In her Christmas speech of 1992, Queen Elizabeth used an old, Latin phrase to describe the year: annus horribilis.

It was a horrible year: three of her children separated from their spouses and a major fire broke out at Windsor Castle, causing enormous damage to the British monarch's residence and destroying priceless artefacts.

Luckily, Anil Ambani hasn't suffered such personal trauma, but for his corporate group, the past few years would certainly merit the 'horribilis' tag.

The Anil Dhirubhai Ambani Group (ADAG, now rechristened the Reliance Group) lost a crucial court battle against Reliance Industries, threatening the future of its power projects.

That, combined with other litigation, business setbacks and questions over corporate governance, has shredded Anil's reputation.

So much so, that the running joke on D-street is that over the past half-decade, ADAG has probably had more litigation in hand than projects. Only, no one's laughing.

. . .

Powered by

All is not well in the Anil Ambani camp. ADAG, with interests in telecom, power, entertainment, infrastructure and even health, is wracked with controversies and charges of poor corporate governance.

Big-ticket projects are yet to get off the ground and funding worries threaten to overwhelm the group.

It wasn't supposed to be like this. In the 2005 settlement between the Ambani brothers, Anil commandeered all the growth businesses (telecom, power and financial services) and seemed determined to take these companies into a higher orbit, starting immediately.

Granted, the businesses were unabashed cash guzzlers and were still in their infancy, but they held out the promise of exponential growth.

And Anil had already earned his stripes in raising capital at Reliance Industries -- apart from being the public face of RIL till the acrimonious split, the kudos for some of the biggest overseas fund-raising exercises at RIL went to him and his pointman, Amitabh Jhunjhunwala.

ADAG certainly got off to a flying start. The stock markets were soaring with strong industrial growth and global tailwinds, and the group's stocks followed suit.

. . .

Powered by

Its companies scaled new peaks, with group market-cap touching Rs 3,44,852 crore (Rs 3,448.52 billion) in early January 2008.

Then came Reliance Power's much-talked-about -- and soon after, disguised -- initial public offer that made a record of sorts, garnering Rs 11,500 crore (Rs 115 billion) from overenthusiastic investors -- both professional managers and the retail public.

What followed was predictable. As sentiment changed on the bourses and an avalanche of selling hit, the hugely overpriced R-Power stock was hammered down, making it one of the worst listings in history for an issue of any meaningful size; the stock ended day one 17% lower than the IPO price.

For a son of Dhirubhai -- the man who created the equity culture in the country -- to crash so spectacularly was disastrous, and unacceptable.

Anil swung into rescue mode, pacifying investors by issuing bonus shares. But, it wasn't enough (even now, the stock is trading at a 51% discount to its issue price) and Anil's woes had just begun.

He took elder brother Mukesh's RIL to court for his share of cheap gas from the KG basin. The fierce, prolonged battle was fought under full media glare and in the corridors of power.

. . .

Powered by

But in vain; in May 2010, the Supreme Court ruled against Anil (ADAG doesn't consider it a loss).

Meanwhile, R-Power had already bagged a fair number of projects. But, till now, only one is off the ground, although the management continues to make pitches about fast-tracking execution.

In project procurements, R-Power's parent R-Infra has also been fairly successful. But, in a bid to outbid competition, the company has been bidding for projects aggressively, possibly compromising on the internal rate of return or making optimistic growth assumptions, feel some industry observers.

Lack of execution, too, appears to be a group-wide problem. Reliance Infrastructure has been similarly hobbled and is now in a Catch-22 situation -- a strong line-up of cash-flow-based projects would have helped it scale up fast, but execution delays have affected its ability to generate those cash flows.

"Execution has been an issue with Reliance Infrastructure," says Sanjeev Prasad, ED and co-head, Kotak Institutional Equities.

More importantly, certain investments in the balance sheet have got analysts worked up.

. . .

Powered by

This is just one reason why the consent order by Sebi last month, banning R-Infra and R-Power from investing in secondary markets, and levying a Rs 50-crore (Rs 500 million) penalty on Anil and some company directors on charges of misquoting certain investments in the books, has analysts and investors wondering whether ADAG has been let off too easily.

