It will bring down the cost of a second house because of tax benefits and price appreciation

Advice for ones sitting on the fence perpetually: It makes sense to buy your first property even if it isn't in the perfect location or of the right size.

Advice for ones sitting on the fence perpetually: It makes sense to buy your first property even if it isn't in the perfect location or of the right size.

Banker couple Ashesh Bharti (31) and his wife Priyanka (29) have been going through the same dilemma for some time. While Priyanka wants to buy the house right away, Ashesh feels it's better to save and buy one that would meet all their needs.

"If we stretch ourselves, we can afford a house that costs Rs 1.4 crore now. The best we can get, in this budget is a two-bedroom property in the distant suburbs of Mumbai.

The way our careers have progressed, in the next 7-10 years we should be able to buy a three-bedroom flat in a better location," says Ashesh. Priyanka, on the other hand, believes they should purchase one now and upgrade to a bigger property by selling this one at a later date.

Experts believe in most cases buying a house one can afford at present can work out to be a better option. Later, the buyer can sell it to buy a bigger house or one at a preferred locality.

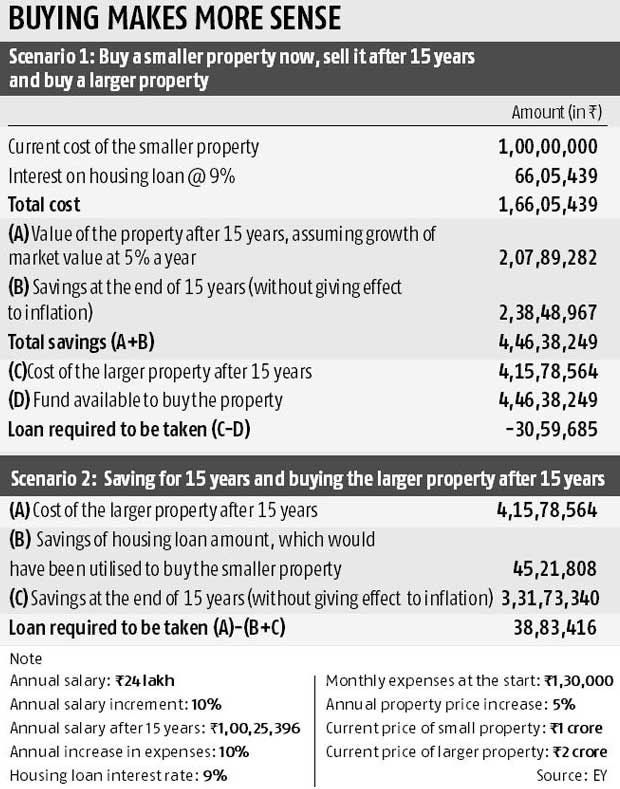

If you look at the table compiled by EY, when there is a dilemma such as this, there is a choice. A person with a budget of Rs 1 crore but wanting to purchase a property worth Rs 2 crore can save aggressively for the bigger property or can buy the smaller one now and continue saving for the bigger one.

The advantage: The first property, while he is saving for the second, will provide him capital appreciation and give tax benefits.

Problems of buying late: For one, steady growth in career and salaries has to be taken into consideration. And, over longer periods like 7-10 years, there are bound to be ups and downs, much like what happened to employees after the 2008 stock market crash or in situations like Brexit.

If the annual salary of a person is Rs 12 lakh and grows at 10 per cent annually, he would be earning around Rs 31 lakh after a decade. This also means the person's loan eligibility will grow. At an income of Rs 12 lakh a year, he will be eligible for a Rs 55.5 lakh loan for 20 years at an interest rate of 10.4 per cent.

A decade later, at an income of Rs 31 lakh, he can get Rs 1.43 crore loan. If the partner is also working, it would boost the eligibility. "Usually, people tend to ignore their growth potential and rush to buy a house. Between the age of 25 and 40, an individual's career progresses rapidly," says Amit Oberoi, national director, knowledge systems, Colliers India.

Real estate experts also say a majority of the buyers don't buy a second property, or are unable to, as other financial priorities take over later in life like children's education, marriage, retirement planning, etc.

On the flip side, postponing your decision could also mean you might end up paying rent, which could have been used to pay the equated monthly instalment (EMI) on the loan. "While taking the decision between buying now and later, one must not only calculate the rent but add the maintenance, taxes and brokerage they have to pay," says Oberoi.

Another thing that could happen is that property prices rise faster than your salary growth. In such a case, the house you aspire for might never fit into your budget.

Buy now: "Purchasing a property in youth means you have created an asset that will appreciate with time," says Shveta Jain, managing director, residential services, Cushman & Wakefield.

So, while you will grow in your career, the value of the property you have purchased will also grow. If an individual decides to change the house, he can sell the existing one and that will fetch him significant value.

The income tax benefits are also conducive for such transactions. If a person sells a house after holding it for three years, he doesn't need to pay any capital gains tax if the money is reinvested in a property. The tax benefit, coupled with savings in rent and appreciation in the property value, makes it more attractive to buy a house in the budget and then upgrade to a better one.

In addition, buyers also get income tax deductions on house purchase. Under Section 80C, an individual can gets Rs 150,000 deduction on the principal amount of the housing loan. For a couple, this will be Rs 300,000. Then, there's deduction of Rs 200,000 on the interest paid every year under, Section 24, if the house is self-occupied. For a couple, this means a deduction of Rs 400,000. If it's given on rent, the entire interest income can be claimed for deduction.