The fundamentals of investing remain the same for all categories of investors and that includes the youth. On the same lines, the investment avenues at the disposal of the investor coincide for all categories. Of course, you have to discount for some investments like the Senior Citizens Savings Scheme that are off-limits for the youth!

We have short-listed the three most important investment avenues that the youth must consider while building a portfolio. While two of these - mutual funds and assured return schemes qualify as investment avenues, the third i.e. life insurance is not really an investment avenue in the strictest sense. However, insurance has been included in our note for some compelling reasons.

Mutual funds are a convenient way to invest in equities and debt for investors who do not have a great deal of knowledge about these asset classes. Life insurance on the other hand, while not strictly an investment avenue, is a must in every individual's portfolio. Life insurance has so many aspects to it - life cover, savings and retirement planning among others, all of which are as relevant to the youth as they are to the next investor.

- To find out about the top 25 MFs, click here

At Personalfn we are unabashed fans of mutual fund investing. That is not to say mutual funds do not have any negatives, it's just that the positives far outweigh them. For sheer convenience and 'ease of use' to borrow a term from a technical manual, mutual funds have no peers.

While there a host of benefits associated with mutual funds, if we have to highlight the most significant, they would be:

Convenience

For investors who do not have the time, inclination and ability to research stock and debt markets, mutual funds are a very convenient investment tool.

Simplicity

Mutual funds are relatively hassle-free. Opening demat accounts and broker accounts are alien to the mutual fund investor. He only needs a bank account. He only needs to write a cheque to the mutual fund he wishes to invest in. And customer service levels among asset management companies and banks have reached a level, where even cheque-writing has now become redundant; funds can be transferred directly from your bank account to the AMC via the ECS facility (electronic clearing service).

Financial planning

Mutual funds are a great way to plan for life's most important milestones like education and marriage, retirement, buying a house or a car. In fact, there are mutual funds that are designed specifically to achieve these milestones.

A place for everyone

Mutual funds are all-inclusive. There is place for all kinds of investors. While stocks and debt instruments are ideally suited for investors with a certain level of risk appetite, mutual funds can fit into just about every investor's portfolio by virtue of the wide variety of products they offer. You have equity funds, debt funds, balanced funds (that invest in equity and debt) and several other fund categories that offer the most interesting investment options to investors across the board.

- To find out about the top 25 MFs, click here

If investors were only aware of the various mutual fund products at their disposal, they would be in a better position to appreciate the last point we have made. Since mutual funds invest across equity and debt markets, they throw up a string of categories:

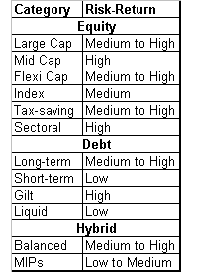

(Please note that the risk-reward remark is for that category only, it is not relative to other categories. For instance, 'medium to high' risk-reward for large cap equity funds is not the same as 'medium to high' risk-reward for balance fund.)

Equity funds

Mutual funds that can invest the entire corpus in equities are called equity funds. Equity funds carry maximum risk because the entire money (or most of it) is allocated to stocks. The fortunes of your equity fund investment are linked to stock markets, which can be quite volatile over the short-term (less than three years).

However, over the long-term you stand a much better chance of accumulating wealth at relatively lower risk. For the youth, equity funds are an ideal way to build wealth over the long term given that they have time on their side.

Equity funds come in various 'shapes and forms'. Depending on where and how the fund manager allocates monies across equity markets, you have various mutual fund categories. We have highlighted some of the popular equity fund categories:

Large cap equity funds

These funds invest predominantly in companies with a large market capitalisation (large caps). While the definition of 'large caps' varies across AMCs, a lot of them consider the 'top 100 companies by market capitalisation' for the purpose of investment. Within the diversified equity fund segment, large cap funds are relatively lower risk since large caps are well-researched and have established track records.

Mid cap equity funds

These funds invest predominantly in companies with a 'medium' market capitalisation (mid caps). Again there is no standard definition of 'mid caps' across AMCs. AMCs usually consider the level below their own large cap level while selecting mid caps.

- To find out about the top 25 MFs, click here

Contrary to their large cap peers, mid cap stocks (and therefore mid cap funds) carry above-average risk. This is because information on mid caps is not widely available so there could be some unpleasant surprises for investors if they misinterpret the company data.

Flexi cap equity funds

As the name suggests these funds can invest across large caps and mid caps depending on which segment presents the most attractive investment opportunities. In terms of risk, they lie between large cap funds and mid cap funds.

