With State Bank of India (SBI), ICICI Bank, HDFC Bank and Axis Bank cutting their base rates, there will be an automatic reduction in interest rates of all floating rate loans.

There is some good news for those looking to buy a home.

With State Bank of India (SBI), ICICI Bank, HDFC Bank and Axis Bank cutting their base rates, there will be an automatic reduction in interest rates of all floating rate loans.

On Wednesday, ICICI Bank cut its base rate by 25 basis points (bps) to 9.75 per cent from 10 per cent and SBI cut its base rate by 15 bps to 9.85 per cent from 10 per cent.

Following the rate cut, ICICI Bank's home loans are now available between 9.9-10 per cent for general borrowers and 9.85 per cent for women.

In the case of SBI, the home loan rates are between 9.95 per cent (for women) and 10 per cent (general borrowers).

Axis Bank has cut its base rate by 20 bps, from 10.15 per cent to 9.95 per cent.

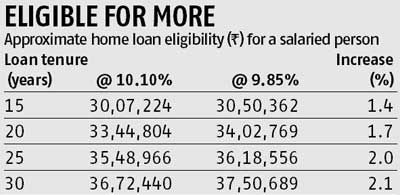

One of immediate benefit of a cut in lending rates is that the borrower’s loan eligibility increases.

A higher loan means the downpayment to be made by the borrower reduces to that extent.

“The average increase in loan eligibility with a 25 bps rate cut is between 1-2 per cent,” says Gaurav Gupta of MyLoanCare.

When banks cut lending rates, they usually keep the equated monthly instalment (EMI) constant and reduce the tenure.

When banks cut lending rates, they usually keep the equated monthly instalment (EMI) constant and reduce the tenure.

This is convenient because the borrower signs the electronic clearance service (ECS) mandate for a particular amount at the start of the loan. If the amount is reduced, the borrower will have to sign a new mandate, involving additional documentation.

Keeping the EMI constant is also advisable because this will not disturb borrowers’ monthly budgeting, says Jairam Sridharan, president, Axis Bank.

“If customers want to reduce the EMI and keep the tenure constant, they can ask their lenders. But since a home loan is a long-term commitment, there will be many situations when interest rates either go up or down. So, the EMI reducing or increasing will make your monthly outgo volatile,” he says.

Reducing the tenure will also bring down the overall interest outgo, compared to reducing the EMI, says Gupta. When you pay a higher EMI, you are paying off more from the principal amount and that will reduce the overall loan quantum.

For instance, assume for a Rs 50 lakh loan, with 13 years tenure, the rate of interest falls from 10.1 per cent to 9.85 per cent.

When the EMI remains constant at Rs 58,000, the savings is about Rs 2 lakh over the lifetime of the loan. Against this, when the tenure is constant and the EMI is reduced to Rs 57,133, the saving is Rs 92,535.

If you find that despite a reduction in rate, you are paying a higher rate that the current prevailing rates, you can move to the lower rate band after paying a certain fee to your bank.

If you find that despite a reduction in rate, you are paying a higher rate that the current prevailing rates, you can move to the lower rate band after paying a certain fee to your bank.

Usually, banks charge 0.5 per cent of the outstanding principal amount for moving to a lower interest rate band.

Despite this, if your rates are higher, you can transfer your loan to another bank, since there is no pre-payment penalty on balance transfers.

However, keep in mind the additional charges such as processing fees, legal fees and, in some cases, stamp duty and registration charges for the new loan agreement, says Gupta.