Sales expansion also down 4.4%

With benchmark indices at new highs, Dalal Street is on a roll these days; it has had a good run for much of the current financial year. But this seems to have had little rub-off on corporate results in the October-December quarter. The earnings of the companies that have so far declared their results for the quarter have been among the worst in two years. And, analysts expect the overall numbers to be much worse, as most top companies in the stressed sectors like capital goods, construction & infrastructure, metals & mining, oil marketing, and automobile, are yet to report their earnings.

With benchmark indices at new highs, Dalal Street is on a roll these days; it has had a good run for much of the current financial year. But this seems to have had little rub-off on corporate results in the October-December quarter. The earnings of the companies that have so far declared their results for the quarter have been among the worst in two years. And, analysts expect the overall numbers to be much worse, as most top companies in the stressed sectors like capital goods, construction & infrastructure, metals & mining, oil marketing, and automobile, are yet to report their earnings.

The combined net profit (adjusted for exceptional items) of 290 early-bird companies has grown 2.2 per cent on a year-on-year basis, the slowest rate in eight quarters. This set of companies had reported annual earning growth of 9.8 per cent in the September quarter, and 12.6 per cent in the December quarter of last year.

The companies’ topline growth was worse, indicating the twin problems of a demand drought in the economy and price deflation. The sample’s combined net sales declined 4.4 per cent on a year-on-year basis, the first drop in at least last eight quarters.

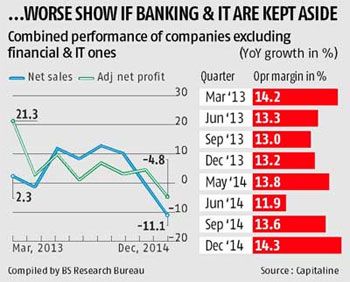

The picture would appear even grimmer if the banking & financial companies and information technology exporters were to be excluded from the sample. Leaving these out, the sample’s combined net profit in the December quarter would be 4.8 per cent lower than a year ago, while its net sales would be 11 per cent down - the worst overall performance in eight quarters.

“These numbers reflect the economic ground reality. The situation has worsened since October and the pain will last for a few quarters before demand begins to rebound. This does not reflect in stock valuations, as the market considers future earning growth, and not past. Stocks are pricing in an economic recovery and faster earning growth from next year,” says G Chokkalingam, founder & chief executive, Equinomics Research & Advisory.

There was some good news for the bulls, though, in lower commodity prices providing a little comfort to corporate earnings. The companies’ bottom lines were also cushioned by higher other incomes, as bonds and equities helped them book treasury profits.

There was some good news for the bulls, though, in lower commodity prices providing a little comfort to corporate earnings. The companies’ bottom lines were also cushioned by higher other incomes, as bonds and equities helped them book treasury profits.

The raw material cost for the companies in the sample, excluding financial & IT ones, declined 22.7 per cent in the December quarter on a year-on-year basis.

This led to a 68-basis-point sequential — and a 115-basis-point annual — improvement in core operating margins (excluding other income) to 14.3 per cent of net sales.

One basis point is the hundredth of a percentage point.

The combined other income for the sample in the December quarter rose 30.9 per cent annually - down from 44 per cent in the previous quarter but a sharp improvement from the 6.4 per cent in the corresponding quarter of last year.

After excluding financial and IT companies from the sample, annual growth in combined other income comes to 30 per cent, compared with 48.6 per cent in the previous quarter and 7.5 per cent in the December quarter of last year. Other income accounts for a fifth of these companies’ operating profit (earnings before interest, tax, depreciation and amortisation), up from 15.8 per cent in the year-ago period.

In the previous quarters of this financial year, IT exporters like Tata Consultancy Services (TCS), Infosys, Wipro, HCL Tech and Tech Mahindra, had more than made up for a poor show by industrial and manufacturing companies. This comfort is missing in October-December, as IT exporters have reported their worst quarter in two years; industry bellwether TCS reported near-flat profit growth.

The IT companies’ combined annual net profit growth stood at 6.3 per cent, down from 15.4 per cent in the previous quarter and 32.7 per cent in the corresponding quarter of last year. Analysts attribute this to a continued economic slowdown in the euro zone and Japan negating the upside from the US.

The IT companies’ combined annual net profit growth stood at 6.3 per cent, down from 15.4 per cent in the previous quarter and 32.7 per cent in the corresponding quarter of last year. Analysts attribute this to a continued economic slowdown in the euro zone and Japan negating the upside from the US.

The other early-bird companies seem to confirm a growing disconnect between the stock market and the underlying economic and corporate fundamentals. “With each passing quarter, the gap between market expectations and actual delivery by companies is widening. Stock indices continue to hit new highs, even as earning downgrades increase.

At this rate, the price-earnings valuations of benchmark indices like the Sensex will enter the bubble zone,” says Dhananjay Sinha, co-head (institutional research), Emkay Global Financial Services.

According to Sinha, incremental liquidity flows on account of actions by major central banks are now a much bigger factor for the markets than corporate earnings. So long as bulls have access to liquidity, they will continue to bid-up stock prices, regardless of earnings, in the absence of alternative assets.