|

|

|

|

|

| HOME | MONEY | REAL ESTATE | TRENDS | |||

|

October 6, 1999

NEWS

|

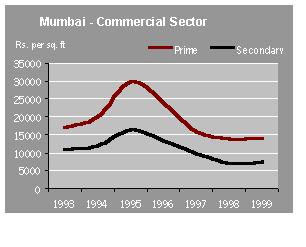

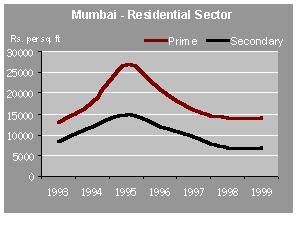

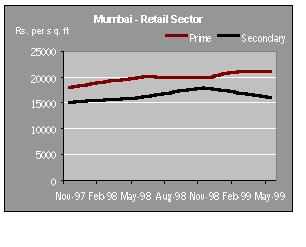

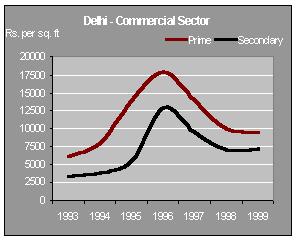

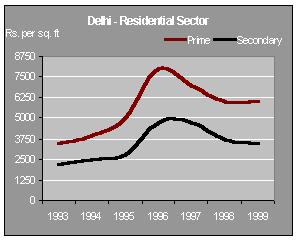

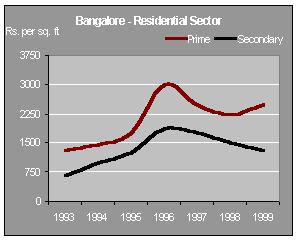

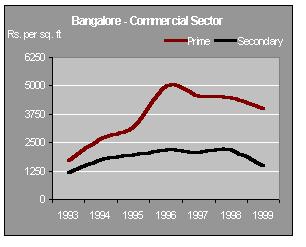

Retail and entertainment are the buzzwordsREAL ESTATE IN INDIA: WATCHING THE MARKETS PROPERTY MARKET With the economy finally showing positive indications, the property markets have started to stabilize. Most Housing Finance companies are providing attractive schemes like reducing interest rate, flexible payment facilities linked to the growth in income of the borrower. This coupled with increase in FDI and a positive stock market has resulted in increased activity in the real estate market. Although the prices continue to be low, there has been a renewed activity in all segments of the property market. With HUDCO entering the Housing Finance market, the competition has started hotting up. Housing finance cos. are concentrating on actual users and have devised schemes to suit their needs. Similarly, with regards to the commercial and retail markets there has been a significant change in the trends. With retail and entertainment becoming the buzzword and large corporates entering the fray this segment is all set to grow. However the ambiguity with regards to policy matters continues on account of the political uncertainty. Both state and central govt. are yet to come out with a clear policy on the following issues 1) FDI in housing 2) Core industry status for construction 3) Modification / repeal of the ULCRA by state governments. Now much would depend on the formation of a stable government and its ability to drive the economy. PRICES AND RENTS MUMBAIThere is a noticeable increase in the demand for residential and good quality commercial space. Although the prices of residential space continue to be soft, the volumes have improved compared to same quarter last year. Good commercial space in the suburbs of Andheri and Bandra now command rentals which are almost equal to that prevailing in secondary buildings in prime areas. OFFICE SECTOR In this sector there is a constant movement towards suburbs like Bandra-Kurla and Andheri (E). This has resulted in a rise in rental values in these locations. The rates prevail in the range of Rs 60-80 per sq ft per month with some premium building commanding as high as Rs 120. This is almost equal to rentals prevailing in CBDs like Nariman Point. However, the capital values in the suburbs have not moved in tandem with the lease rentals and have stabilized at 6000 to 7000 Rs/ sq ft.. The values in the prime CBDs haven't seen significant movements and have stabilized at Rs10000 to Rs15000 per sq ft.. The average rentals prevailing here are Rs 100 - 135 per sq. ft per month. RESIDENTIAL SECTOR The residential sector witnessed some positive activity. Prominent developers in Mumbai have reported increase in demand compared with the corresponding period last year. This increase can be attributed to an increase in demand for middle income housing projects. Most Housing finance companies have come out with various attractive schemes to suit the requirements of first time buyers. There has not been a significant change in other segments of the residential sector. The capital values in prime areas continued to be depressed and are prevailing in the range of Rs 9000-14000 and those in secondary areas prevail in the range of Rs.5000-8000. Studies have indicated that there is a potential demand for middle income housing projects that offer value for money. RETAIL SECTOR Retail worldwide has been the most profitable sector of the real estate industry. But in India this has not been the case. Its only now, with large Corporates venturing into the retail sector, that there has been a flurry of activity. There is a potential demand for large retail space in malls and other comprehensive developments. However there has not been any significant change in the retail market. The rentals in the prime and secondary areas continue to be around Rs 250 and Rs 200 per sq ft per month respectively. The