The finance minister was expected to announce some sweeping changes in taxation and tax structures. Sadly, Budget day was not the day for it. While he tweaked a little here and a little there on exemptions and deductions, no major changes were made to tax rates or tax slabs.

However, he did promise that these changes would be announced soon. "A comprehensive review should await the proposed income tax code which will be introduced in the Parliament this year," were his exact words.

This is precisely the reason why he has not tampered with the income tax rates for now, the proverbial lull before the storm. It is a widely accepted fact that the existing exemptions and deductions do not constitute an ideal tax structure for the long term.

Aligning all tax saving instruments under the exempt-exempt taxed (EET) regime is a certainty. The only question is, when.

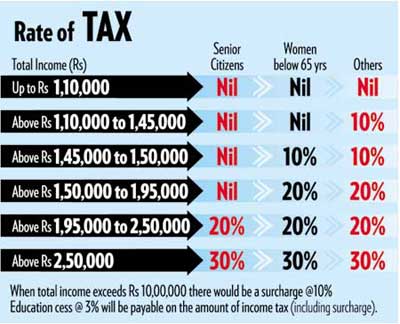

What did the taxpayer get. The tax rates for individual assessees have been kept constant at 10, 20 and 30 per cent of the taxable income for the assessment year 2007-08. These have been in existence since last two assessment years.

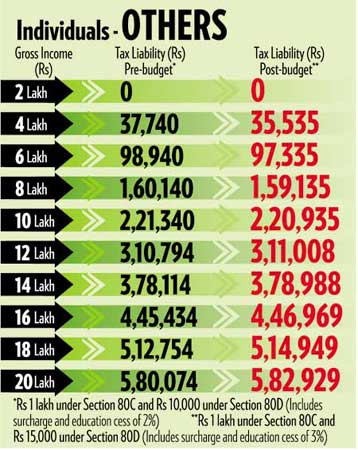

However, the threshold limit of exemption in the case of all individual assessees has been increased by Rs 10,000. Earlier, other than women and senior citizens, those individuals with taxable income up to Rs 1 lakh were not required to pay any tax. Now this limit has been increased to Rs 1.10 lakh. This gives every assessee a relief of Rs 1,000.

However, the threshold limit of exemption in the case of all individual assessees has been increased by Rs 10,000. Earlier, other than women and senior citizens, those individuals with taxable income up to Rs 1 lakh were not required to pay any tax. Now this limit has been increased to Rs 1.10 lakh. This gives every assessee a relief of Rs 1,000.

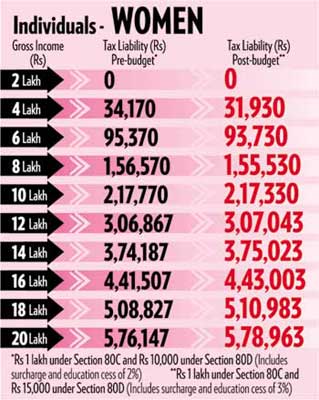

Similarly, in the case of a woman assessee, the threshold limit has now been increased from Rs 1.35 lakh to Rs 1.45 lakh, giving her a relief of Rs 1,000.

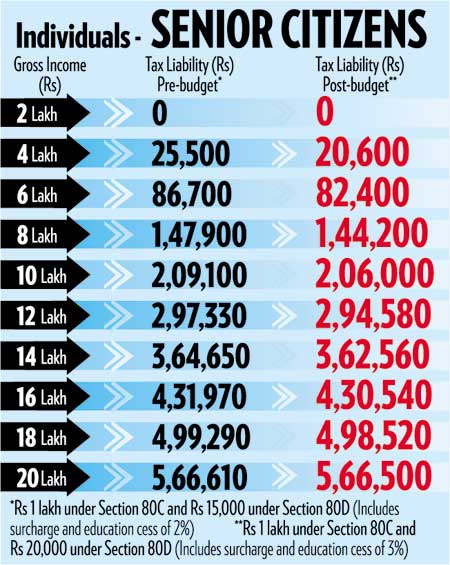

Senior citizens never had it so good in any of the past budgets. The threshold limit of exemption for them has been raised from Rs 1.85 lakh to Rs 1.95 lakh, giving them a relief of Rs 2,000.

The impact. Having said that, the net impact of increasing the tax slabs and the limit for deduction under mediclaim gets diluted to a certain extent by the imposition of additional cess of one per cent. With the existing education cess of two per cent, the total cess on your tax payable becomes three per cent.

Remember, this additional cess is not only on your tax payable, it is also being levied on all products and services covered under excise, customs and service tax. Hence, the impact is widespread, however small the figure might be.

The effective rates after the imposition of cess become 10.3, 20.6 and 30.9 per cent for individuals in the 10, 20 and 30 per cent slabs, respectively. If your taxable income exceeds Rs 10 lakh, the surcharge of 10 per cent continues, and the effective rate for you would be 33.99 per cent.

This Budget's impact would be most felt by tax assessees who are women, senior citizens or those who have a gross income of about Rs 5 lakh. Illustratively, someone with a taxable income of Rs 3.85 lakh would now pay tax of Rs 35,535, a reduction of about 5.85 per cent in taxes.