ADAG did not respond to emails and telephone calls from Outlook Business.

The poor governance story plays out at Reliance Communications, too, where the tangles are not just because of intensifying competition but flaws in the initial strategy.

If its indecision in choosing a technology platform (the company chose to straddle both GSM and CDMA) for its operations prevented it from having a focused approach to building market-share, its aggressive pricing dragged the company down; RCom has the worst leverage ratio among telcos, with debts of Rs 38,000 crore (Rs 380 billion).

The two other key companies in the group, Reliance Capital and Reliance Entertainment, are on a better footing, but they account for relatively smaller portions of the pie.

Power Play

Before getting into the intricacies, here's a quick look at how Anil's infrastructure business is structured.

. . .

Powered by

ADAG initially divided all these businesses under three group companies -- Reliance Infra (R-Infra), which was originally Reliance Energy; Reliance Power (R-Power) and Reliance Natural Resources (RNRL).

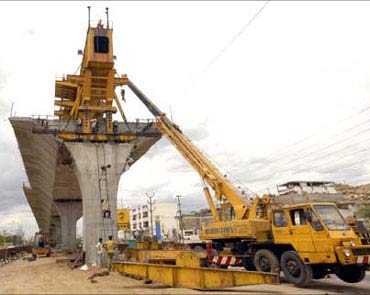

While R-Infra is the parent company for all infrastructure businesses, including cement and EPC, R-Power is the parent for all power generating projects, especially those under construction (R-Infra holds 44% in R-Power).

The operating power units -- the 165 MW Kochi power plant; the 220MW Samalkot plant; the 500 MW Dahanu plant; and the 48 MW Goa plant -- under R-Infra have been spun off into separate, fully-owned subsidiaries. The 600 MW Rosa power plant is the only venture that has come up post 2005, and is part of R-Power.

R-Power also has 14 subsidiary companies, including the three ultra-mega power plants (UMPPs) as well as Rosa Power Supply, which has a capacity of 1,200MW.

RNRL, whose primary business is to source gas from RIL and supply the same to ADAG's gas-based ventures, last year merged with R-Power. (RNRL is also engaged in exploration and production of coal bed methane and owns a gas block in Mizoram.)

On paper, R-Power seems a sure bet. After all, Anil Ambani already has the largest number of UMPPs under his belt. And, if all goes to plan, ADAG could become the country's largest private power player, with 35,000 MW by 2017.

. . .

Powered by

Right now, though, the group has an operating capacity of a little over 1,000 MW, so imagining a 'powerful' R-Power involves making a quantum leap of faith.

The projects that are on track aren't on the same scale as the UMPPs: Rosa II and Butibori have achieved financial closure and have capacities of 600 MW each.

In the UMPPs, R-Power has achieved financial closure for Sasan and Krishnapatnam, which are due to be commissioned in 2013.

The third UMPP, Tilaiya, is scheduled to be commissioned by 2014, but is yet to achieve financial closure.

(Financial closure involves getting all sources of funds in place and, in some cases, signing power-purchase agreements, before beginning major civil work on a power plant. A plant is said to be 'commissioned' when it finally begins producing power to the grid and any delay in closure will have a domino effect on commissioning.)

Incidentally, while the Sasan and Mundra (owned by the Tata Group) UMPPs came up for bidding at the same time (although there were controversies in Sasan), Mundra is likely to be commissioned in Q3 2011.

. . .

Powered by

And although Krishnapatnam has achieved financial closure and imported coal supplies have been tied up, some analysts doubt whether it will be commissioned as scheduled in 2013.

According to them, R-Power presentations say that equipment orders for the project have been placed with R-Infra, but R-Infra's order backlog doesn't reflect this.

Meanwhile, project awards have been mired in controversy -- Sasan is a classic example. At the outset, Lanco's bid of Rs 1.19 per unit was the lowest and was considered shockingly low by the industry -- until other players woke up to the potential of the captive coal blocks associated with the project (if the coal was allowed to be used for other projects, too, it would translate into huge financial gains).