capital values have now stabilized at Rs 21000 for primary area and Rs 16,000 for secondary area. DELHI Real estate prices in Delhi today are perhaps at the lowest in recent times. There are indications that suggest that the markets are bottoming out and now the prices and rentals would stabilize. OFFICE SECTOR Few corporates have shifted from the secondary locations to the CBD taking advantage of the falling rental values. There is increased activity in the CBD inspite of the factors like parking problem, poor maintenance of buildings & lack of power backup facility. There has been no significant change in the capital values of prime and secondary areas, which continue to be in the range of Rs 9000 - 10,000 per sq. ft. and Rs 6500 - 7500 per sq. ft respectively. On the other hand the lease market rates prevailed in the range of Rs 80 - 110 per sq. ft. per month and Rs 40 - 60 per sq. ft per month in prime and secondary areas respectively. RESIDENTIAL SECTOR In residential sector demand for premium leased space Rs 150,000 to 200,000 is still sluggish. However the lease market in the middle segment has seen good activity, the demand mainly coming from Embassy personnel, senior officials of MNC's and Indian corporates. There has been no change in the capital values in the prime & secondary areas which continue to be in the range of Re 5500 to 6300 and Rs 3500 to 4000 per sq. ft respectively. Same is the case with lease rentals. The rentals in prime and secondary areas continue to be Rs 40 - 50 and Rs 25-30 for prime and secondary areas respectively. RETAIL SECTOR The overall demand for leased and outright retail space in Delhi continues to be sluggish. Delhi retail market is characterized by acute shortage of quality retail space. In the absence of proper planning illegal constructions have prospered, leading to problems of parking space, water supply & electricity, at all major retail locations. Quite a few quality retail projects are in the pipeline. The capital values in the prime areas like Connaught Place, South Extension and Karol Bagh continue to be in the range of Rs 12000 - 14000 per sq. ft and that in the secondary areas like Green Park and Lajpath Nagar continue to be in the range of Rs 9000 - 11000 per sq. ft. The lease rentals in the prime and secondary area continues to be in the range of Rs 180 - 200 and Rs 100 - 150 per sq. ft per month respectively. BANGALORE Bangalore seems to have finally woken up to the threat posed by Hyderabad and Chennai to its booming software industry. Karnataka govt. has come up with various schemes to upgrade the existing infrastructure and even the builders have started value-added services like property management and customization of development as per user requirements. OFFICE SECTOR The Bangalore commercial real estate market is primarily driven by IT sector. Although there is an emerging trend among these companies to move to suburbs from the CBDs' because of better infrastructure and low real estate prices, there is clear indication that these companies are hungry for good quality office space. Most of the good quality ready stock in the CBD has been absorbed. The Capital values in the prime & secondary areas have declined marginally and are now in the range of Rs 3800 - Rs 4800 & Rs 1700 - 2200 respectively. However the rentals have stayed firm in the prime and secondary areas and continue to be in the range of Rs 40 - 50 & Rs15- 20 per sq. ft. per month respectively. RESIDENTIAL SECTOR As in other prime cities, there has been increased activity in budget and lower end housing in Bangalore. This demand is mainly propelled by attractive housing finance schemes. In prime areas the demand continues to be sluggish on account of high cost . There is however demand for quality housing in prime areas, apartments done by reputed builders are still able to find buyers and lessees. Otherwise there is a situation of oversupply in prime areas. The capital values in the prime areas ranges between Rs 2200 - Rs 3500 per sq ft. The rental values prevailing in prime areas also have not witnessed significant changes and continue to be in the range of Rs 13 - 16 per sq. ft. per month. RETAIL SECTOR Bangalore has always been a shopper's paradise. The