Photographs: Rediff Archives

In the concluding part of this series on managing investment risks, Sanjiv Singhal explains how to handle investment risks that are beyond your control.

In the first part -- How to assess and manage investment risk -- we discussed why it is important for us to understand investment risks that could affect our ability to achieve our investment goals. We also identified three risks:

- Not knowing what the risks are

- Underestimating the goals

- Not understanding the interplay of investment amount, expected return and duration of investment

For the purpose of this post we'll assume that we have correctly estimated our goals and also worked out how much we need to invest and for how long to reach target expected rate of return. We're feeling pretty confident now.

Understanding the next set of risks -- things beyond our control -- is important for you to continue being confident.

Risk #1: What happens if the expected return does not materialise?

Expected return is just that -- 'expected'. It's usually a long term average for an asset class. For example expected return for equity in India is 16 per cent. But the return we get will most likely be different -- either higher or lower. There are usually three reasons for returns being lower than expected.

One reason is that we chose the right asset class (e.g. equity) but the wrong investment (e.g. specific stock or mutual fund).

This is a risk that has to be managed by monitoring the performance of your chosen investment against the benchmark for the asset class. Does your chosen stock or mutual fund perform in line with the benchmark? If it under-performs, you need to replace it with another. An annual review of your investments is a good idea.

This particular risk is enhanced when we use a passive investment strategy like a SIP (systematic investment plan). SIP is a disciplined investment strategy and works really well for long term investors with a regular income. But if you don't review the performance of the mutual fund into which your SIP is going, you maybe in for a rude shock. As a rule, review your SIP every year.

Second reason, which affects mostly fixed maturity investments, is that you were unable to reinvest at the rate you were hoping. For example, if you have a ten year horizon and choose a 5 year bank FD giving 9 per cent interest as an investment. When that FD matures interest rates may have declined and you may only be able to get 6 per cent for the next 5 years (this actually happened in 2004-2005!).

The best way to manage this risk is to align the maturity of your investments with your goal. It is however easier said than done.

Third reason, which affects mostly market-linked investments, is that when you need the money, the market may be down.

For example if you had invested money in equity for a goal in early 2009, you would have needed to withdraw money with a loss of capital. To manage this risk, you can adopt a strategy of shifting your money from equity to debt 2-3 years in advance. So if you need 100 rupees two years from now, shift 50 to 80 rupees today into fixed income. This strategy requires active management and leaves you exposed to regret if the market moves up.

The author is the COO of scripbox.com, a 'virtual' basket of four scientifically chosen mutual funds which seeks to leverage the power of technology and Internet to make mutual fund investing simple and convenient.

How to deal with investment risks you can't control

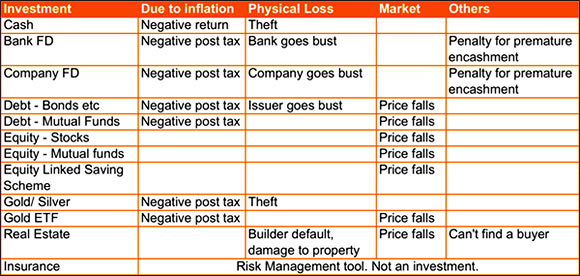

Risk#2: The risk of losing your money

This risk varies across investments and the loss can be invisible (inflation) or very visible (value goes down). Let's take a look at how this applies to various common investments options as shown in the table:

As we can conclude from the same table:

- No investment is "absolutely safe"

- Each investment has its own unique set of probabilities which could cause you to lose money

- Safety of principal is no safety because inflation reduces the value of money

I did not mention the risk of fraud in above because:

- The government and the respective regulators have made laws and regulations to prevent against fraud in all these cases. There are also strict guidelines and oversight for entities that are permitted to take your money (Banks by RBI, Mutual funds by SEBI). Bank deposits are also covered by deposit insurance.

A fraudster usually takes advantage of an investor's greed by offering unrealistic returns through some sort of a scheme. If you understand what the expected return of an investment is, you would not fall prey to fraud.

How to deal with investment risks you can't control

Photographs: Rediff Archives

Risk #3: Not being able to save long enough

Assuming that you achieve the expected return on your investment, the only other risk is that you are either not able to save enough or for long enough. This may happen due to loss of job, accident, illness, unexpected expenses or death.

This is where insurance comes in. Insurance fills the shortfall in your goals when you're unable to: Health and accident insurance for disease and injury; household insurance for loss of property and life insurance in case of death. We don't yet have layoff/redundancy insurance in India to cover job loss.

Conclusion: Living with risk

Now that we understand risks we can figure out how to live with them. Our financial life is no different from our day-to-day living in this respect. We are surrounded by risks. We may slip in the bathroom, get injured while crossing the road, be in a car accident, get robbed on our way home. However, we don't choose to stay in bed, and yet we don't suffer misfortunes everyday. This is because we take actions that help us manage those risks.

We use non-skid tiles, take the over bridge, drive within the speed limit and take a well-lit road home after dark.

Investing is similar.

Comment

article