| « Back to article | Print this article |

At the time of global depression and economic slowdown, investors are looking at parking their investments safely. And gold is the obvious choice as a safe investment haven.

At the time of global depression and economic slowdown, investors are looking at parking their investments safely. And gold is the obvious choice as a safe investment haven.

During last two years, when all the asset classes have failed to perform, gold is the only investible asset that has remained upbeat. Gold is a hedge against the dollar and inflation. It has a very low correlation with other asset classes like equity and debt thereby a good asset to diversify the overall portfolio.

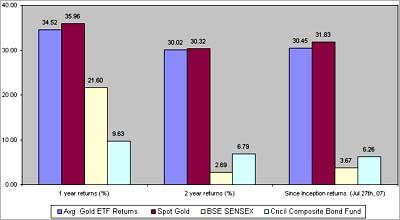

Gold Performance classes with other asset

Gold ETFs are open ended mutual funds that are passively managed and they mirror the return of spot price of gold. Gold ETFs are listed and traded on stock exchanges just like other stocks. Gold ETF gives investor an advantage to participate in the gold bullion market without taking any physical delivery of gold.

Gold ETFs provide returns, which before expenses; closely correspond to the returns provided by physical gold. Each unit is approximately equal to the price of 1 gram. To invest in gold ETF one needs to have trading and demat account, as gold ETF can be traded only in demat form.

Gold ETF is classified under mutual fund and is taxed as per debt mutual fund taxation rules. Investors investing in gold ETF are not liable to pay wealth tax.

About Gold Exchange Traded Funds

Advantages of Investing in Gold ETF:

Gold as an investment option

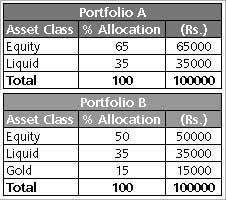

To minimize the investment risk one has to diversify his investments into different asset class. With diversification, he reduces the risk of loosing money in case his preferred asset has underperformed or when a specific sector is not doing well.

To better understand the advantages of diversification let's consider two portfolios, portfolio 'A' without allocation to gold and portfolio 'B' with 15 per cent allocation to gold. The total amount invested is assumed to be Rs 1 lakh.

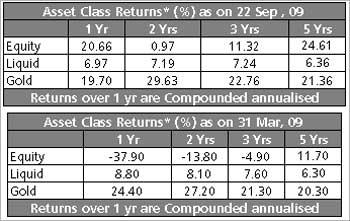

For computing returns, the equity part is assumed to be invested in BSE Sensex, Liquid part is assumed to be invested in CRISIL Liquid Fund Index and rupee based returns are considered for gold.

The comparative performance shows that Portfolio 'B' with 15% allocation to Gold has outperformed across time horizons when the equity markets are bearish till 31st Mar, 09 and also at the time when equities are outperformed (see below table for portfolio returns). The performance of gold as an asset class tends to have an inverse co-relation with the business cycle.

By extension, this provides gold an inverse correlation with other asset classes especially with equities. Thus, even in a potentially recessionary business environment, gold tends to provide an upswing to the portfolio and provides stability in a volatile market.

Future gold prospects

The global financial crisis, which started as housing collapse in US, has steamrolled into a massive recession, encompassing the developed economies of US, EU, Japan. As a policy response, the US Federal Reserve and other global central banks have resorted to deficit financing and fiat-currency expansion to help stimulate their struggling economies.

It is believed that the incidental impact of US Fed's balance-sheet expansion (currency printing) initiative may see an over supply of paper currency. The money supply in the US economy has been increasing year on year. Including $1 trillion in cash infusions, the stimulus plan will pump $9.7 trillion into the economy, according to Bloomberg.

Increased money supply may induce hyper inflation in the economy and cause currency devaluation. Gold is a hedge against both these factors. Gold has an inverse relationship with US dollar indicating that gold can protect value against the dollar.

Furthermore, the increase in demand for gold has far outstripped the global gold production. This provides a structural momentum to growth in gold prices. For instance, of the world's three biggest gold producers (China, South Africa and Australia), only China has managed to increase gold production in recent years. However, the increase in Chinese gold production has been matched by a corresponding rise in Chinese demand for gold.

During last one year China has doubled its gold holdings to 1,054 tons. Yet that only equals 1.6 per cent of its overall foreign exchange reserves. As China is moving out of US treasuries and into gold, this may trigger the next leg of the run-up in gold. Also according to US Treasury Dept currently, the US government holds about 286.9 million ounces of gold. It has printed about $1.569 trillion worth of paper dollars. If each dollar were to be backed by gold, that would put the price at $5,468.80 an ounce of gold. (Source: commodityonline.com)

South African gold output has been falling since 1970. Last year South Africa produced 272 tonnes of gold. The last time South Africa produced less than 260 tonnes of gold was in 1920. Australia saw its gold production slump 13 per cent in the second quarter to an 18-year low. Added to that, there has not been any major gold discovery in years.

This implies that the supply/demand balance in gold is becoming increasingly tight. And although interim volatility cannot be ruled out, gold prices are likely to trade higher.

The author is Head (Products) at Kotak Mahindra Mutual Fund.