For taxable income of Rs 8.85 lakh, the impact is marginal at 0.18 per cent. A senior citizen with gross income of Rs 4 lakh gets the maximum benefit from this Budget -- tax reduction of 19.2 per cent.

For taxable income of Rs 8.85 lakh, the impact is marginal at 0.18 per cent. A senior citizen with gross income of Rs 4 lakh gets the maximum benefit from this Budget -- tax reduction of 19.2 per cent.

Healthy action. The action may have just begun on the health insurance front. In the coming year, you can expect more calls from insurance companies offering their health insurance plans. The deduction allowed on medical insurance premium under Section 80D has been increased from the earlier Rs 10,000 in a financial year to a maximum of Rs 15,000.

And, in the case of senior citizens, from Rs 15,000 to a maximum of Rs 20,000. This means that you can knock off another Rs 5,000 from your taxable income. Antony Jacob, managing director, Royal Sundaram Alliance says, "This will encourage more people to buy health insurance, safeguarding their future in times of need ,and will also improve our market penetration."

An exclusive health insurance policy for senior citizens from National Insurance Company, called Varishta Mediclaim, is already in existence. The government has urged the other three public sector insurance companies to offer a similar product.

M. Ramadoss, managing director and chairman, Oriental Insurance has a slightly different view. "We already have a mediclaim policy that covers persons till the age of 85 and also offers a renewal of policy till age of 90. Our policy covers to a sum assured of Rs 5 lakh, while the Varishta Mediclaim policy restricts the sum assured to Rs 1 lakh and critical illness to Rs 2 lakh." He adds, "We will discuss this with the finance ministry, and if need be, we will bring out a specialised product."

Ramdoss is also disappointed by the Finance Minister's move of extending the tax benefit under Section 80(D) for medical insurance by only Rs 5,000. With rising healthcare costs, he expected the limit to be raised to Rs 25,000. "The limit of Rs 10,000 for mediclaim was fixed sometime in 1996-97. Therefore, keeping inflation in mind, it should have been raised to Rs 25,000."

Shikha Sharma, managing director and CEO of ICICI Prudential Life Insurance, also shares this view and adds that the limit for senior citizens should be further enhanced in the years to come, as the cost of healthcare is considerably higher in the older age groups.

Cash tax. As an investor, you may have noticed that at the time of investment, there are certain formalities being undertaken under the know-your-customer norms. This is another step taken by the government to track unaccounted monies and their source and destination.

Cash tax. As an investor, you may have noticed that at the time of investment, there are certain formalities being undertaken under the know-your-customer norms. This is another step taken by the government to track unaccounted monies and their source and destination.

The Banking Cash Transactions Tax (BCTT) also has the same objective. However, the exemption limit on such transactions by individuals and HUFs has been raised from Rs 25,000 to Rs 50, 000.

The bond. Capital gains generated from the sale of any asset may be invested in tax-saving bonds from institutions like Rural Electrification Corporation (REC) and National Highway Authority of India (NHAI). The limit of Rs 50 lakh per investor per year that one can invest in the permissible bonds has been retained. You can continue to invest in these and save on capital gains tax.

The outcome. A senior citizen, with Rs 1 lakh invested in a five-year tax deductible bank fixed deposit, and another Rs 20,000 paid as medical insurance premium, can earn tax-free gross income of up to Rs 3.15 lakh a year, or Rs 26,250 a month. A woman, less than 65 years, can earn tax-free income of up to Rs 2.6 lakh a year, or Rs 22,000 a month. And, a man, below the age of 65, can earn tax-free income of up to Rs 2.25 lakh a year, or Rs 18,750 a month.

Overall, changes in taxes in this Budget don't warrant a celebration, but its benefits are not to be shrugged away, either. But this is not the end, there is more to come.

Tax highlights of the Budget

- Rate of taxes for individuals assesses has been kept constant at 10 and 20 and 30 per cent of the taxable income.

- Threshold limit of exemption in the case of all individual assessee has been increased by Rs 10, 000.

- Income of women tax-payers not taxable till Rs 1.45 lakh.

- Income of senior citizens not taxable till Rs 1.95 lakh.

- Income of all other individual taxpayers not taxable till Rs 1. 10 lakh.

- Imposition of additional cess of one per cent. Existing cess of two per cent continues. Total cess becomes 3 per cent on tax payable.

- Effective rates after the imposition of cess becomes 10.3, 20.6 and 30.9 per cent for various slabs, and 33.99 per cent for those paying surcharge as well.

- Positive impact the most for income tax assessees with gross income of Rs 5 lakh.

- Deduction allowed for medical insurance premium u/s 80D increased to a maximum of Rs 15,000 (Rs 20,000 for senior citizens).

- Banking Cash Transactions Tax (BCTT) raised from Rs 25, 000 to Rs 50,000.

- Rs 50 lakh per investor per year that one can invest in the permissible bonds under section 54 EC continues.

Inputs by Swami Saran Sharma, Bridget S. Leena and Anagh Pal.