have to take a definitive position on ratings for Infrastructure - that too on as important an occasion as the Union Budget speech?

To comprehend the necessity, it is important to first understand the basics.

For those uninitiated with the complex world of ratings, here is a quick primer.

Conventional corporate borrowings are rated according to the format shown below in Table A.

Infrastructure projects, unfortunately, do not get investment-grade ratings generally.

Infrastructure projects, unfortunately, do not get investment-grade ratings generally.

In India, credit ratings given to most of the operational infrastructure projects cluster around BBB levels.

This is because infrastructure projects are traditionally considered riskier by rating agencies, as cash flows arise from a single asset and are perceived to carry higher political and regulatory risks.

The rationale for classifying infrastructure projects around this BBB level are, however, not clear as there is lack of adequate historical data to confirm this.

Research carried out on the UK Private Finance Initiative and European project-financed initiatives has shown that for public-private partnership financing in infrastructure, the likelihood of default may be the same as, or lower than that of, corporate financing because of steady cash flows, near-monopoly market structures, pricing power and low technological obsolescence.

While project loans are supposed to be “non-recourse” (based only on the economics of the specific project), in most cases they are actually backed by collaterals, debt-servicing structures and other full or partial guarantees, which effectively reduce the extent of possible credit loss.

Limited historical data and lack of institutional mechanisms to capture project default data lead to risk loading by rating agencies.

This leads to mispriced loans for projects as well as greater capital requirements for banks and financial institutions.

Access to bond markets remains constrained, and does not allow investment from longer-term sources such as pension and insurance funds, where the stipulated requirements are AAA- or AA-rated securities.

Thus, lower conventional credit ratings lead to poor capital allocation to infrastructure in the economy.

And poor capital allocation from markets based on misplaced ratings is a high cost for India’s infrastructure development ambition, considering that the requirement of debt from non-public sector sources is expected to be in excess of Rs 5 lakh crore per annum.

Clearly, reliance on commercial bank funding is no more the answer.

Infrastructure credit is henceforth going to be heavily dependent on non-bank financial sources and institutions, both domestic and international.

And the use of conventional credit rating methodologies is not working. This is the finance minister’s worry.

Discussions with noted infrastructure finance expert Dhruba Purka-yastha suggest that the solution lies in three broad interventions.

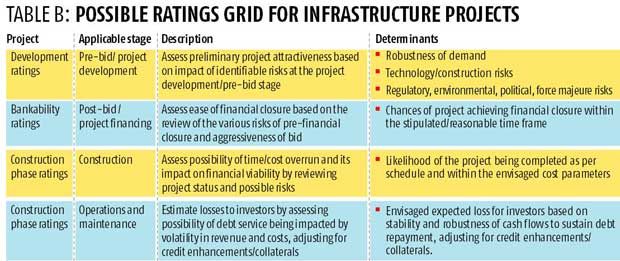

One, a differentiated rating grid structure specific to infra projects could be adopted as illustrated in Table B.

One, a differentiated rating grid structure specific to infra projects could be adopted as illustrated in Table B.

Two, credit enhancement - raising the rating from BBB level to at least A/AA levels by way of a partial credit risk guarantee.

Referring to the Budget announcement, the secretary, Department of Economic Affairs in the finance ministry, said at an industry event in March this year that “the dedicated fund to provide credit enhancement to infrastructure projects will be operational in 2016-17”.

Three, enabling a consortium of domestic institutions to evolve, suggest and adopt a practical and workable scale for infra project ratings.

Assuming all this is in place sooner than later, India will be ready for its next phase of capital market funded infra growth.

The author is chairman, Feedback Infra.