The rupee staged a sharp recovery on Wednesday after suspected heavy dollar selling by the Reserve Bank of India, preventing the battered currency from slipping to a record low on the same day that the authority ushers in a new governor.

Raghuram Rajan, a former chief economist at the International Monetary Fund, takes charge at the RBI as the country faces its worst economic crunch since a balance of payments crisis two decades ago.

In a reminder of the uphill task he faces, a report on Wednesday showed that activity in India's services sector shrank in August for the second straight month for its lowest reading in four years.

It added to a series of data showing the economy struggling for growth.

Gross domestic product figures last week said annual growth had slipped to 4.4 per cent in the April-June quarter, its weakest pace in four years.

The mining and manufacturing sectors contracted from a year earlier.

The country is grappling with a record current account deficit and a hefty budget deficit, factors both weighing on the rupee.

Concerns about rising prices for oil and gold, India's two biggest import items, are keeping pressure on the currency.

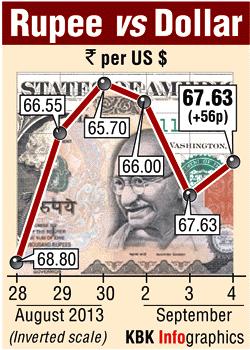

The rupee closed at 67.065/075 to the dollar as against Tuesday's close of 67.63/64.

. . .

It had fallen to 68.62 in early session, not far from its record low of 68.85 seen last week.

Dealers cited heavy central bank intervention via state-run banks, which coupled with dollar selling by foreign banks related to arbitrage opportunities with the offshore rupee market, pulled the rupee sharply back from its day's low of 68.62 per dollar.

The currency hit a record low of 68.85 last week, marking a drop of 20 per cent from the end of 2012.

"The intervention has been aggressive and the best part is it has been consistent today. Even dollar/rupee levels in the offshore and currency futures markets have sharply come down," said Anil Kumar Bhansali, vice president at Mecklai Financial.

Rajan, who famously predicted the 2008 global financial crisis, officially becomes the 23rd governor of the RBI after signing an oath of secrecy on Wednesday.

But he will not take charge operationally until Thursday.

Aware markets are scrutinising everything he says for clues about his intentions, Rajan has been circumspect in public, revealing little about whether he will pursue the policies of his predecessor, Duvvuri Subbarao, or change tack.

"The rupee will be Rajan's first and key challenge.

“His IMF aura may help but he will need to win the market's faith by announcing something which helps bring in dollar inflows," said Vikas Babu Chittiprolu, a senior foreign exchange dealer at state-run Andhra Bank.

. . .

India's economy is reeling mainly from a dearth of investment and a slowdown in manufacturing activity and consumer demand.

Several banks, including Goldman Sachs this week, have cut their GDP growth forecasts to well below the decade low of 5 percent recorded for the year ended in March.

Traders said the economy has also been hit by the extraordinary measures from the RBI under Subbarao, who tightened cash conditions to make it harder to make speculative bets against the rupee and raised short-term interest rates.

Investors are showing little faith the government can push through substantial reforms, such as a hike in subsidised fuel prices, which could help revive confidence in the economy.

Prime Minister Manmohan Singh, in a statement ahead of a trip to Russia to attend the Group of 20 nations' summit on Thursday and Friday, said India would also need a more stable global environment.

"The Summit comes at a time when we in India have introduced several reform measures and taken steps to strengthen macro-economic stability, stabilise the rupee and create a more investor friendly environment," Singh said in a statement.

"At the same time, a stable and supportive external economic environment is also required to revive economic growth."

Global markets are weakening after leaders of a US Senate panel said they reached an agreement on Tuesday on a draft authorisation for the use of military force in Syria, paving the way for a vote by the committee on Wednesday.

Worryingly for India, global crude and gold prices are surging.

Oil and gold imports are big factors in the wide current account deficit.

The prospect that the Federal Reserve will unveil a plan after its policy meeting on September 17-18 to start winding down its monetary stimulus is also weighing on emerging markets, but India has fared worse than most because of the lack of confidence it can address its precarious deficits.

(Additional reporting by Rafael Nam in Mumbai)