| « Back to article | Print this article |

Maruti's results and the investor response indicate that quite a few stocks in the auto sector could be on the verge of a big bounce, says Devangshu Datta.

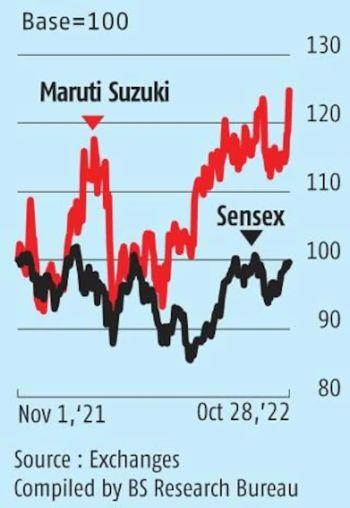

A jump in profits allied to optimism on the supply chain led to a bounce in the share price of Maruti Suzuki.

The company said it sold a record 517,395 vehicles in Q2, 2022-23: domestic sales stood at 454,200, while exports accounted for 63,195 units.

The firm had sold 379,541 units in Q2, 2021-22, when production was constrained by chip shortages.

In addition, the company claimed it had pending orders for 412,000 vehicles.

Maruti's consolidated revenue came in at Rs 29,943 crore, as against Rs 20,551 crore in the year-ago quarter.

The Ebitda (earnings before interest, taxes, depreciation, and amortisation) stood at Rs 3,433 crore, as against Rs 1,389 crore in the same period last year.

The firm's operating profit had dipped last year due to chip shortages and high commodity prices.

Efforts at sourcing electronic components, cost-reduction measures, and improving realisations led to much better margins.

The standalone Ebitda margin rose to 7.2 per cent from just 0.5 per cent, while consolidated PAT (profit after tax) jumped to Rs 2,113 crore from Rs 487 crore a year ago.

While the firm's top line was 1.4 per cent ahead of Bloomberg consensus estimate, its net profit was 4.3 per cent ahead of projections.

Even in sequential comparisons, the company's performance improved considerably over Q1, 2022-23.

In Q1, Maruti's consolidated revenue amounted to Rs 26,512 crore, with Ebitda of Rs 2,027 crore and net profit of Rs 1,036 crore.

The standalone Ebitda margin improved 220 basis points sequentially in Q2.

Another favourable factor has been the rupee's strengthening versus the yen, which reduced the cost of imports and other payouts to the parent.

However, while raw material costs have dropped and the disruption of supply of electronic components has also reduced, power costs have risen and so have advertising and marketing expenses.

There's been volume growth in every segment except for mid-size and LCV.

Mini+ compact sales volume was up 57 per cent YoY and van sales were up 32 per cent, while UV sales were up 10 per cent. Of course, there was a low-base effect but even so, the growth is impressive.

Overall, sales across the passenger vehicles segment, where Maruti is by far the largest player, have improved for most companies, with aggregated volumes growing by 15 per cent quarter-on-quarter (QoQ).

Chip supply normalisation has been noted for other auto manufacturers as well and raw material costs have fallen.

The festival season is crucial -- analysts will be monitoring rural demand through this period. One bad signal is poor growth in the tractor segment.

However, Maruti's huge order book ensures that it is very likely to have another record/near record quarter in Q3.

At the sector level, Maruti has lost market share -- now it has around 41 per cent compared with over 50 per cent pre-pandemic.

At the macro level, concerns about global inflation and rising interest rates remain.

This is an inherently capital-intensive industry and there are always working capital needs even in a scenario of high demand and smart inventory management.

Maruti's results and the investor response indicate that quite a few stocks in the auto sector could be on the verge of a big bounce.

On the NSE, the stock jumped 5.6 per cent on the results, and it's up 8.8 per cent in the last month and 19.5 per cent in the last year.

Feature Presentation: Rajesh Alva/Rediff.com