Experts say that despite the sizeable client base, PMS providers lag their domestic MF counterparts by quite a distance, when it comes to reporting and disclosure standards.

Jash Kriplani reports.

Illustration: Dominic Xavier/Rediff.com

The Portfolio management service (PMS) sector has grown at a sharp pace in India, with the growing pool of high networth investors (HNIs) going for this investment option in search of higher returns.

However, experts say that despite the sizeable client base, PMS providers lag their domestic MF counterparts by quite a distance, when it comes to reporting and disclosure standards.

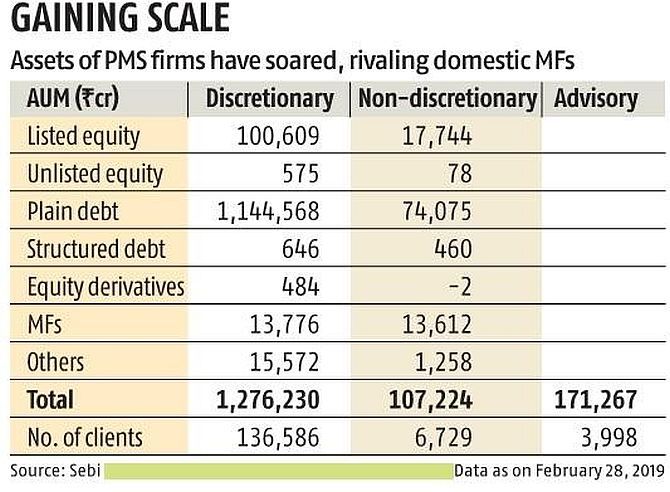

Over the last four years, the size of assets managed by PMS providers has grown at an annual rate of 16 per cent.

At the end of February, assets under management of portfolio managers stood at Rs 15.6 trillion with a client base of over 147,300.

As the industry gains in size, experts say disclosures made by portfolio managers, particularly with respect to performance, should improve.

"Lot of PMS firms report the returns of a model portfolio, which doesn't give a fair picture of the performance of actual portfolios within a strategy.

These are also typically net returns (after fees), which doesn't show the impact of the fees being levied on the investor," said Sanjay Parikh, who is leading the initiative to implement the Global Investment Performance Standards -- formulated by the CFA Institute -- in India.

"Moreover, there is also no clarity on whether returns for a financial year take into account all investor returns for that period, or excludes returns for exiting investors," he added.

According to experts, computing returns on the basis of only existing investors could give a lopsided view of a strategy's performance.

"Typically, an investor exits a PMS-managed portfolio when he is disappointed with the returns.

"So, while reporting returns for a financial year, the provider should adjust for exiting investors' returns too," said Jinal Sheth, portfolio manager at Multi-Act Equity PMS.

Further, such practices can lead to mis-selling.

"There are instances of advisors pointing investors to the regulator's website, where returns shown are combined for all portfolios, across strategies. These don't give a fair picture of the performance and aren't comparable with other PMS' returns reported," Sheth added.

The Securities and Exchange Board of India's (Sebi) site states the performance of portfolio managers has not been approved or recommended, and also that it doesn't certify the accuracy or adequacy of their monthly reports.

However, industry insiders say the fine print is not emphasised upon while selling PMS products.

Currently, regulations laid down by Sebi only mandate PMS providers to follow the weighted average method to calculate returns in individual categories.

"While the regulator has regulated the MF industry heavily as it is more retail-focused, it has not set tight norms for the PMS sector, given its orientation towards more sophisticated and wealthy clients," said a PMS provider, requesting anonymity.

Following the 2008 market crash, Sebi decided to curb some of the practices in the PMS industry.

The minimum investment size was increased from Rs 5 lakh to Rs 25 lakh, fund managers were restricted from pooling investments from clients, and the norms around profit-sharing or performance-related fees were made tighter.

While industry sources say these changes have helped in giving more credibility, there is more scope for improvement in the reporting standards.