| « Back to article | Print this article |

The fact is that you cannot get rich without taking risks. Risks and rewards go hand in hand; and, typically, higher the risk you take, higher the returns you can expect. In fact, the first major Zurich Axiom on risk says: "Worry is not a sickness but a sign of health. If you are not worried, you are not risking enough". Then the minor axiom says: "Always play for meaningful stakes".

The secret, in other words, is to take calculated risks, not reckless risks.

In financial terms, among other things, it implies the possibility of receiving lower than expected return, or not receiving any return at all, or even not getting your principal amount back.

Every investment opportunity carries some risks or the other. In some investments, a certain type of risk may be predominant, and others not so significant. A full understanding of the various important risks is essential for taking calculated risks and making sensible investment decisions.

Seven major risks are present in varying degrees in different types of investments.

Default risk

This is the most frightening of all investment risks. The risk of non-payment refers to both the principal and the interest. For all unsecured loans, e.g. loans based on promissory notes, company deposits, etc., this risk is very high. Since there is no security attached, you can do nothing except, of course, go to a court when there is a default in refund of capital or payment of accrued interest.

Given the present circumstances of enormous delays in our legal systems, even if you do go to court and even win the case, you will still be left wondering who ended up being better off - you, the borrower, or your lawyer!

So, do look at the CRISIL / ICRA credit ratings for the company before you invest in company deposits or debentures.

Business risk

The market value of your investment in equity shares depends upon the performance of the company you invest in. If a company's business suffers and the company does not perform well, the market value of your share can go down sharply.

This invariably happens in the case of shares of companies which hit the IPO market with issues at high premiums when the economy is in a good condition and the stock markets are bullish. Then if these companies could not deliver upon their promises, their share prices fall drastically.

When you invest money in commercial, industrial and business enterprises, there is always the possibility of failure of that business; and you may then get nothing, or very little, on a pro-rata basis in case of the firm's bankruptcy.

A recent example of a banking company where investors were exposed to business risk was of Global Trust Bank. Global Trust Bank, promoted by Ramesh Gelli, slipped into serious problems towards the end of 2003 due to NPA-related issues.

However, the Reserve Bank of India's decision to merge it with Oriental Bank of Commerce was timely. While this protected the interests of stakeholders such as depositors, employees, creditors and borrowers was protected, interests of investors, especially small investors were ignored and they lost their money.

The greatest risk of buying shares in many budding enterprises is the promoter himself, who by overstretching or swindling may ruin the business.

Liquidity risk

Money has only a limited value if it is not readily available to you as and when you need it. In financial jargon, the ready availability of money is called liquidity. An investment should not only be safe and profitable, but also reasonably liquid.

An asset or investment is said to be liquid if it can be converted into cash quickly, and with little loss in value. Liquidity risk refers to the possibility of the investor not being able to realize its value when required. This may happen either because the security cannot be sold in the market or prematurely terminated, or because the resultant loss in value may be unrealistically high.

Current and savings accounts in a bank, National Savings Certificates, actively traded equity shares and debentures, etc. are fairly liquid investments. In the case of a bank fixed deposit, you can raise loans up to 75% to 90% of the value of the deposit; and to that extent, it is a liquid investment.

Some banks offer attractive loan schemes against security of approved investments, like selected company shares, debentures, National Savings Certificates, Units, etc. Such options add to the liquidity of investments.

The relative liquidity of different investments is highlighted in Table 1.

|

Table 1 | |

|

Liquidity of Various Investments | |

|

Liquidity |

Some Examples |

|

Very high |

Cash, gold, silver, savings and current accounts in banks, G-Secs |

|

High |

Fixed deposits with banks, shares of listed companies that are actively traded, units, mutual fund shares |

|

Medium |

Fixed deposits with companies enjoying high credit rating, debentures of good companies that are actively traded |

|

Low and very low |

Deposits and debentures of loss-making and cash-strapped companies, inactively traded shares, unlisted shares and debentures, real estate |

Don't, however, be under the impression that all listed shares and debentures are equally liquid assets. Out of the 8,000-plus listed stocks, active trading is limited to only around 1,000 stocks. A-group shares are more liquid than B-group shares. The secondary market for debentures is not very liquid in India. Several mutual funds are stuck with PSU stocks and PSU bonds due to lack of liquidity.

