A flavour-of-the-season approach does not work in investing, suggests Deepesh Raghaw.

Illustration: Uttam Ghosh/Rediff.com

When it comes to investing, skill is extremely important.

However, experience is perhaps the greatest teacher.

Experience makes us aware of the various risks that exist.

This awareness changes one's approach so that from merely focusing on higher returns, we also begin to focus on risk mitigation.

Let us take a look at some of the key lessons that 2019 taught us.

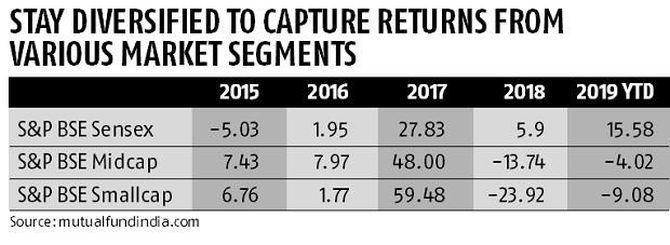

No strategy works all the time

In the 2014-2017 period, mid and small-cap funds outperformed the Nifty, Sensex and large-cap funds by a wide margin.

It was not uncommon for an investment advisor like me to come across portfolios with over 60% exposure to mid and small-cap funds.

Many investors who had never invested in anything riskier than bank fixed deposits wanted to put a large portion of their wealth in mid and small-caps funds.

They were not invested in mid and small caps at the start of the rally, and the feeling of missing out on what seemed like easy returns was difficult to bear.

There was a palpable risk in such portfolios that was not adequately appreciated.

Since the beginning of 2018, the tables have turned.

While mid and small-cap stocks and mutual funds schemes have struggled, large-cap mutual fund schemes have given good returns.

Even in the large-cap space, the rally has been driven by only a few stocks.

The fund managers who are smart or lucky enough to hold those stocks have done better than others.

In fact, most actively managed large-cap funds have failed to beat the Nifty or Sensex index funds.

What should investors do? Market history suggests that nothing works all the time.

Don't chase the categories that have outperformed recently.

A flavour-of-the-season approach does not work in investing.

Most investors will be better off spreading out their equity investments across the market spectrum.

The sub-allocation to large-cap, mid-cap, small-cap and thematic/sector funds should depend on the investor's risk appetite.

Debt funds carry risks

Elroy Dimson of the London Business School said: 'Risk means more things can happen than will happen.'

When the times are good, we tend to underappreciate risk.

If our short-term experience suggests that nothing untoward has happened, we assume that nothing will go wrong in the future too.

However, just because risk has not materialised in the recent past does not mean it will not materialise in the future.

Don't mistake low probability for no possibility.

There were several instances over the past 18 months when risk materialised in the fixed-income space.

Moreover, the pain did not come in obscure names.

Many prominent financial institutions and promoters defaulted on their obligations.

Many investors had mistaken debt funds and non-convertible debentures (NCDs) to be as safe as bank fixed deposits.

However, the events of the past 18 months have proved this premise to be untenable.

Investors look beyond bank fixed deposits for two reasons -- better tax efficiency and higher yields.

While these are acceptable reasons for investing in debt mutual funds or NCDs, you must appreciate the risk involved.

There is no free lunch.

Tax efficiency and higher yields come with a higher level of risk -- the risk that the underlying bonds can default.

Henceforth, investors must scrutinise (or get a financial advisor to do so) the portfolios of debt funds they invest in for credit risk.

They must also make sure that these portfolios are well diversified with limited exposure to a single issuer and promoter group.

Select your bank carefully

Over one million deposits were adversely affected by the Punjab and Maharashtra Co-operative Bank scam.

The bank management forged its account books to lend over 70% to a single real estate developer.

The Reserve Bank of India imposed restrictions on withdrawals.

Many have lost their entire life's savings in the scam.

Could this have been avoided? Well, that's the job of the regulator and the auditors.

PMC was a fraud. As depositors, there is little we can do to unearth such frauds or fraudulent intentions in advance.

However, we can always aim to reduce the impact of such events.

Even in the past, co-operative banks have failed and depositors have lost money in them.

The level of regulatory oversight is not as high in them as in scheduled and commercial banks.

An acknowledgement of this fact should have made many depositors hedge their bets.

In my opinion, co-operative banks are best avoided.

However, if you must bank with them for convenience or for higher interest rates, put only a limited portion of your assets in these entities.

Beware of jewellery scams

Indians's love affair with gold is well known.

Most jewellers cash in on this by offering gold jewellery schemes, where the buyer deposits a fixed amount with the jeweller for 11 months.

The jeweller adds a 12th instalment and allows the buyer to buy gold jewellery worth the accumulated amount.

While you can dig deeper using a spreadsheet to see if such schemes are indeed useful for the buyer, one thing is for sure.

The entire structure is very similar to a recurring deposit.

The only difference is that the counterparty here is a jeweller, and not a bank.

And therein lies the risk.

There were a few well-publicised instances in 2019 (IMA, Goodwin, etc) of jewellers running away with investors' money.

While these may have been genuine failures, in some cases, the money was routed to unrelated businesses such as real estate.

While these schemes appear attractive, buyers should be mindful of the risks too.

If you must participate in a jewellery scheme, stick to the most reputed brands.

Alternatively, accumulate your money in a bona fide financial instrument and buy the jewellery once you have accumulated the requisite amount.

Remember that good people can take care of bad contracts but good contracts can't take care of bad people.