'I cannot believe I was removed on grounds of non-performance,' an angry Cyrus Mistry wrote in his mail following his sudden ouster as Tata Sons chairman.

But what do the facts say?

Aslam Hunani looks at how key Tata group companies fared under Mistry's stewardship.

On October 24, 2016, in a corporate surgical strike, the board of directors of Tata Sons, the controlling entity of all the Tata group companies, sacked Cyrus Pallonji Mistry as group chairman after just four years in the job, and announced the return of Ratan Tata as interim chairman for four months, in which time a new chairman will be selected.

The ostensible ground for Mistry's abrupt dismissal, which sent shockwaves through India Inc and rattled the stock markets enough to push down the share prices of group companies, was 'non-performance.

Which Mistry has strongly rebutted in an internal email circulated to Tata group employees.

Cyrus Mistry had taken over as chairman of Tata Sons on December 28, 2012, from Ratan Tata who retired after serving as group chairman for more than 21 years.

Mistry was only the second non-Tata to become group chairman.

His family's Shapoorji Pallonji group is the largest individual shareholder in Tata Sons, with 18.4% stock-holding (the largest collective shareholder are the Tata Trusts, with more than 66% holding, which enables it to push through any proposal).

In his damning email, Mistry wrote: 'I had to take many tough decisions with sensitive care to the group's reputation as well as containing panic amidst internal and external stake-holders.'

'Despite bad press, impairments were taken to clean the books but substantial exposure remains. Dividends were reduced to conserve cash for needed investments in the teeth of shareholder fury. Apart from hotels, the group made several exits in the fertiliser business, UK steel operations...'

'I had to ease out hangers-on who are prone to flaunt their proximity to power...'

Against the backdrop of the battle that has clearly broken out in the Tata board -- on which Mistry remains a director -- it is worthwhile to examine the performance of the Tata flagship companies in the last three years, with Mistry at the helm.

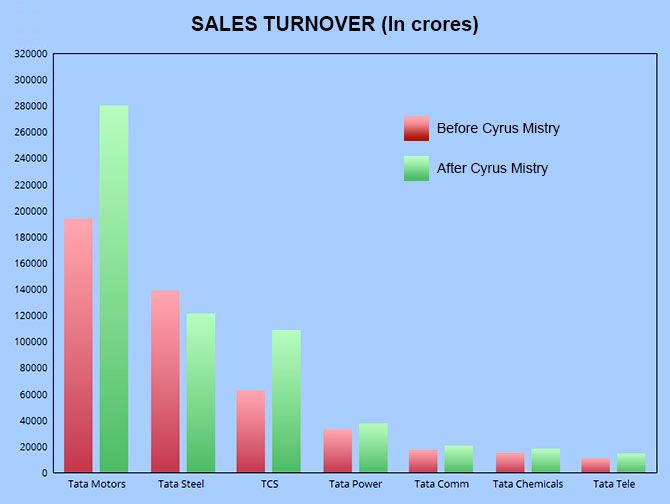

Since there are more than a hundred companies under the Tata banner, we have picked the top seven group companies based on their sales turnover in the 2013-2016 period when Mistry was in charge.

The parameters analysed are sales turnover, net profit, total debt, total assets and stock prices of these companies.

Automobile major Tata Motors reported sales of Rs 280,097 crore in the financial year 2016, a surge of 44.6 per cent from the sales figures of Rs 193,698 crore in FY 2013.

Similarly, the software arm, Tata Consultancy Services, reported an increase of 72.5 per cent in its sales turnover during the period FY13 to FY16.

The main laggard in the sales was Tata Steel, which reported negative sales -- a decline of 12.4 per cent from FY13 to FY16.

In his communication to Tata group, Mistry pointed out: 'The European steel business faced potential impairments in excess of USD 10 billion, only some of which has been taken as of date.'

Under Mistry, the group had announced in March that it was reviewing its European steel operations, and has since been in negotiations with Germany firm Thyssenkrup over merging their European steel operations.

The group has also been in talks with the UK government about financial aid for Tata Steel UK.

Under Mistry, some of these group companies have reported decent profits.

The embattled Tata Motors has reported a rise of 22.3 per cent in net profit from FY13 to FY16.

On TaMo, Mistry writes: 'Historically, the company employed aggressive accounting to capitalise substantial portion of the product development expenses, creating a future liability.'

