'RBI is already late in addressing inflation pressures.'

"India still is not in stagflation. It is experiencing high inflation pressures. But growth is still expected to be a respectable 7% in FY23, and the latest data from CMIE show that the labour market recovery has picked pace," Priyanka Kishore, Head of India and SEA (South East Asia) Economics tells Rediff.com's Shobha Warrier in the concluding part of a two-part interview.

Your report says you are less convinced that the real policy rate will turn positive as quickly as the market is anticipating. What kind of impact do you foresee in the economy?

I believe the growth-inflation trade-off will turn trickier in the coming quarters, and this will lead the RBI to re-assess the balance of risks once it has unwound the pandemic-related monetary support.

True, inflation is expected to stay above the RBI's target range until Q1 2023. But downside risks to growth have also intensified.

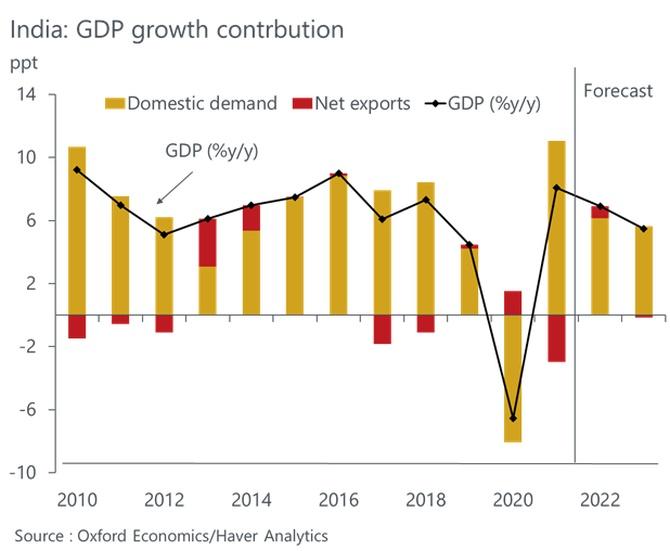

We have recently lowered our FY23 growth forecasts to 7.1%.

In addition to the deteriorating external environment, the downgrade reflects the strained domestic power supply situation and the potential impact of China's lockdowns on India's industrial production.

The Chinese mainland is India's largest import partner and a key source of intermediate inputs for several Indian industries, especially hi-tech.

More broadly, Beijing's approach to containing Covid is increasingly threatening to amplify the global stagflationary shocks generated by the war in Ukraine, the impact of which will be felt in India too.

Do you think the RBI has prioritised inflation overgrowth? Because of the war, India's growth has been downgraded to 4.6% by UNCTAD. What is the best way to fight inflation in such a situation?

The April monetary policy meeting and its minutes clearly highlighted the shift in the RBI's balance of risks to inflation from growth.

I believe this is justified in the current circumstances as price stability is important to achieve sustainable levels of high growth over the medium term.

In fact, one can argue that the RBI is already late in addressing inflation pressures.

Once higher inflation expectations become more entrenched, India may have to sacrifice even more growth in the near term to bring CPI back towards the middle of the 2%-6% target range.

How is the cash reserve ratio hike of 50 basic points to affect the lending cycle which has almost stopped due to the NPA crisis?

Low credit growth is as much a function of demand as supply in my view.

Even with real rates negative for such a long time, credit growth has struggled to gain broad-based momentum.

The pick-up we have seen in recent months can be attributed to relief measures such as loan moratoriums and restructuring that were announced during the pandemic.

While tighter monetary conditions will dent the momentum of credit recovery, I think credit growth will end up being slightly higher in 2022 overall due to the non-monetary support measures in place.

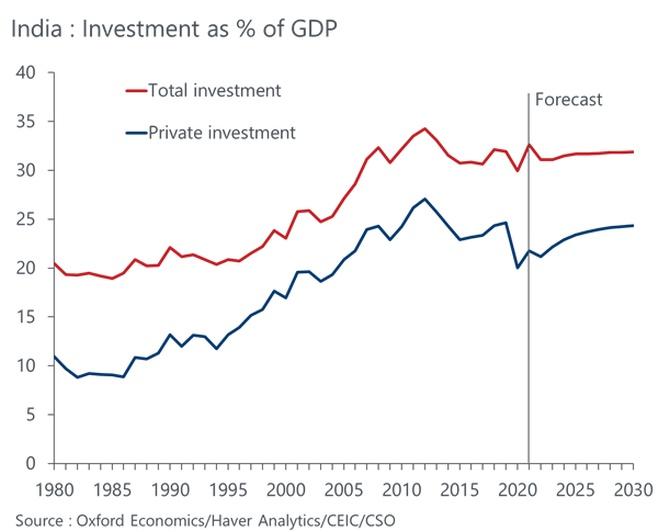

The general complaint of the industry was that there is no demand in the market and that's why private investment is not happening. Do you think the supply-demand situation will get worse in the days to come?

Yes, the outlook for private investment continues to be constrained by weak industrial trends.

High input prices and supply-chain disruptions pose challenges to an already fragile manufacturing recovery.

While legacy balance sheet stresses have eased for large corporations, with the manufacturing capacity utilisation rate still quite low, there is little incentive to invest just yet.

Meanwhile, financial strains could re-emerge for the medium and small enterprises once Covid relief measures lapse.

How different is India's economic situation compared to other countries?

Despite recent downgrades, I would say that India still is not in stagflation.

It is experiencing high inflation pressures. But growth is still expected to be a respectable 7% in FY23, and the latest data from CMIE show that the labour market recovery has picked pace.

India's early decision to start 'living with Covid' has helped sustain domestic demand, albeit this has come at a large humanitarian cost.

But I must add that downside risks to growth have soared due to inflation being elevated for a long time, the electricity shortage concerns, and the worrisome external developments.

These are likely to become more evident as we head into 2023.

We already expect GDP growth to dip below 6% in FY24.

There is also a talk of the US heading for a recession. India escaped the impact of the 2008 recession because of high domestic demand. Now with demand so low and high inflation, what will happen to the Indian economy if a global recession happens?

India will feel the knock-on impact of a global recession.

With the labour market on the mend and catch-up demand in play, especially for services, it may just avoid entering recession itself.

However, growth will likely take a sizeable hit, and conditions could begin to feel recession-like.

Feature Presentation: Rajesh Alva/Rediff.com