Though the deduction will be higher and net take-home pay will fall, you can get a significant tax benefit.

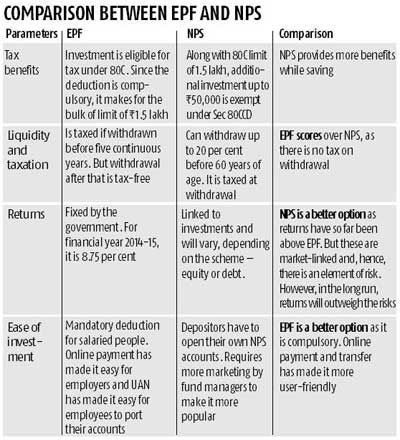

With introduction of the National Pension System and retirement funds from mutual funds, the Employees' Provident Fund Organisation (EPFO) might be losing its sheen.

With introduction of the National Pension System and retirement funds from mutual funds, the Employees' Provident Fund Organisation (EPFO) might be losing its sheen.

In fact, in his Budget speech, Finance Minister Arun Jaitley had referred to EPFO subscribers as "hostages, rather than clients".

"The low-paid worker suffers deductions greater than better-paid workers, in percentage terms," he had said.

As of November 2014, the EPFO had 41.9 million contributing members; the interest rate for 2014-15 has been fixed at 8.75 per cent.

With the EPFO launching an electronic challan-cum-return facility, companies can make EPF payments electronically.

Last year, the Universal Account Number (UAN) facility was launched for facilitating portability of accounts. Other changes, too, have been proposed.

Let's see how these will impact subscribers:

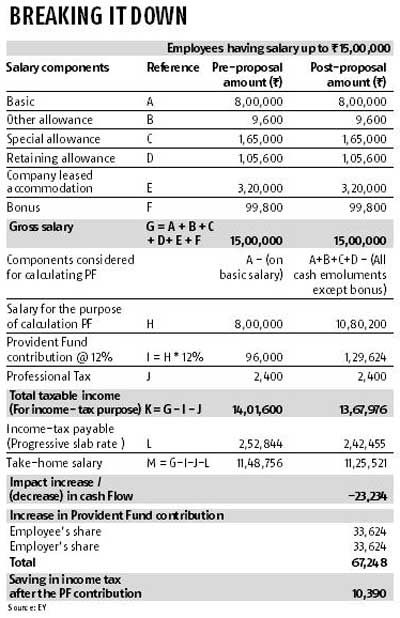

Change in the way EPF contribution is calculated

Currently, contribution to EPF is calculated as a percentage of the basic salary and dearness allowance. It has been proposed other allowances be also included.

These include special and specific allowances such as house rent allowance, conveyance, medicines, food, education and furnishing.

This means while the contribution of employees and employers to the EPF will increase, the net salary (take-home salary) will be reduced.

"Here, the positive is it will help accumulate a much bigger corpus at the time of retirement, which is a good thing. The flip side is the money in hand could go down, affecting the servicing of current expenses and loans," says Suresh Sadagopan, founder of Ladder7 Financial Advisories.

Small firms, for which allowances form a small part of the salary package, might not feel the pinch. But for large corporations, deductions and employers' contributions will rise.

"Now, employers will also guard their positions, as they have to contribute an identical amount to PF funds. So, in all likelihood, the structure will be further aligned to reduce cash in the hand of employees," says Malhar Majumder, partner and consultant, Positive Vibes Consulting and Advisory. "Even if this creates a challenge initially in terms of the take-home pay, ultimately, it makes sense for retirement benefits," says Sudip Mukhopadhyay, managing partner, Vantage Health and Benefits Consulting.

Raising contribution to pension from 58 to 60 years

This was long overdue, considering the retirement age was increased from 58 to 60.

"For the two-year period between 58 and 60, contribution to the pension component of the EPF stopped but contribution to the provident fund continued. For these two years, subscribers were getting a salary as well as pension, simultaneously. Now, this anomaly will be corrected," says Majumder.

Withholding 10 per cent of the fund till subscriber turns 50

This proposal is aimed at discouraging subscribers from withdrawing the PF amount before superannuation.

Today, most employees withdraw their PF while changing jobs, to avoid transferring the money to the account of the new employer.

Account portability, as proposed by the UAN, should help resolve this. To ensure employees do not withdraw the entire corpus, one could be allowed to withdraw the employee's contribution alone, not the employer's.

Sadagopan says though this proposal is positive, 10 per cent is too small an amount; he adds it should have been much higher, say, two-thirds. "With UAN for EPF holders, porting from one company to another is not a hassle. So, holding 10 per cent will not be a challenge," he says.

However, for subscribers who need the entire money, this could pose problems. "It is important to spread awareness about the need for retirement savings among subscribers. A proper blend of education and fiscal incentives might stop the practice of premature withdrawal," says Majumder.

Making employees' contribution optional below a certain income

The Budget proposed for employees below a particular monthly income threshold, contribution to the EPF should be optional, without affecting or reducing the employer's contribution.

The threshold, however, wasn't mentioned. In case the salary is low, if the PF contribution is not deducted from the employee's salary, it will increase the take-home salary. But without the employee's contribution, the PF corpus will be small.

This could result in hardships later, says Sadagopan.

Change in pension calculation; minimum pension of Rs 1,000/month

Currently, pension is based on the average of the salaries drawn in the past 60 months.

It has been proposed this be changed to the past 30 months. If that is the case, the pension amount will increase for most subscribers.

But a minimum pension of Rs 1,000 a month does not help retirees, given the current high prices, says Majumder.

Amarpal Chadha, tax partner, EY India, says, "There have been many improvements over the recent past in the way EPFO operates, the kind of facilities provided to contributors/employers like online facility, SMS alerts for monthly credit into the account, etc. Earlier, it was time-consuming to get a PF account transferred/withdrawal from the account. However, there has been significant improvement in the processing time over the recent past. Having said that, better coordination with employers and putting right control measures in place at the PF organisation might help in streamlining processes like PF transfer/withdrawal much better."

THE RATIONALE BEHIND THE PROPOSALS

A senior EPFO official explains

Basic plus allowance: The labour ministry is yet to decide on a proposal to calculate provident fund based on basic pay and allowances. There is some opposition from employers, as this will mean more contribution from their side

Increasing pension contribution: The proposal to increase pension contribution from 58 to 60 years is only an enabling one; the contribution is voluntary, as some employees retire at the age of 60. Earlier, there was no provision to contribute towards pension after one is aged 58. The move will help subscribers, as they could earn interest on the additional contribution

Withholding 10% of the corpus: The proposal to withhold 10 per cent of the corpus till a subscriber is 50 is aimed at stabilising the UAN. The EPF should serve as a true social security, not like a savings bank account. In fact, in most developed countries, 30-40 per cent of an employer’s contribution is not given to the subscriber before retirement.