In eight months, India has already imported gold worth $24.4 billion; at this rate, the golden metal might squeeze our external balance.

According to 2013-2014 data, India had trade deficit with 81 countries. Top 10 countries with which India's trade deficit had widened during that period are China, Kuwait, Qatar, Venezuela, Indonesia, Korea, Angola, Japan, Belgium, UAE and Mexico. Trade deficit happens when a country's imports exceeds its exports. Is gold causing a rise in deficit?

A report by financial services firm Anand Rathi points towards that direction.

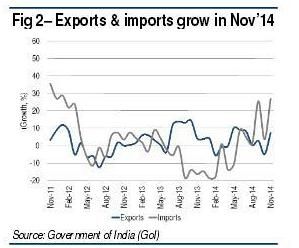

India’s trade deficit widened to $16.9 billion in November.

Despite the global economic slowdown, exports expanded 7.3 per cent.

Imports (26.8 per cent) continued to rise even as the steep fall in oil imports (down 9.7 per cent) was counter-balanced by the high non-oil import growth (26.8 per cent).

Gold imports were high, with year to date gold imports at $24.4 billion.

The short-term risk to our external balances stems from the yellow metal.

We feel that the Reserve Bank of India may resort to higher duties to curb the appetite for gold.

Exports correct in November: From a 5 per cent contraction in October, exports soared to 7.3 per cent in November.

While in absolute terms, exports were $26 billion, the favourable (low) base helped attain the high-growth figure.

Also, high growth was noted in gems and jewellery, engineering goods and textiles among others.

With it, year to date export growth has increased to 3.8 per cent.

Imports rise on account of high non-oil imports: Import growth reverted to a high 26.8 per cent in November, after it had slowed to 3.6 per cent in October.

In absolute terms, imports rose to $42.8 billion.

Year to date import growth has picked up to 4.6 per cent.

Oil imports in contraction: In line with expectations (falling crude prices), oil growth contracted 9.7 per cent in November (vs. 19.1 per cent in October).

Low crude prices reduced the absolute figure to a 29-month low of $11.7. Year to date, oil imports have contracted 1.5 per cent.

Non-oil imports cross $30bn: Non-oil imports grew 49.6 per cent, a 42-month high (vs. 18.9 per cent in October).

In absolute terms, the rise in non-oil imports, from $27.1 billion to $31 billion, can be partly accounted for by the rise in gold imports (an additional $1.4 billion) and in engineering goods and fertilisers.

Trade deficit at 18-month high: In November, the foreign-trade deficit widened to $16.9billion, from $13.4billion in October.

The April-November deficit is a comfortable $103.1 billion.

Services trade surplus slips in October: The services trade data showed that the trade surplus declined to $6.2 billion (vs. $6.8 billion).

Exports and imports, both fell, to, respectively, $12.1 billion (vs. $12.9 billion the previous month) and $5.9 billion (vs. $6.2 billion).

Assessment and outlook: Despite the global stagnation, the growth in exports is reassuring.

Assessment and outlook: Despite the global stagnation, the growth in exports is reassuring.

The surge in imports, primarily of gold, is, however, worrying.

In eight months, India has already imported gold worth $24.4 billion; at this rate, the golden metal might squeeze our external balance.

We feel that the RBI might increase duties or revert to the 80:20 rule to curtail the appetite for gold.

An increase in crude prices now, to $100/barrel looks stretched.

In addition, active currency management by the Reserve Bank of India has kept at bay volatility in the rupee.