The general nervousness because of the IL&FS default will prevail in the system for now.

Anup Roy reports.

Illustration: Uttam Ghosh/Rediff.com

Non-banking finance companies (NBFCs), especially housing finance companies (HFCs), could be in for a rough ride in terms of fund-raising plans, as market dries up and interest rates rise.

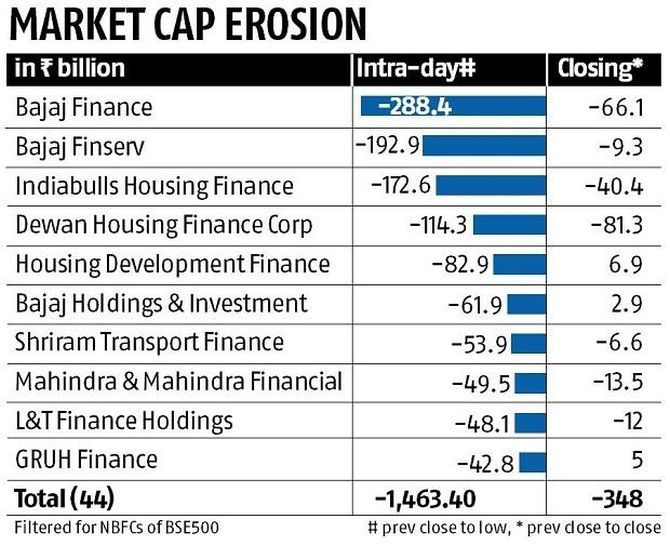

The sharp fall in stocks of major HFCs on September 21, led by DHFL, have clearly shaken the nerves of investors.

Kapil Wadhawan, chairman and managing director, DHFL, said about 60 per cent of the fall in stock was an effect of contagion of the IL&FS sentiment.

"I am sure this has to do with the contagion effect in the market because of the IL&FS issue," Wadhawan said, adding: "Unfortunately, irrational behaviour in the market has led to everybody being painted with the same brush, literally."

Ashwini Kumar Hooda, deputy managing director, Indiabulls Housing Finance, said the intra-day fall of 35 per cent was because of "contagion coming from another housing finance stock whose paper was sold at a higher yield".

Both firms denied having any liquidity problem.

Icra revalidated Indiabulls' Rs 250 billion commercial papers, retaining the rating at A1+.

The liquidity tightness could be the general trend here on and fresh fund raising, by HFCs in particular, could become challenging.

"One of the characteristics of HFCs is that they typically suffer from an asset-liability maturity mismatch, given longer tenor assets and relatively shorter tenor liabilities," said Krishnan Sitaraman, senior director, CRISIL.

HFCs lend money to projects that mature over 10 to 15 years whereas the funds raised have a much shorter maturity profile. To overcome this, HFCs keep themselves liquid.

Some companies keep unutilised bank lines, some invest in liquid MFs, some keep in bank FDs, while some mix and match all three.

"What we look at is how the company manages its ALM profile, and its liquidity policy," Sitaraman said.

HFCs enjoyed higher profitability as borrowing costs reduced in a falling interest environment, but their lending rates did not fall that much, Sitaraman added.

This fiscal, the cost of borrowing is rising in line with the increasing interest rate scenario, but yields on loans have not increased by an equal quantum on account of competitive dynamics.

This is putting some pressure on profitability for HFCs.

However, larger HFCs have been able to buck the trend and manage their profitability better by effecting regular hikes in lending rates.

"For NBFCs, the business is of leveraging. Their borrowings are on the higher side and thus any rise in interest rates become challenging for them. The outlook on interest rates is quite negative," said Naresh Takkar, managing director and group CEO of Icra.

"Fixed income market is under stress and overall liquidity is getting tight," Takkar added.

According to Takkar, NBFCs dependent on short-term borrowings could find it challenging as liquidity tightens in the system.

The general nervousness because of the IL&FS default will prevail in the system for now, Takkar said.

Access to finance is also coming under stress as 11 public sector banks remain under the RBI's restrictive prompt corrective action regime.

Private banks are slowly filling the void, but their balance sheet is not that large.

Good NBFCs will continue to get finance but at a cost.

"HFCs with a strong track record, good parentage, and active liquidity management should be able to manage their liabilities better than the smaller entities," Sitaraman said.