Valuations at current levels have historically corresponded single-digit returns.

Notwithstanding indices being lower than the all-time high levels touched nine months ago, the stock market has rarely been as expensive as it is now on one particular metric.

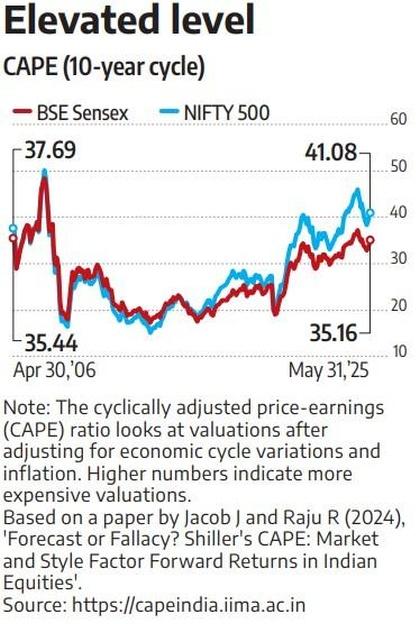

The 10-year cyclically adjusted price-to-earnings (CAPE) ratio for the BSE Sensex is at 35.2x, according to data based on a study, Forecast or Fallacy? Shiller's CAPE: Market and Style Factor Forward Returns in Indian Equities, authored originally in July 2024 by Joshy Jacob, professor at the Indian Institute of Management, Ahmedabad, and Rajan Raju, director at Singapore-based family office Invespar.

The numbers are updated monthly. The latest valuations for May 2025 are typically associated with lower expected returns in the future.

While the traditional price-to-earnings ratio considers valuations that are usually based on the immediate past or near future, the CAPE also considers the longer-term business cycle and adjusts earnings for inflation.

The ratio is popularly called the Shiller PE after Nobel Prize-winning economist R J Shiller, who worked on the measure with John Campbell.

Shiller used the measure to suggest that equities were overvalued just before the dotcom bubble burst in 2000.

The CAPE ratio is currently above the 90th percentile, higher than it has been 90 per cent of the time in data going back to 2003, noted Raju.

'Valuations at current levels have historically corresponded with single-digit forward expected annualised returns for a five-year holding period. This may be mitigated by longer 10-year holding periods, which have corresponded with higher returns relative to five-year holding periods on average,' he said.

The authors added that while CAPE provides valuable insight, it should not be the sole determinant in investment decisions.

The changing nature of Indian firms, with more technology and startups listing, may push up valuations, observed Jacob.

'To some extent, there is improved productivity in Indian firms,' he said.

Still, the broader inverse relationship of the CAPE ratio and future expected returns is expected to hold, as seen in developed markets like the US, according to Jacob.

The Sensex had hit an all-time high of 85,978 in September 2024. It closed at 81,362.

There is still room for earnings growth, which may cause valuations to become less expensive, suggested Chandraprakash Padiyar, senior fund manager at Tata Mutual Fund.

Corporate profit accounted for around 6.8 per cent of gross domestic product during the peak years of 2008 to 2009.

This is currently at around 5.3 per cent. The peak in this cycle could be higher due to structural changes like the formalisation of the economy, which could lead to more business for listed companies, as well as companies making higher profits from every rupee of sales than before.

"Relative to 2008 to 2009, today corporate earnings deliver a far higher profit margin (as much as 400 basis points)," said Padiyar.

A year of time correction may well see valuations look far better as earnings catch up.

There may be lower returns in the short term but more reasonable gains over a three- to five-year period, said Padiyar.

The Nifty 500 index has been trading at higher valuations than the Sensex, suggesting that smaller companies are being valued higher relative to their earnings.

Sizeable inflows into the broader market may have contributed to the gap between the Nifty 500 and the Sensex, noted the authors, reflecting on market dynamics.

The relatively lower float and limited trading activity in smaller companies compared to blue chips -- a 'liquidity premium' -- may have contributed to the widening valuation gap.

The study suggests a direct relationship between CAPE values and drawdowns. Drawdowns are the maximum decline from the peak.

The higher the CAPE, the greater the decline or potential loss. The study suggests that value and low-volatility stocks tend to be more resilient during declines.

Disclaimer: This article is meant for information purposes only. This article and information do not constitute a distribution, an endorsement, an investment advice, an offer to buy or sell or the solicitation of an offer to buy or sell any securities/schemes or any other financial products/investment products mentioned in this article to influence the opinion or behaviour of the investors/recipients.

Any use of the information/any investment and investment related decisions of the investors/recipients are at their sole discretion and risk. Any advice herein is made on a general basis and does not take into account the specific investment objectives of the specific person or group of persons. Opinions expressed herein are subject to change without notice.

Feature Presentation: Rajesh Alva/Rediff