'India cannot expect to be insulated from the crisis. Europe is India's biggest trading partner with two-way trade of E72.5 billion or Rs 530,000 crore last year,' says Paranjoy Guha Thakurta.

Even black humour has its ideological orientation as far as today's Greece is concerned.

The capitalist version of the joke goes like this. Going Dutch means everyone sitting at a restaurant table shares the bill while Going Greek means that after everyone has eaten and drunk, everyone gets up and realises that no one has money to pay the bill.

In the socialist version of the joke, those who have ordered food realise that those sitting at the next table -- who are owners of the restaurant -- are eating their food, but they are nevertheless being presented the bill.

A capitalist joke: While the gross domestic product (GDP) of Greece is currently around $250 billion, the surplus cash in the balance sheets of the Apple group of companies is $30 billion higher. So Apple should buy Greece so that its employees, who are computer geeks, have a permanent holiday destination serviced by Greeks.

A joke loved by socialists is a statement made by an American capitalist around a century ago: If you owe a bank $100 and can't repay it, you have a problem; if you owe a bank $100 million and cannot repay your dues, your bank has a problem.

In German playwright Bertolt Brecht's The Resistible Rise and Fall of Arturo Ui, which parallels the rise of Adolf Hitler and Chicago gangster Al Capone, at the end of the play, the lead actor who plays Arturo Ui comes forward on the stage, takes off his Hitler moustache, and speaks the epilogue to the audience:

If we could learn to look instead of gawking

We'd see the horror in the heart of farce

If only we could act instead of talking

We wouldn't always end up on our arse...

Greece is in turmoil. Almost all the 28 nation-States of Europe are in the throes of a double-dip or triple-dip recession. The decision to make the Euro a common currency was taken 16 years ago in 1999. At present, 19 countries are part of the Eurozone. It will soon (that is, by Sunday July 5 or Monday July 6) be known whether Greece will remain in the Eurozone.

On Tuesday, June 30, Greece became the first 'developed' country in recent times to default on its loan repayment obligation to the International Monetary Fund. The IMF is the third arm of the 'troika' comprising the European Central Bank and the European Commission that have loaned huge amounts of money to Greece.

In 2004, the public debt of Greece was Euro 183.2 billion; this amount went up to nearly E300 billion by 2009 or 127 per cent of the country's GDP and further to over E323 billion at present or a staggering 175 per cent of the GDP or national income of Greece.

The distance between Athens and Berlin has stretched and become longer since the Second World War began in 1939 and ended in 1945. Among sections of Greeks, German Chancellor Angela Merkel has been demonised as a new avatar of Hitler.

It is frequently recalled in Greece that after the 1953 London Agreement, half of post-Nazi Germany's public debt was written off, thereby paving the way for Germany to become an industrial powerhouse and the richest country in the Eurozone.

As The New York Times remarked on July 2: 'With memories of World War II, the glue that initially held the (European) project together, now faded, the union is bound together by fiendishly complicated rules, informal codes of behaviour and a passion among its bureaucrats (also derogatorily called 'Eurocrats') for technical minutiae that baffles ordinary citizens. Syriza, however, has thrown a hand grenade into the whole setup.'

In January, Syrizia, an acronym meaning 'radical coalition of the Left,' won the elections in Greece. After the coalition's success in the polls, the 40-year-old leader of Syrizia and Prime Minister Alexis Tsipras exulted: 'The Greeks wrote history.'

Most observers perceived the electoral outcome in Greece as a revolt by the youth against the rich elite. Greek oligarchs, especially shipping magnates, have occupied space in the popular imagination. Remember Aristotle Onassis, reportedly once the 'richest man in the world,' who married Jacqueline Kennedy and courted opera singer Maria Callas?

After the troika sought to 'bail out' the government of Greece in a way in which it was supposed to revive the economy, exactly the opposite happened. In less than five years, Greece's economy was ravaged with national income shrinking by roughly a fourth and real wages coming down by a similar proportion.

After the troika sought to 'bail out' the government of Greece in a way in which it was supposed to revive the economy, exactly the opposite happened. In less than five years, Greece's economy was ravaged with national income shrinking by roughly a fourth and real wages coming down by a similar proportion.

One out of four people in that country is currently living in poverty, unemployment and social exclusion by European standards. Over 26 per cent of the 11 million population of Greece is unemployed and over 60 per cent of the country's youth is without jobs.

As the new government in Athens, which was elected to power on a programme to resist the imposition of so-called austerity measures -- a euphemism for cutting public spending on health-care, pensions and education -- sought to renegotiate the country's debt burden, it predictably ran into huge opposition from the troika in general and Germany's Merkel in particular.

Tsipras' government could hardly escape the burden imposed by the profligacy of predecessor governments that had not just splurged on borrowed money, but also fudged accounts, as has been observed by an official committee instituted to find the 'truth' about Greece's public debt.

Roughly 80 per cent of the country's debt is owed to various institutions in Europe and the IMF and the rest to private creditors.

The increase in Greece's debt before 2010 was not so much on account of excessive government spending but more on the high rates of interest at which it borrowed funds, loss of tax revenue due to illicit outflows and also because of high military spending.