retail sector in Bangalore is getting more organised and designated shopping streets are gradually accommodating large departmental stores which offer the 'shopping experience'. Specialty stores like Health & Glow, Music World are testing waters before they embark upon a chain of such stores. The retail activity is gradually moving to, some up-market residential areas like Jayanagar, Indiranagar, Vijayanagar, Koramangala etc. These retail locations cater to the local population at large. There are also some destination shopping centers which attracts shoppers from all areas of Bangalore. This has resulted in increased demand in the secondary areas. There is no significant change in the capital values in prime and secondary areas which continue to be in the range of Rs 3000 - Rs 5000 and Rs 1000 - Rs 2500 respectively. The city was not affected by the general real estate slump witnessed by the major Indian cities till about a year back. The real estate situation in the city improved after 1993. The property prices in the city started rising since mid 1995 & the development activity picked up in the following years. The market however seems to be stagnant at present. This could be attributed to the overall liquidity crunch and the general slowdown in the Indian Economy. This market has very few speculators and is actually dominated by the end users. OFFICE SECTOR The office sector currently seems to be sluggish with oversupply of office space. Hyderabad does suffer from a lack of A grade office space in terms of construction quality and the availability of parking space. Some of the well established builders are now giving importance to common areas and parking.The constructions of the Cyber Towers located at the now famous HI TEC city in Madhapur has spurred a lot of activity in that area. There are a few corporates like WIPRO, BAAN who have built their independent development centers in Madhapur. However the demand for the Cyber Towers is also quite sluggish with rate of 50%. The prime area would comprise Sardar Patel road to Banjara Circle as well as parts of the Rajbhavan Road. The secondary locations would comprise Sarojini Devi Road, Banjara Hills & Himayat nagar. The Capital values for prime and secondary areas are much lower as compared to places like Bangalore and re in the range of Rs 1800 - 2000 and Rs 1200- 1700 respectively. The lease rental for primary and secondary areas are in the range of Rs 16- 20 & Rs 10 - 15 per sq. ft. per month respectively.Developing markets RESIDENTIAL SECTOR The prime residential comprise of Banjara Hills, Jubilee Hills Somajiguda, RajBhavan Road & Adarsh nagar Banjara and Jubilee Hills are mostly bungalows which range between 3500 sq ft to 5000 sq. ft. Somajiguda, Raj Bhavan Road , Adarsh nagar offer flats which are centrally and conveniently located The secondary areas comprise Durganagar, Himayatnagar, Srinagar Colony, Begumpet, Ameerpet, Marredpally, Gunrock Enclave . The residential sector unlike the other sectors has witnessed some activity as more and more IT companies are considering it as an alternative to Bangalore. The capital value in the prime and secondary area is in the range of Rs 1300 - 1800 & Rs 900 - 1200 respectively. The rentals are the range of Rs 6 - 10 per sq. ft. per month for prime area and Rs 3 - 6 per sq. ft. per month for secondary area. RETAIL SECTOR The retail space is perhaps the only sector which is witnessing hectic activity. All units that enjoy good visibility are picked up almost immediately. While the rest of the areas of the development are sluggish in terms of occupancy. The main retail markets of Hyderabad are Abids and Somajiguda in Hyderabad and MG Road and Rastrapathi Road in Secunderabad. The capital values in the prime and secondary area are in the range of Rs 6000 - 8000 & Rs 4000 - 5500 per sq. ft. respectively. The rental values for prime and secondary area are in the range of Rs 50 - 70 & Rs 30 - 45 per sq. ft. per month respectively. BROOKE INTERNATIONAL (INDIA) Pvt. Ltd. |

||

|

HOME |

NEWS |

ELECTION 99 |

BUSINESS |

SPORTS |

MOVIES |

CHAT |

INFOTECH |

TRAVEL SINGLES | BOOK SHOP | MUSIC SHOP | HOTEL RESERVATIONS | WORLD CUP 99 EDUCATION | PERSONAL HOMEPAGES | FREE EMAIL | FEEDBACK |

|||