Purchasing power risk, or inflation risk

Inflation means being broke with a lot of money in your pocket. When prices shoot up, the purchasing power of your money goes down. Some economists consider inflation to be a disguised tax.

Given the present rates of inflation, it may sound surprising but among developing countries, India is often given good marks for effective management of inflation. The average rate of inflation in India has been less than 8% p.a. during the last two decades.

However, the recent trend of rising inflation across the globe is posing serious challenge to the governments and central banks. In India's case, inflation, in terms of the wholesale prices, which remained benign during the last few years, began firming up from June 2006 onwards and topped double digits in the third week of June 2008. The skyrocketing prices of crude oil in international markets as well as food items are now the two major concerns facing the global economy, including India.

Ironically, relatively "safe" fixed income investments, such as bank deposits and small savings instruments, etc., are more prone to ravages of inflation risk because rising prices erode the purchasing power of your capital. "Riskier" investments such as equity shares are more likely to preserve the value of your capital over the medium term.

Interest rate risk

In this deregulated era, interest rate fluctuation is a common phenomenon with its consequent impact on investment values and yields. Interest rate risk affects fixed income securities and refers to the risk of a change in the value of your investment as a result of movement in interest rates.

Suppose you have invested in a security yielding 8 per cent p.a. for 3 years. If the interest rates move up to 9 per cent one year down the line, a similar security can then be issued only at 9 per cent. Due to the lower yield, the value of your security gets reduced.

Political risk

The government has extraordinary powers to affect the economy; it may introduce legislation affecting some industries or companies in which you have invested, or it may introduce legislation granting debt-relief to certain sections of society, fixing ceilings of property, etc.

One government may go and another come with a totally different set of political and economic ideologies. In the process, the fortunes of many industries and companies undergo a drastic change. Change in government policies is one reason for political risk.

Whenever there is a threat of war, financial markets become panicky. Nervous selling begins. Security prices plummet. In case a war actually breaks out, it often leads to sheer pandemonium in the financial markets. Similarly, markets become hesitant whenever elections are round the corner. The market prefers to wait and watch, rather than gamble on poll predictions.

International political developments also have an impact on the domestic scene, what with markets becoming globalized. This was amply demonstrated by the aftermath of 9/11 events in the USA and in the countdown to the Iraq war early in 2003. Through increased world trade, India is likely to become much more prone to political events in its trading partner-countries.

Market risk

Market risk is the risk of movement in security prices due to factors that affect the market as a whole. Natural disasters can be one such factor. The most important of these factors is the phase (bearish or bullish) the markets are going through. Stock markets and bond markets are affected by rising and falling prices due to alternating bullish and bearish periods: Thus:

How to manage risks

Not all the seven types of risks may be present at one time, in any single investment. Secondly, many-a-times the various kinds of risks are interlinked. Thus, investment in a company that faces high business risk automatically has a higher liquidity risk than a similar investment in other companies with a lesser degree of business risk.

It is important to carefully assess the existence of each kind of risk, and its intensity in whichever investment opportunity you may consider. However, let not the very presence of risk paralyse you into inaction. Please remember that there is always some risk or the other in every investment option; no risk, no gain!

What is important is to clearly grasp the nature and degree of risk present in a particular case and whether it is a risk you can afford to, and are willing to, take.

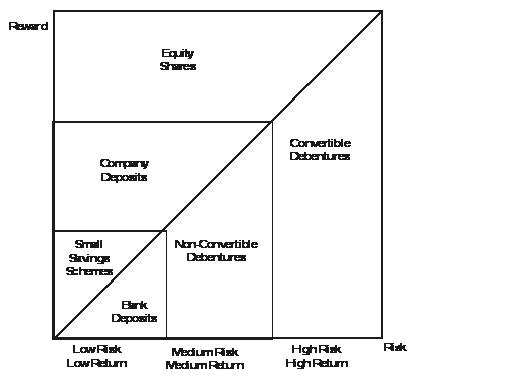

Success skill in managing your investments lies in achieving the right balance between risks and returns. Where risk is high, returns can also be expected to be high, as may be seen from Figure 1.

Figure 1: The Risk-Return Trade-Off

Once you understand the risks involved in different investments, you can choose your comfort zone and stay there. That's the way to wealth.

(Excerpt from Personal Investment & Tax Planning Yearbook (FY 2008-09) by N. J. Yasaswy, published by Vision Books.)

Published by ![]()