Of the E254 billion loaned to Greece over the last decade, barely 11 per cent of the amount was spent on the government's current expenditure.

Yet the troika still wants Greece to show a budget surplus of 3.5 per cent of GDP (excluding interest) by 2018. This clearly seems an impossible task given the current state of the country's economy.

After defaulting on paying its dues of E1.5 billion to the IMF on the last day of June, the Greek prime minister suggested a new loan of E29.1 billion to cover its debt repayments over the next two years. But that did not take place.

The crisis in Greece is not just about the size of its huge debt overhang. As Nobel Laureate Joseph Stiglitz observed, very little of the amount of money lent to Greece has gone to the country's people; it has gone largely to private creditors, notably banks and financial institutions in Germany and France.

Another Nobel Laureate in economics, Amartya Sen, compared the prescription being given to Greece by the troika to a pill containing both antibiotics and rat poison. The patient is ill and desperately needs the medicine, but can only have the tablet that contains both antibiotics and deadly poison.

Greece accounts for barely two per cent of the combined GDP of Europe. Why then is it so important? Answer: there is genuine fear that if 'Grexit' happens, the 'contagion' will spread across Europe and perhaps, much of the rest of the world.

The first countries that are likely to be adversely affected by a Grexit will be the relatively weak economies of Europe such as Portugal, Spain, Ireland and Italy. Political formations on the Right and the Left are gearing up for bitter battles in Spain, France and the Netherlands.

Analysts like Mathew Lynn of Market Watch (which is owned by Dow Jones) argue that by exiting the Eurozone, the 'real damage' will not so much be on Greece, but more on the European Union and the IMF.

Many in Greece and across the world agree with Tsipras when he claims that the troika is trying to 'blackmail' the country in a desperate battle between global finance capital and the forces of democracy.

There is likely to be greater economic, social and political uncertainty across Europe and the world in the near future. Over the last five years, there have been a dozen-odd regime changes in the 28 countries of the European Union.

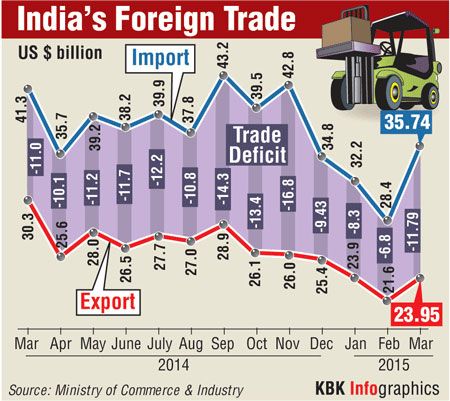

India cannot expect to be insulated from the crisis despite claims to the contrary made by government spokespersons. Exports are down from this country. It must be remembered in this context that as a single entity, Europe is India's biggest trading partner with two-way trade of E72.5 billion or Rs 530,000 crore last year.

India cannot expect to be insulated from the crisis despite claims to the contrary made by government spokespersons. Exports are down from this country. It must be remembered in this context that as a single entity, Europe is India's biggest trading partner with two-way trade of E72.5 billion or Rs 530,000 crore last year.

With the future of the Euro uncertain, the question that is being raised over and over again is whether it is at all possible, leave alone desirable, to attempt to bring about economic unity without political integration. The European Union was formed to create a single market, even if only 19 out of the 28 member states are at present part of the Eurozone.

India's experience has been different. This country may be more politically united than before, but its economy remains disintegrated. This is why the government is finding it so difficult to implement what many believe would be the most important economic reform measure that could reduce corruption and create a unified market for the Indian Union, that is, a common Goods and Services Tax (GST) for all of this country's 29 states and seven Union territories.

There is yet another important lesson that India needs to learn from the recent European experience. We in this country need to get our banking system in order, sooner rather than later.

The non-performing assets (NPAs) -- or a euphemism for loans not repaid -- of public sector banks has been steadily rising and continues to rise, comprising over ten per cent of the total 'stressed' assets of the banks.

Most of these bad loans have been disbursed not to small players, but to large corporate entities owned and controlled by big businessmen, including the likes of Vijay Mallya's Kingfisher Airlines.

Having withstood some of the worst ravages of the Great Recession that started in 2007-2008, Indian banks are financially weaker than before, even as the government and Arun Jaitley remain niggardly in re-capitalising the assets of the country's nationalised banks.

As the debate on the desirability of amending India's land acquisition law intensifies here at home, the ideological divide between the Left and the Right across the world has become sharper than before, especially since the collapse of the Berlin Wall in 1989 and the subsequent disintegration of the former Soviet Union.

As Stiglitz argued, the crisis in Greece is 'about power and democracy much more than money and economics.'

Irrespective of the outcome of the referendum in Greece on Sunday (July 5), the political economy of the planet may have changed more significantly than what many of us imagine.

Images: Top: People wait to withdraw cash from an ATM on the island of Crete, Greece. Photograph: Stefanos Rapanis/Reuters

Middle: An anti-austerity pro-government demonstration outside the Greek parliament in Athens. Photograph: Yannis Behrakis/Reuters

Bottom: India's Foreign Trade. Graphics: KBK