There are three options available to us whenever we invest in a mutual fund - growth, dividend payout and dividend reinvestment. Many investors are not very sure as to which option is better.

In one of my earlier articles, I had with the help of an example, shown that the basic returns from all 3 options are same. So the choice of option will, technically speaking, make no difference to your basic returns.

However, the choice of option can make a difference in the final returns because of a couple of other factors.

When the dividend earned is not reinvested, the returns from a Dividend Payout option will be somewhat lower than dividend reinvestment or growth option. In other words, it is our investment strategy, which will affect the returns, not the choice of option per se.

The applicable tax rate on the type of fund (debt or equity), the holding period (less than or more than 1 year) and the type of earning (i.e. dividend or capital gains) is different. Hence the post-tax return under different options will differ. The major impact, though, is on debt funds. Again an external factor viz. tax which affects the final returns.

While, we considered the tax aspect in the aforesaid article, in this article let us take the first point forward and see how much impact it can make.

Before we do that, here are a few investing traits commonly found amongst the investors:

Psychologically it is quite comforting to receive cash from our investments from time to time. Therefore, even if we may not need this money, many times we still opt for dividend payout option

We diversify our investments across many funds, which of course, is a good thing to do. But it also means that the dividends that we receive are a few hundred or thousand rupees. Since the individual dividend amounts are small, we generally tend to spend it rather than reinvest it.

By doing so, we lose out on the full benefits of compounding. All profits earned are, of course, not distributed as dividend. Since they remain in the fund, we earn compounding benefit on that amount. But we lose the benefit of compounding on the amount distributed as dividend. (Even if we were to later reinvest this dividend, there is some time lost in between and also we may have to pay entry loads.)

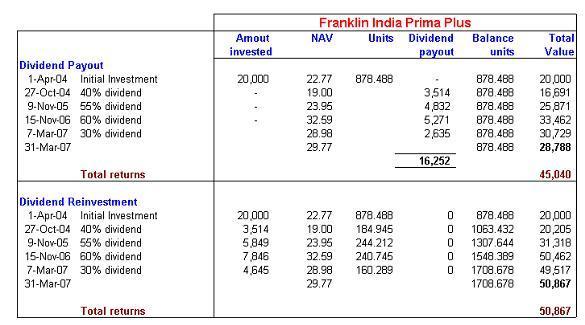

Now let us take an example and see what we stand to lose if we choose dividend payout option vis-a-vis dividend reinvestment (or growth) option. Of course, kindly remember that here we are basically discussing equity funds and long-term investment horizon.

Suppose we invested Rs 20,000 in Franklin India Prima Plus Fund on April 1, 2004. And the dividends we received were not reinvested, but were spent.

As we can we see from the above table, over a long-term period i.e. 3 years in this particular example, the returns from dividend payout work out somewhat lower at 31 per cent p.a. as compared to 37 per cent p.a. in dividend reinvestment option. In absolute terms this works out to about Rs 5,800 less money in the dividend payout option. Therefore, from the returns point of view, we earn less. The difference, though, is not that significant.

But this is just one fund with a 3-year time period. Add to it the loss from 10-15 other funds that we may be holding for 10-15 years and you can imagine how big difference it can make.

Also, the more significant impact is on 'wealth creation'. As on Mar 31, 2007 the corpus we have in hand is just Rs 28,788 in the dividend payout option as against Rs 50,867 in the dividend reinvestment option i.e. almost half.

The point is that if we keep spending our dividends, it will be very difficult to build long-term wealth for our retirement, children's education & marriage or such other long-term needs.

The bottom line is that let the money work harder for you. Let your money remain invested. Even if they may seem to be small and insignificant amounts, these dividends and their compounding effect will add-up to a large amount. Besides, if you need money you can always conveniently sell a few units.

The author is an investment advisor and promoter of wealtharchitects.in. He can be reached at sanjay.matai@moneycontrol.com.

For more on mutual funds, log on to www.easymf.com