| « Back to article | Print this article |

Can SEBI stop mis-selling of mutual funds?

The stock market regulator's move to label fund schemes of different risk profiles with discerning colours could be simple but powerful communication. But how much would risk differentiation help?

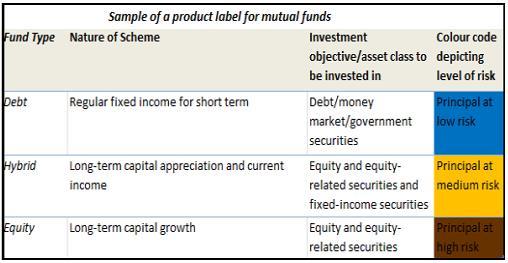

In keeping with its drive to prevent mis-selling of mutual-fund products and help investors take informed decisions, market regulator Securities and Exchange Board of India (SEBI) recently issued a circular stating, with effect from July, fund companies shall have to "label" their fund offerings to indicate their nature of the product, investment objective and risk level.

Thus, the label-- to be displayed prominently on application forms, scheme information documents and the key information memorandum -- for a liquid/debt fund would specify that the fund is suitable for investors seeking regular fixed income for short term (or something on similar lines), state the asset class it would invest in, and carry a blue-coloured tag indicating it is a low-risk product.

Similarly, hybrid funds would be labelled yellow while equity funds will sport the brown tag.

Additionally, a disclaimer would ask the investor to consult their financial advisor if they are not clear about its suitability.

Courtesy: ![]()

Can SEBI stop mis-selling of mutual funds?

Will it work?

The move is the latest among the many the regulator has undertaken in recent years to curb mis-selling of mutual fund products to investors without regard to their investment objective or risk profile.

In a market such as India where investor awareness is low and funds remain a push product rather than a pull product, such visual indicators are likely to be a powerful communication tool providing a clear indication of the different levels of risks they carry.

Industry experts have expressed concerns about the labelling system carrying the same tag for a single category of funds, within which you could have products of different risk profiles.

For instance, an index equity fund may not be as risky as an active equity fund; a conservative hybrid fund would carry lower risk than an aggressive hybrid fund; while in debt, an FMP is far less risky than a long-duration gilt fund.

But the move is clearly a step towards conveying the broad risk associated with each asset class in an uncomplicated, if perhaps oversimplified, way.

However, what is needed in greater magnitude are efforts to create more understanding about and thus demand for mutual-fund products in particular, and equity and debt instruments in general, among individual investors -- a goal that the regulator, the industry and the financial media need to work together towards.

Can SEBI stop mis-selling of mutual funds?

The bigger point being: for an advisor, risk tolerance and risk profiling may often not be as simple as asking an investor to fill up a questionnaire, looking through their age and financial status, enquiring about their goals or asking: can you foresee yourself taking a 50 per cent hit on your portfolio?

Because while these are certainly a good indicator of an investor's risk profile, several studies have shown that investors over-estimate their appetite for taking risks during booming markets and underestimate it in a bear market. That is, they would believe they are capable of investing in a higher-risk product if recent performance of that asset class has been good (a la 2004-2007) while lowering their perception of their own risk appetite after going through a nerve-wracking fall in the markets.

So it would not be surprising if the same investor who is shying away from a "yellow-labelled" hybrid fund today because of its equity exposure -- thanks to stocks' dismal performance in the past few years -- would be keen to lap up the higher-risk, "brown-labelled" equity offering at the peak of a booming market in the future.