Investment in market leaders with a safety-first approach could yield reasonable returns across sectors.

Ram Prasad Sahu and Hamsini Karthik report.

Photograph: Adnan Abidi/Reuters

A sharp recovery, after the fall in March, helped benchmark indices post their second consecutive double-digit growth of 15 per cent in 2020.

While defensives such as health care and information technology sectors dominated the returns charts, growth became more broad-based towards the second half with cyclicals, too, catching investor attention.

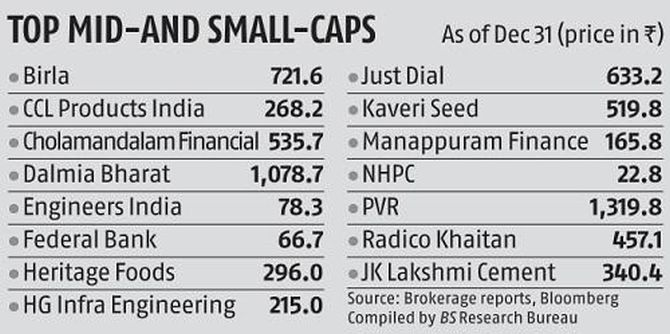

It was not just growth across sectors but down the market capitalisation ladder as well.

After their underperformance over the past couple of years, small and mid cap indices did better than the benchmarks with returns over 20 per cent for the year.

Going ahead, the Street expects strong economic recovery, which is expected to rub off on earnings growth.

In addition to a positive outlook on IT and pharma, analysts expect cyclicals and infrastructure sectors to do well as the capex cycle and investment by the government picks up.

While fund flows continue to be strong, given the sharp rally, investors will have to keep the valuations factor in mind.

With Nifty now trading at 23 per cent premium to the 10-year average, brokerages stress on the need to be selective in the year ahead.

With larger companies gaining market share and the trend expected to be maintained, investment in market leaders with a safety-first approach could yield reasonable returns across sectors.

Also, given multiple levers at their disposal, market leaders are in a better position to absorb the rise in input costs and push up volumes or pass it on to protect margins.

In addition to the most-recommended large caps, we also highlight a few small-caps and mid-caps brokerages included in the portfolios for 2021 due to high growth expectations and attractive valuations.

Bharti Airtel

- The company continues to lead on net additions increasing subscriber count by 3-4 million per month and gaining market share.

- Improving product mix with a higher share of 4G users should lead to higher average revenue per user and margins.

- Price hikes remain biggest trigger and could happen given falling industry subscriber additions and price hike by Vodafone Idea.

- A well capitalised balance sheet and strong execution should sustain its operating performance in the coming year.

- Best placed to gain from sector recovery, say brokerages which is why consensus target price indicates a 31 per cent potential even as the stock has already gained over 30 per cent since mid-October.

Dr Reddy's Laboratories

- After severe pricing pressure over the last five years, the quantum of price erosion is on a declining trend in the US market. Lower drug filings and limited number of US-FDA plants have helped.

- Analysts at Nomura expect the generic launch of vascepa (cardiovascular) and progress on copaxone (multiple sclerosis), nuvaring (contraceptive) and rituxan (auto immune disorder) as the key products to watch out for.

- The company has highlighted that it expects more approvals in the complex generic category not yet in the public domain.

- Outlicensing deals in the ongoing drug development programmes in the specialty segment and positive news on the Sputnik-V vaccine could aid revenue growth.

- Consolidation and recovery in the domestic market coupled with incremental growth from acquired Wockhardt's products should aid performance.

Hindustan Unilever

- Market leadership across categories, wide distribution reach and synergy benefits from Glaxo Consumer brands should aid growth going ahead.

- Major beneficiary of the demand for hygiene products and has launched over 100 products in the first half of FY21 in this segment.

- The focus on volumes should help the company gain market share in key categories such as tea, soaps and detergents; it has affected limited price hikes vis-a-vis competition.

- After underperforming the Nifty by over 20 per cent in the last six months, ICICI Securities expects this (volume focus) to be a key driver for HUL stock's outperformance in CY2021.

- Calibrated price hikes across categories including premium segments to offset some of the rise in input costs across categories.

ICICI Bank

- Focus on data, analytics and technology to drive growth and improve productivity and efficiency.

- Surplus liquidity, strong capitalisation and healthy CASA ratio at 44 per cent gives it a cost advantage over peers.

- Initiatives like automated and data driven customer acquisition and decision-making have lowered turnaround times and are likely to have aided performance to reach pre-Covid levels faster than anticipated.