Soon after, it was brought to light that Lanco may not have followed all the bidding norms for the project and in a rare decision, the government annulled Lanco's bid, declaring it 'void ab initio', thereby making the initial second-lowest bidder (R-Power) the real winner.

R-Power then matched Lanco's rate and, subsequently, the government also allowed excess coal from the associated mines to be used for ADAG's other projects.

In effect, the win not only gave the group the 4,000 MW Sasan project, it also infused fresh life into its Chitrangi power project, which has an identical power capacity. One of the other bidders, Tata Power, has now approached the Supreme Court, challenging the change in the conditions on which the project was allotted.

. . .

Powered by

Delays and controversies aren't unique to R-Power; R-Infra has its share as well.

Three of the company's 11 highway projects are yet to achieve closure and traffic flow for some projects is a big concern.

The first phase of the ambitious Mumbai metro project, covering Versova-Andheri-Ghatkopar, is to be completed by June 2011, but is running behind schedule: only 65 per cent of the work is complete.

The Delhi Airport Metro was to be commissioned in time for the Commonwealth Games; it's not been opened yet (to be fair to ADAG, here the asset has been created; this latest delay is because of security issues).

Obviously, delays change the economics of the projects. Says Feedback Ventures chairman Vinayak Chatterjee, "For the group, it is now all about execution. Timelines are critical." Going by the list of projects, ADAG's hands are already full.

Do The Math

It's not surprising that ADAG is struggling to achieve closure for its projects -- back-of-the-envelope calculations show the group has to raise a staggering Rs 1,36,000 crore (Rs 1,360 billion) in the next couple of years just to meet its power sector targets.

Toss in the funding requirements of Anil's other interests -- roads (11 projects); metro rail (three, including two in Mumbai and the Delhi Airport metro); power transmission (five projects) and distribution (Delhi); fuel supply and transportation; airports (five projects); and businesses such as engineering, procurement and construction and cement -- and you're talking of roughly Rs 1,76,000 crore (Rs 1,760 billion).

. . .

Powered by

Following the convention that key infrastructure sectors have a 70:30 debt-equity ratio, R-Infra and R-Power need to raise Rs 52,800 crore (Rs 528 billion) and another Rs 1,23,200 crore (Rs 1,232 billion) as debt.

And if ADAG is to achieve its 2017 target of becoming the largest private power player, these funds have to be secured in the next couple of years at most.

Where will the money come from? Anil hasn't approached the equity market since the Reliance Power IPO as investors are still an unhappy lot.

"If you need capital you cannot have a crisis of confidence. Then, the financiers will extract their pound of flesh," says Gaurav A Parikh, founder of Scriptech, an equity and investment advisory service company.

And then, his pockets are not deep enough to fund the projects in the pipeline either. In FY10, R-Power had a net profit after tax of Rs 273 crore (Rs 2.73 billion).

In contrast, Reliance Infra reported a net profit after tax of Rs 1,151 crore (Rs 11.51 billion) of which, Rs 516 crore (Rs 5.16 billion) was profit after tax from discontinuing operations (the company has transferred some of its power plants and other assets to separate, fully-owned subsidiaries).

. . .

Powered by

Says Scriptech's Parikh, "What will come to his [Anil's] help is the fact that the scale [of Reliance Power] is big and the stakes involved are so high."

It is in the context of this humongous funding requirement that the financial community is questioning Sebi's recent consent order. Has the regulator been too soft on the group by levying a fine that could be paid out of Anil's personal petty cash?

Granted, banning R-Infra and R-Power from investing in secondary market shares doesn't change anything. But if the charges were proven right and there was any evidence of price manipulation in RCom, the companies could have been barred from approaching the secondary market to raise capital -- and that could have scuttled all ADAG's plans.

A 'D' in Corporate Governance

For some analysts, where ADAG will get the money isn't as worrying as what the group will do with it. According to a Macquarie Research report, 52 per cent of the IPO proceeds of Reliance Power had been utilised by the first quarter of the current fiscal and "the bulk of the utilisation in the preceding two quarters had not been with the projects highlighted in the prospectus (Rosa/ Sasan/ Shahapur/ Butibori/ Urthing Sobla)".

