Photographs: Reuters Jaimini Bhagwati

Despite what partisan fund managers are projecting, the rise in the Indian equity market has to be evaluated carefully, says Jaimini Bhagwati.

In the last 12 months, the 30-stock Sensex and the Sensex-100 have gone up by 16 per cent and 14.6 per cent respectively.

About 10.3 per cent and 12 per cent of the rise in these two indices respectively took place in the last three and a half months.

Foreign institutional investors (FIIs) have been the principal investors, and their net investments in Indian equities from January 1 to April 16 amounted to $4.8 billion. In comparison, over these three and a half months, net FII investments in Indian government debt totalled $5.1 billion.

This article reviews the domestic and international perceptions that have motivated these investments and the extent to which optimistic sentiments are likely to be sustained.

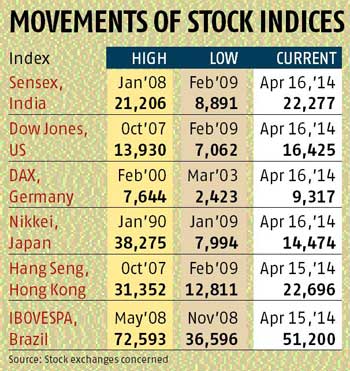

The table provides a listing of the highs and lows of stock indices in a sample group of developed and emerging economies in the past few decades.

The table provides a listing of the highs and lows of stock indices in a sample group of developed and emerging economies in the past few decades.

For the Indian, American, Japanese, Hong Kong and Brazilian equity markets, lows were reached in the first quarter of 2009 or the fourth quarter of 2008, after the last financial sector breakdown.

...

Market boom: Are stock prices inflated?

Photographs: Reuters

For Germany, the lowest point was reached in March 2003 after the information technology bubble burst in 2002. Although the Indian, US and German stock indices are hovering around their highest levels ever, the Japanese, Hong Kong and Brazilian equities have not yet climbed back to their historic highs.

Clearly, such cross-country comparisons of stock market performance over long periods of time can be misleading since constituent companies in stock indices change over time.

Further, index levels are impacted by the extent to which the firms included in equity indices declare dividends, issue bonus shares, acquire or merge with other firms and so on.

Additionally, the countries for which stock indices are listed are at different stages of economic development, productivity, transparency and regulatory efficiency.

In India, the following are a few pointers to future movements of our stock markets. For instance, the Sensex has given up some of its recent gains on April 15 and 16 since investors appear to be concerned about the higher-than-expected inflation numbers that were released on April 15.

More broadly, Indian growth has been below five per cent for two years and growth in industrial production is flat. However, the merchandise trade balance improved during April-December 2013.

Exports were up 5.5 per cent and imports down 6.5 per cent compared to the same period in 2012, due to rupee depreciation. Incremental domestic investments in stocks have been mostly from government-owned insurance companies and the odd mutual fund.

...

Market boom: Are stock prices inflated?

Photographs: Uttam Ghosh/Rediff.com

Turning to the global environment, with China's gross domestic product (GDP) growth estimated at 7.4 per cent for the first quarter of 2014, it is facing a slowdown compared to its high growth standards.

And murmurings about how much China's shadow banking sector ironically casts a shadow on the ability of the formal financial sector to provide credit are growing. In the US, growth has picked up, but projections for inflation are still subdued and may not reach the target of two per cent for another year or more (according to the minutes of the March 18-19, 2014, meeting of the US Federal Reserve's Open Market Committee).

The Reserve Bank of India (RBI) continues to be concerned about potentially destabilising foreign exchange outflows from India as the US Fed's "tapering" continues and possibly gains momentum.

This was evident from the RBI governor's intervention at a Brookings event in Washington, DC, on April 10, 2014, seeking multilateral co-ordination to avoid competitive monetary easing. It was proposed that safety net arrangements through the International Monetary Fund (IMF) could help avoid excessive reserve accumulation.

The reaction from former Federal Reserve Chairman Ben Bernanke was that sufficient co-ordination was already taking place across central banks. Since IMF quota reforms continue to be opposed, it is highly unlikely that the IMF will be allowed to act independently if there is a perceived conflict across IMF shareholders.

...

Market boom: Are stock prices inflated?

Photographs: Uttam Ghosh/Rediff.com

Incidentally, last month, the US administration's linkage of IMF quota reforms to aid to Ukraine was rejected by the US Congress. As Fed tapering inevitably leads to higher dollar interest rates, we cannot expect effective remedies to capital flight from either the IMF or the G20 grouping. Consequently, India should raise its foreign exchange reserves at every available opportunity.

On April 14, 2014, after the spring meetings of the IMF, European Central Bank President Mario Draghi signalled that the ECB may venture into the uncharted territory of negative nominal interest rates instead of quantitative easing to combat low inflation in the euro zone.

In Japan, the rise in Japanese equity markets has mirrored the depreciation of the country's currency from 77 to 101 yen to a dollar. Japan's central bank is likely to continue with its easy money policy even at the risk of continuing to annoy the US.

It is in this environment, taking domestic and international drivers into account, that it is surprising that the Indian equity indices are around their highest levels ever.

It is likely that the recent stock market boom is due to investor perception that project implementation, which has been paralysed for some time, would speed up and that the next government would be market friendly and fiscally more responsible.

...

Market boom: Are stock prices inflated?

Photographs: Uttam Ghosh/Rediff.com

Consequently, despite what partisan fund managers are projecting, the rise in the Indian equity market has to be evaluated carefully.

To sum up, retail investors would do well to invest in individual stocks that they have tracked for years and for which they have estimated a dollar-denominated return over differing time horizons, including dividends. It is only with such a cautious approach that individual investors can avoid getting burnt.

They need to think beyond the forthcoming general election results of May 16 in order to protect against the possibility that we do not get a government that lasts five years.

Namely, it should not be just election results-based gambling for investors, since some of the upside of a stable government is factored into the recent rise in stock prices.

The writer is a former Indian high commissioner to the United Kingdom and served as a finance professional in the World Bank and the finance ministry. He is currently RBI professor at Icrier.

article