- Analysts expect loans to grow at a compounded annual rate (CAGR) of 11.9 per cent during FY20-23 and core return on assets (RoA) and equity (RoE) to improve from 0.8 per cent and 7.3 per cent to 1.6 per cent and 14.3 per cent during FY20-23, respectively.

- Improved profitability of group companies also adds to valuations.

Infosys

- Large deal wins have seen a sharp rise over the past two quarters; reported 16 large deal wins of $3.15 billion in Q2, the highest for the quarter.

- These deal wins provide double digit growth visibility in FY22 which coupled with growth in the digital segment will help offset the weakness in the traditional or legacy business.

- Deal wins are single biggest upside trigger for the stock in CY21 despite the 70 per cent return in CY20.

- Lower travel as well as onsite costs to help expand operating profit margins helping deliver higher earnings growth.

- Strong cash on the books gives the company options to pursue value accretive acquisitions or return cash to shareholders.

Larsen & Toubro

- Over FY19-21, the ordering levels would average Rs 1.4 times FY20 sales and order backlog would move up to Rs 3.3 times FY20 sales, with these years drawing support from large-sized orders spanning across segments such as transportation infrastructure, power, hydrocarbon and water.

- Large orders account for over 45 per cent of domestic order book and are supportive of speedier execution.

- While there could be a lull in high-speed rail corridors beyond the current Mumbai-Ahmedabad project, large airport orders may be limited to Chennai and Kolkata going ahead.

- Larsen & Toubro (L&T) is well-placed for lumpy order wins from defence sector and also business from healthcare and data centre segments.

Mahindra & Mahindra

- Tractor segment remains the mainstay of earnings growth. Volume growth to continue on the back of strong rural economy, government measures and shift to mechanisation.

- Despite the supply constraints, analysts expect high single digit growth in FY21 and stronger growth in FY22 helping it recover market share it has lost in recent months.

- New launches in the sports utility vehicle segment to help tap the stronger growth trends in this space and arrest market share loss.

- Multiple steps taken to turnaround or shut loss making international subsidiaries is helped to change the street's view on company's capital allocation priorities.

- Despite the 33 per cent uptick over the past year, analysts believe the stock is attractively valued.

Reliance Industries

- After deleveraging the balance sheet, price hikes in telecom would be the key trigger for the stock. Analysts believe price hikes could come through given slowing subscriber growth and RIL gaining substantial volume and revenue market share.

- Strong growth in the retail segment is expected to continue on new store openings, market share gains and leveraging of its online presence through JioMart.

- While the refining business is expected to see a gradual uptick, the petchem segment could surprise given supply shortages and improving demand from key user sectors.

- Positive news from upstream assets (gas) and stake sale in the oil to chemical business to Saudi Aramco remain other triggers.

SBI LIFE

- SBI Life is the largest private insurer by new business premium (NBP) and a market leader in individual private NBP with 23 per cent share as on FY20.

- The insurer is yet to fully tap into its parent SBI's customer base spread across 23,000 branches and presently has a mere 2 per cent penetration and less than 1 per cent in its digital-only YONO customer base. This implies significant runway for growth.

- The receding share of ULIPs or unit linked insurance plans (from 69 per cent on premium basis) and potential to increase individual protection business from the current 5 per cent adds to growth sustainability.

- It is seen as a front runner to capture 7x potential in individual protection segment along with rising share of annuity segment.

UltraTech Cement

- India's largest cement company, UltraTech has a strong pan-India distribution network and enjoys preferred supplier status for key infrastructure projects.

- These advantages position it ahead of peers and place it in a good spot to tap into expected growth in both retail and institutional (non-trade) cement demand.

- The cement major is ramping up its under-utilised acquired capacities such as Binani and Century, and also improving their profitability. These steps should help improve their revenue and margin contribution.

- UltraTech also has a strong pipeline of projects and brownfield expansion potential which offers visibility on long-term growth.

YTD: Year to date, P/E is price-to-earnings ratio; Data as of December 31, 2020 and compiled by BS Research Bureau; source: Bloomberg estimates, stock picks sourced from ICICI Securities, Angel Broking, HDFC Securities, Credit Suisse, Axis Securities, Nomura, Reliance Securities, BNP Paribas, IIFL Securities, Bernstein, and Motilal Oswal Financial Services; for ICICI Bank, revenue indicates net total income

Feature Presentation: Aslam Hunani/Rediff.com