Reliance Power raised around $2.5 billion through its IPO and, said the report, some of this "may" have been used to fund the capex for the Indonesian coal blocks for the Krishnapatnam UMPP.

. . .

Powered by

Also, in FY08, R-Infra's balance sheet had Rs 9,700 crore (Rs 97 billion) of investments, of which Rs 7,800 crore (Rs 78 billion) had been given as loans and advances and inter-corporate deposits (ICDs).

Advances to group companies and ICDs are always viewed with suspicion, and concerns over these entries led to a de-rating of R-Infra shares in the following year.

The shares recovered after the management redeployed the bulk of the ICDs in liquid mutual funds, bringing down exposure from Rs 5,060 crore (Rs 50.60 billion) to Rs 1,580 crore (Rs 15.80 billion) in FY09. Last year, though, the ICDs went up again, to Rs 2,760 crore (Rs 27.60 billion).

"The 75 per cent hike in ICDs was a significant disappointment in our view since the management has been guiding to the contrary," wrote Shilpa Krishnan of JP Morgan in a report. Meanwhile, loans and advances have continued to rise (Rs 13,200 crore) in FY10 from Rs 8,600 crore the previous year).

Another grouse is excessive investments in group companies like Sonata Investments (Rs 1,090 crore) and Reliance Infraproject International (Rs 2,330 crore), especially since the management hasn't explained the objective of these investments.

"There is lack of clarity when it comes to related-party transactions," says Prasad of Kotak.

. . .

Powered by

Another iffy transaction on the books relates to the power distribution business in Mumbai, where R-Power didn't source additional power on time in summer 2009.

It later sourced power at higher rates and the tariff that could not be passed on to consumers (Rs 1,602 crore) has been shown in the FY10 balance sheet under a 'tariff adjustment account'. "Those are just glorified debtors," says an analyst.

Also, Anil's decision to merge RNRL with R-Power did not go down well with shareholders as it ended up increasing ADAG's stake by 2% at the cost of minority shareholders whose stake dropped from 15% to 13%.

RCom's Wrong Numbers

If the earlier figures don't ring right, those for RCom are completely out of whack. ADAG's flagship telecom company has been struck by the triple whammy of high debt, slipping revenues and an aggressive accounting policy.

"Both Reliance Infrastructure and RCom follow fairly aggressive accounting practices," says Prasad. Besides, RCom has piled up a mountain of debt -- Rs 38,000 crore (Rs 380 billion) as on September 30, 2010, which will knock off Rs 1,900 crore (Rs 19 billion) in interest payments from this year's profit. Those numbers are just wrong.

Over the past eight months, RCom has tried selling assets to bring in money for growth. On June 6, 2010, the board of directors agreed to sell up to 26% in the company saying it was open to pursuing "appropriate strategic consolidation opportunities" by issuing equity to strategic or private equity investors at a premium to the prevailing market price.

. . .

Powered by

The UAE's Etisalat seemed a sure bet to come on board, but RCom is still single and desperate to mingle.

"It wouldn't make sense for a foreign company to buy into RCom. They want an exorbitant price for a debt-laden company," says a telecom consultant who has worked closely with RCom.

The desperate bid to merge tower assets with the Manoj Tirodkar-promoted GTL Infrastructure also met with a similar fate.

Last June, the companies announced the merger, which would have reduced RCom's debt by Rs 18,000 crore (Rs 180 billion); a few weeks later, GTL unceremoniously called off the deal, with no explanations given.

"We believe it will be increasingly difficult for RCom to monetise tower assets. Given the lack of external tenants at the tower company level, RCom can only benefit from GTL-style transactions, in our view," says Rajiv Sharma, telecom analyst at HSBC Securities and Capital Markets.

RCom's book-keeping is also a red-flag issue. "There is no consistency when it comes to the accounting standards used. This was evident in the treatment of forex gains and losses in RCom in the past three years," says Kotak's Prasad.