'Beyond this, the Nano product development concept called for a car below Rs 1 lakh, but the costs were always above this.'

'This product has consistently lost money, peaking at Rs 1000 crores. As there is no line of sight to profitability for the Nano, any turnaround strategy for the company requires it to shut it down.'

'Emotional reasons alone have kept us away from this crucial decision.'

'Another challenge in shutting down the Nano is that it would stop the supply of the Nano gliders to an entity that makes electric cars and in which Mr Tata has a stake.'

In the 2013-2016 period, TCS, the group's cash cow by a mile, recorded a jump of 72.3 per cent in its net profit, from Rs 13,836 crore to Rs 23,928 crore.

Of the companies not listed here, Tata Elxsi leads group companies in terms of rise in net profit with a 388.9 per cent, from Rs 32 crore to Rs 154 crore, closely followed by Tata Capital Housing which recorded a surge of 303.9 per cent in its net profit, from Rs 28 crore to Rs 113 crore in the same period.

This is the core area of concern for any corporation, and the Tata group companies were not lagging behind in this area in comparison to their peers.

Tata Motors saw a rise of 31.2 per cent in its debt to Rs 70,468 crore from Rs 53,716 crore.

Similarly, Tata Steel which reported negative sales numbers, also saw its debt increase by 25.8 per cent to Rs 86,204 crore from Rs 68,507 crore.

Tata Teleservices Ltd also saw a great increase in its debt to Rs 35,204 crore from Rs 23,491 crore.

On Tata Tele, Mistry writes: 'Of all the companies in the portfolio, the telecom business has been continuously haemorrhaging.'

'If we were to exit this business via fire sale or shut down, the cost would be USD 4-5 billion. This is in addition to any payout to DoCoMo of at least a billion plus dollars.'

'The original structure of the DoCoMo transaction raises several questions about its appropriateness from a commercial or prudential perspective within the then prevailing Indian legal framework.'

'In light of all this, our strategy over the past three years has been to increase the EBITDA from Rs 400 crores to Rs 2500 crores, in the hope of being a potential player in the consolidation of the industry.'

Of the other companies, TCS, Tata Power Co, Tata Communications and Tata Chemicals saw a marginal rise in debt.

Even though the liabilities of some group companies rose during Mistry's tenure, a few others reported a positive trend in their assets as well.

Tata Motors reported a rise of 68.3 per cent in its assets, from Rs 10,3345 crore to Rs 17,3903 crore.

Similarly, TCS reported a rise of 66 per cent in assets.

Tata Steel's asset quality increased by 12.8 per cent in the interim period.

Some other group companies like Tata Power and Tata Tele reported a marginal increase in their assets.

On Tata Power, Mistry writes: 'Tata Power aggressively bid for the Mundhra project based on low-priced Indonesian coal. As regulations changed, the losses in 2013-14 alone amounted to Rs 1,500 crores.'

'Given that Mundhra constitutes Rs 18,000 crore of capital employed (40% of the overall company's capital employed), this substantially depresses the return on capital for Tata Power as well as carries the risk of considerable future impairment.'

Return on Investment as reflected in the stock prices is the main gauge to find out if and how the companies have benefited the investors with Cyrus Mistry as chairman.

As the end of trading on October 26, 2016, Tata Motors saw its share price rise to Rs 526.9 from Rs 310.05.

Similarly, TCS' share value rose to Rs 2,383 from Rs 1,267.5.

However, the beleaguered Tata Steel and Tata Power were not able to provide profits to the investors, with their share value actually seeing an erosion.

Tata Communications and Tata Chemicals also gave good returns to shareholders when Mistry was leading the group.

How does Mistry look back on his tenure?

He writes: 'During my term, the operating cash flows of the group have grown at 31% compounded per annum.'

'The Tata group valuation from 2013 to 2016 increased by 14.9% per annum in rupee terms as against the BSE Sensex annual increase of 10.4% over the same period.'

'The Tata Sons net worth has increased from approximately Rs 26,000 crores to Rs 42,000 crores, after considering the impairments.'

'This has significantly strengthened our balance sheet, enhancing our ability to absorb further shocks from restructuring in the companies.'

'I cannot believe that I was removed on grounds of non-performance.'

Data source: Capitalineplus

Design: Reuben N V