FII holding in top listed firms at 10-year high as retail investors, domestic institutions & funds scale down presence.

Indian stock markets are rocking but the number of Indians joining the party is shrinking fast.

While foreign institutional holding in India's top listed companies is at a 10-year high and rising, the exposure of domestic investors, including retail ones, insurance companies and mutual funds, has been declining steadily over the years.

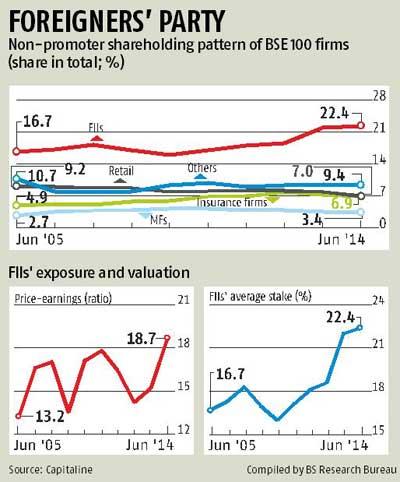

Foreign institutional investors (FIIs) now, on an average, effectively own around a quarter of India's top listed companies, up from 16 per cent five years ago and 16.7 per cent in June 2005.

During this period, retail shareholders' exposure in these companies has declined to 7.2 per cent from 9.2 per cent in 2005 and 8.2 per cent three years ago.

…

Stock ownership of insurance companies like Life Insurance Corporation and mutual funds has declined sharply in the past two years. This period saw the bulk of the incremental rise in FII exposure.

Stock ownership of insurance companies like Life Insurance Corporation and mutual funds has declined sharply in the past two years. This period saw the bulk of the incremental rise in FII exposure.

Between June 2012 and June 2014, FIIs' average stake in BSE 100 companies rose 370 basis points to account for nearly 60 per cent of the entire increase in the past decade.

This more than compensated for a sell-off by domestic investors, leading to a rally on Dalal Street. The result has been a 48.5 per cent rise in the combined market capitalisation of the companies in the sample.

A Business Standard analysis of the BSE 100 companies whose shareholding pattern is available since the quarter ended June 2005 takes into account 81 companies with comparable data.

…

Effective stake or shareholding is derived by adding the value of stake by respective classes of shareholders, based on a company's market capitalisation at the end of June every year.

"Foreign investors are more bullish on India than domestic investors, which, still mourning their losses during the 2008 crash, have moved to gold, real estate and commodities," says Devang Mehta, senior vice-president and head of equity sales at Anand Rathi Financial Services. He expects the trend to change, given an improvement in market sentiment and growth outlook.

Others attribute this to a steady decline in households' financial savings. "For many urban families, the bulk of their income is absorbed by EMIs on home loans, leaving little surplus to invest in equity or mutual funds," says Dhananjay Sinha, head of institutional equity at Emkay Global Financial Services.

It shows in the numbers. In 2012-13, financial assets, including bank deposits, mutual funds, equity, bonds and pension & insurance funds, accounted for only a third of all household savings - down from nearly half in 2006-07, according to data from the Central Statistics Office.

…

The bulls, however, are pinning hopes on the cheer spread by FIIs. "FII investments expand and deepen the market. This expands the investment opportunity for domestic investors subsequently," says Equinomics Research Founder G Chhokkalingam.

In the past 10 years, the rise in FII exposure has gone hand-in-hand with the decline in promoter holdings and rise in free-float; that is, the shares available for trading on the bourses. The average promoter holding in the sample is down to 47.3 per cent from nearly 54 per cent in June 2005.

FII investment has surely energised Dalal Street and expanded India's dollar billionaire's club, but it has also made the indices more vulnerable to global financial volatility.

A gush of foreign capital has led to a re-rating of Indian stocks without any meaningful change in underlying finances. In the past two years, while the market cap of the companies in the sample was up 48.5 per cent, their combined net profit rose only 12.4 per cent.

…

The mismatch pushed stock valuation to a 10-year high. These companies are valued at 18.7 times their latest annual net profits, up from 14.2 times two years ago and 13.2 times in 2004-05.

Experts attribute this to benign liquidity conditions in the developed markets. "Thanks to a low interest rate policy and quantitative easing by the world's top central banks, cost of capital has fallen to historic lows in Europe and North America. This has led to re-rating of Indian markets by foreign investors," says Sinha.

In other words, the same profit now attracts higher valuation. For example, Sensex companies offer an average 15.2 per cent return on their equity, down from the highs of over 25 per cent in 2006-07 but still juicy for top global banks that can borrow dollars at less than one per cent in the London Interbank market for one year. Stability in the rupee-dollar exchange rate in the past six months has further decreased the risk-reward ratio for foreign investors.

The catch is that any bad news could trigger a sell-off, given high valuations. An immediate trigger could be monetary tightening by central bankers that raises the cost of capital.

FIIs now effectively own 46 per cent of all free-floating shares and nearly two-thirds of all institutional holding. A sell-off by them would put tremendous downward pressure on the stock price.

In that case, domestic retail shareholders would be left holding the can, as FIIs have been buying for nearly three years now which gives them a huge price band to book profits; but retail investors, entering only now, are vulnerable.