Index funds

An Index Fund is the most fundamental equity fund category. Also known as passive funds (other equity funds are known as active funds), these funds invest in the same companies as their benchmark index (BSE Sensex or S&P CNX Nifty for instance) in exactly the same proportion. This ensures that the fund gives a return in line with the index even if it cannot outperform it. In terms of risk, index funds have a lower risk profile than an actively managed diversified equity fund.

Index funds are particularly relevant in the context of developed markets where the fund manager cannot outperform the index as easily. In the Indian context, fund managers are still able to outperform the index, so investors prefer actively managed funds to index funds. Index funds also benefit from lower fund management costs; again this is something that is yet to unfold in the Indian context compared to the truly lean costs of index funds in the US for instance.

Tax-saving funds

For all practical purposes, tax-saving funds or equity-linked savings scheme (ELSS) are regular diversified equity funds except for two differences - they offer investors a tax benefit under Section 80C and your investment in tax-saving funds is subject to a 3-Yr lock-in. We have discussed this category in some detail in the article on Section 80C.

Sector/Thematic funds

Sector/thematic funds invest in a particular sector/theme. Equity funds that invest only in software companies (i.e. Technology/Software Funds) or pharma companies (Pharma Funds) or consumer products companies (FMCG Funds) are examples of sector funds.

On the same lines funds that invest in a particular theme - infrastructure or outsourcing are called Thematic Funds. The risks associated with sector/thematic funds are the highest since there is a restriction on the fund manager's investment options and he cannot invest elsewhere if the sector/theme loses its appeal in the stock markets.

Debt funds

Debt funds invest in debt securities - fixed income bonds, floating rate bonds, government securities (gsecs/gilts) and call money to name a few. While debt funds are perceived to be low risk, they do take on credit risk (by investing in lower rated AA/A paper) as well as interest rate risk (by investing in paper with varying maturities). Like equity funds, debt funds also have several categories:

Long term debt funds

These funds invest in debt instruments that have a maturity of more than a year. That is why debt instruments that form part of the fund's investments are mainly long term corporate bonds and gsecs. Ideally, investments in long term debt funds must be made with a time frame of about 12-18 months.

Floating rate funds

When a debt fund invests primarily in long term floating rate instruments (where the coupon rate is revised at regular intervals), it's categorised as a floating rate debt fund. Investing in a floating rate fund is particularly beneficial at a time when there is uncertainty about interest rates.

Short term debt funds

When debt funds invest primarily in instruments with a maturity of less than a year, they are called short-term debt funds. As with their long term counterparts, there is also a category of short term debt funds that invest primarily in floating rate instruments. These are called 'Short term Floating Rate Funds'. Ideally, investments in short term debt funds must be made with a time frame of about 3-6 months.

Gilt funds

Debt funds that invest primarily in gsecs are called 'Gilt/Gsec Funds'. These funds avoid corporate bonds. They are the equivalent of sector funds on the equity side; since they do not diversify across debt instruments, they carry above-average risk. Moreover, compared to corporate bond prices, gsec prices are often more volatile.

Liquid funds

These funds invest mainly in debt instruments with very short maturities (less than 30 days). Call money, treasury bills, certificate of deposits, short term bank deposits and cash are the main constituents of a liquid fund portfolio. For investors who want to set aside money for less than 3 months with the primary objective of preserving capital, must consider investing in liquid funds.

Hybrid funds

As the name suggests, these funds do not restrict themselves to one asset class (equity or debt), they invest in both asset classes. There are two significant categories within this segment:

Balanced funds

Balanced funds invest pre-dominantly in equity markets i.e. usually over 65 per cent of the corpus is invested in equities. The balance is invested in debt market instruments. Balanced funds are ideal for investors who do not have the risk appetite for a 100 per cent equity investment. Like equity funds, they need to be considered with a minimum 3-yr investment time frame.

Monthly Income Plans

The term 'MIPs' is rather misleading because it leads a lot of investors into believing that these funds give something a regular income/dividend. The fine print 'MIPs do not assure returns' hardly catches their eye. Nonetheless, MIPs like balanced funds are 'asset allocation' investments because they allow investors an opportunity to access both equity and debt markets. Unlike balanced funds, MIPs have a much smaller allocation to equities (ranging from 10-25 per cent). Investors need to consider MIPs with a minimum 18 month investment horizon.

By Personalfn.com, a financial planning initiative

Money Simplified - 5 Sectors to invest in. Get it now. Its free!