With the stock coming under pressure, the MF holding value could have dropped to Rs 50 billion, back-of-the-envelope calculations show.

Jash Kriplani reports.

The drop in share prices of YES Bank has weighed on the net asset values (NAVs) of several mutual fund schemes.

Shares of YES Bank, which is part of the Sensex and Nifty, are down 57 per cent from their all-time highs of Rs 394 on August 20.

The drop comes amid uncertainty over leadership succession at the bank, concerns over governance practices, and a ratings downgrade, which could raise borrowing costs and hit margins.

An analysis of the market data indicates the value of MFs' equity holdings in YES Bank is down 30 per cent since the September quarter.

At the end of the quarter, the value of the MF holdings stood at Rs 84 billion.

With the stock coming under pressure, the MF holding value could have dropped to Rs 50 billion, back-of-the-envelope calculations show.

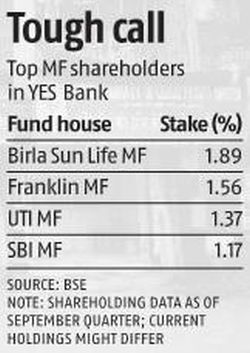

As of September 30, Birla Sun Life MF, Franklin MF and UTI MF were among the fund houses with highest equity stakes in the troubled lender.

The impact of the share price slide for each of the fund houses would depend upon their average buying and selling price.

Last week, credit rating agencies ICRA and CARE Ratings downgraded YES Bank's debt instruments.

The move triggered a fall in the lender's shares and bonds.

Analysts say the ratings downgrade would affect the bank's profitability because the cost of borrowings goes up.

Also, if the bank decided to raise equity capital, the weaker share price could mean higher dilution for existing shareholders.

Experts say YES Bank has high dependence on wholesale funding compared to some of its large peers.

In a note, Investec says YES Bank is less capitalised and has higher dependence on wholesale funding, which makes it 'vulnerable to liquidity issues'.

'We believe liquidity is the more critical (issue) of the two and all the rating agencies (including Moody's) have reiterated that the liquidity situation at the bank is comfortable,' says Investec.

Credit rating agencies were more sanguine over the private lender's liquidity profile.

'The bank's daily average liquidity coverage ratio (LCR) 99.44 per cent for Q2FY19 and 101 per cent for Q1FY19 -- compared to the RBI's requirement of 90 per cent as on January 1, 2018 and 100 per cent as on January 1, 2019 -- remains comfortable.' ICRA said in its report.

'The deposits for the bank have remained stable, which provides further comfort,' ICRA said, while downgrading the bank's tier-II bonds from 'double A plus' to 'double A'.

Analysts say asset quality and potential divergence are major factors that could weigh on the stock.

'From a fundamental perspective, after liquidity, the biggest variable would be that of divergence,' the Investec note says.

'Based on the credit cost guidance of 50 to 70 basis points for FY19E, we estimate the divergence could be in the range of 50 per cent of last year's divergence of Rs 64 billion,' adds the Investec note.