. . .

Powered by

The reported FY10 pre-tax profit of Rs 5,260 crore (Rs 52.60 billion) was boosted by Rs 2,700 crore (Rs 27 billion) on account of forex gains booked on translation of foreign currency loans and other liabilities.

But the reported FY09 pre-tax profit of Rs 6,100 crore (Rs 61 billion) did not include forex-related losses of Rs 5,800 crore (Rs 58 billion) in FY2009. Instead, this figure had been adjusted in the balance sheet, notes Prasad.

He further points out that RCom increased the estimated useful life of network equipment to 18 years in FY10 versus seven to 10 years the previous year, which boosted profit before tax by 22% (Rs 950 crore).

Prasad also notes that RCom's reported FY10 net income would have been 71% lower than its reported net income (Rs 1,360 crore versus Rs 4,660 crore reported) if adjusted for the forex-related gains and benefits.

Bottomline management is only part of the problem -- RCom has fallen foul of the Telecom Regulatory Authority of India (Trai) for reporting different sets of revenue numbers.

In 2008, the company reported lower numbers from mobile services to Trai, choosing to pass on some revenue to the internet division; investors were given a different set of numbers. It was alleged that RCom "managed" revenues as the internet service does not require any licence fee renewal, unlike mobile services where 6-10% of the aggregate revenues is paid every year as renewal fees.

. . .

Powered by

The government ordered a special audit of RCom's accounts, but the results are not yet known. Meanwhile, the discrepancy in data continues.

In a report, Kotak's Prasad said the company has attributed the revenue gap between investor reports and regulatory filing to the non-inclusion of VAS revenues and USO subsidies in the revenues reported to the regulator, but "we do not find these items sufficient to justify the 29% difference in gross and 50% difference in net revenues in the most recent quarter."

Way Behind Peers

RCom's problems aren't only about numbers. Operationally, too, it compares unfavourably with Airtel, although both companies are present in the same segments.

In mobile telephony, RCom has the second-largest subscriber base, 125 million compared to Airtel's 150 million. But its average revenue per user (ARPU) is just Rs 122 a month, against Rs 202 for Airtel and Rs 167 for Idea Cellular (figures for July-September 2010).

During that quarter, RCom's Arpu declined 6.3% compared to the previous year, while minutes of usage fell equally sharply to 276. In contrast, Airtel's minutes of usage is 454 per user, per month, while Idea has 394 minutes.

Falling usage indicates a decline in utilisation of the network, and this affects the topline as well as the bottomline.

Besides, network quality is also an issue. "RCom's poor coverage in 2G remains a concern. Current GSM coverage is insufficient and the company needs to invest more in tower infrastructure to meaningfully attract high-end subscribers," says HSBC's Sharma.

. . .

Powered by

The financials for both companies reflect the difference: for Q2FY11, Airtel reported a 24.4% growth leading to revenues of Rs 15,215 crore (Rs 152.15 billion), while RCom grew just 0.2% to reach Rs 5,118 crore (Rs 51.18 billion).

And investors have taken stock, too; in November 2007, RCom and Bharti were running neck and neck in terms of market-cap with a gap of just Rs 9,000 crore (Rs 90 billion). RCom was trading at roughly Rs 1,60,000 crore (Rs 1,600 billion) while Bharti was at Rs 1,69,000 crore (Rs 1,690 billion).

That gap has now widened more than 10 times with RCom plunging to Rs 26,000 crore (Rs 260 billion) and Bharti at Rs 1,24,000 crore (Rs 1,240 billion).

Could 3G turn the tide for RCom? The company paid Rs 8,585 crore (Rs 85.85 billion) for 3G spectrum in 13 circles; introducing those services could help it wean away high-end users from operators like Airtel and Vodafone Essar.

But analysts believe that the cash-strapped firm has not invested adequately in technologies to support 3G services.

"RCom's investment on 3G infrastructure can best be described as 'keeping the lights on'. It has under-invested, and should the subscriber additions turn out to be higher than anticipated, consumers will start experiencing service-quality issues," says Alok Shende, principal analyst at Ascentius Consulting.

. . .

Powered by

Further, with the launch of LTE-based 4G services on the horizon, the risk is that unsatisfied customers will leave for better quality and higher speed 4G services. (WiMax spectrum winners like RIL are gearing up to offer even faster services using the long term evolution platform.)

Another challenge for RCom is the exodus of some key officials. While Prakash Bajpai, the president of RCom's broadband business, quit in June 2008 to start his own venture, two others put in their papers in October last year -- Inder Bajaj, who was heading Reliance Infratel (tower arm), and George Varghese, president for the enterprise broadband business.

The company had to summon its old lieutenant SP Shukla to take over Infratel. "The agenda for transformation is wide. RCom urgently needs to increase the management depth as a key for transformation and continued survival," declares Shende. And now, RCom is embroiled in controversies relating to the allocation of new 2G licences in 2008.

The Silver Lining

Amidst all the controversies and poor showing on corporate governance, it's easy to lose sight of the fact that Anil has made some maverick entrepreneurial moves as well.

In October last year, he tied up with a bunch of Chinese banks (including Bank of China, China Development Bank, The Export Import Bank of China, and Industrial and Commercial Bank of China) for credit to the tune of $12 billion (Rs 56,000 crore), or about 45% of the total debt needed for all of ADAG's infrastructure projects already on hand.

He also signed on Chinese vendor Shanghai Electric for all ADAG's coal-based power plants even as companies like NTPC and even some private power developers are keeping away from Chinese vendors due to quality issues.

. . .

Powered by

With so much at stake, executives say that the Chinese banks will ensure Shanghai Electric pays adequate attention to supplies it makes to RPower.

The money from the Chinese banks would directly go to the vendor and repayment of credit to the Chinese bank would stop in case the plant faces a shutdown on account of faulty equipment, says the executive.

Similarly, Anil's diplomatic skills led to US President Barack Obama acknowledging Reliance Power's Samalkot power plant (for which a Rs 3,500 crore turbine order to ramp up the existing capacity has been placed with US giant General Electric) as creating 1,600 jobs at GE's factory in Schenectady, New York.

Besides, not all his businesses are doing badly. RCapital and REntertainment are on a relatively firmer footing, although the latter has very little by way of execution.

When Anil ventured into the entertainment business in 2005, he had committed to be present across all the media verticals by 2010. While he's lived up to this promise, media experts feel he was over-ambitious.

The media practice head of a leading consulting group says that apart from the radio business and, to some extent, the film business, ADAG has not succeeded in getting anywhere near market leadership position.

. . .

Powered by

"They announced with great pomp and show that they would launch around 11 entertainment channels. They even hired people, but the venture never took off. They finally settled with an English entertainment channel, which is very niche."

She adds it is too early to say whether the group's entertainment business is a success. "They have got into too many verticals at one go. I am not sure whether are they are able to do justice to all of them."

In financial services, Reliance Mutual Funds was the star performer. But ironically, the business case for asset management companies has gone bottom-up, thanks to the no-load regime.

Meanwhile, a question mark hangs over Ambani's wish for RCapital to become a bank, since the Reserve Bank is still holding back on issuing banking licences to corporate houses.

Brothers In Arms?

Meanwhile, the market is abuzz with speculation that some sort of consolidation between the siblings may be in the offing.

. . .

Powered by

Interestingly, the pressure may be mounting even on Mukesh's side -- RIL is throwing up cash of Rs 25,000 crore (Rs 250 billion) annually (once all its exploration assets are fully operational, this will go up substantially), but has been unable to scale up its retail business as well as originally envisaged.

So the group needs to buy good annuity businesses to ensure that its cash is deployed profitably.

Telecom, infrastructure and power are all annuity businesses that fit the bill perfectly for Mukesh. For Anil, this may be the perfect bailout in RCom. R-Infra and R-Power have the projects but lack execution excellence.

Combine this with the Herculean task of raising funds and managing multiple projects, and perhaps reconciliation looks increasingly attractive.

With inputs from Rashmi K Pratap and Ajita Shashidhar.

Powered by